For years, MB has argued that one’s principal place of residence must be included in the assets test for the Aged Pension on both equity and Budget sustainability grounds.

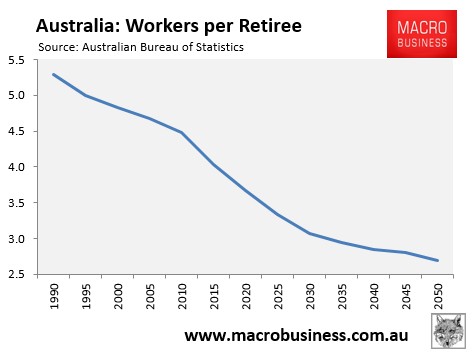

The underlying need for further Aged Pension reform can be boiled down to: 1) the fact that the ratio of workers supporting retirees is set to decline for decades:

And 2) that the Aged Pension (currently $44.2 billion in 2015-16 and rising to $52 billion by 2019-20) is the largest and one of the fastest-growing Budget expenses.

These factors alone make it inevitable that further Aged Pension reform will be required sooner or later.

In recent times, our argument that one’s principle place of residence should be included in the pension assets test has received support from diverse groups, including the Productivity Commission, The Grattan Institute, The ACCI, and the The CIS.

Now you can add research director at the Australian Centre for Financial Studies, Professor Kevin Davis, to this group. From The AFR:

[Davis] questioned the fairness of pensioners maintaining their assets, while still receiving a pension.

“The real issue here is people’s attitudes….is the pension a safety net to help people who can’t reach an adequate level of consumption in retirement or is it something, because I pay taxes, is it something I should be entitled to?” he said.

“One of the big problems with our whole approach is that a lot of retirees with part pensions have got $600,000 of assets, as well as the family home, and that doesn’t count towards the assets test.”

Mr Davis said the government should consider including the family home and increasing the asset test to compensate for that inclusion.

Professor Davis’ prescription is similar to the approach long championed by MB, namely:

- Include one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

- Once implemented, raise the overall assets test for the Aged Pension, as well as the base rate.

- Extend the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HELP-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under this plan, house-rich pensioners could continue to receive a regular income stream as they do now under the Aged Pension, but with less drain on the Budget and on younger taxpayers. At the same time, poorer renting pensioners, and those without significant assets, would receive greater financial assistance.

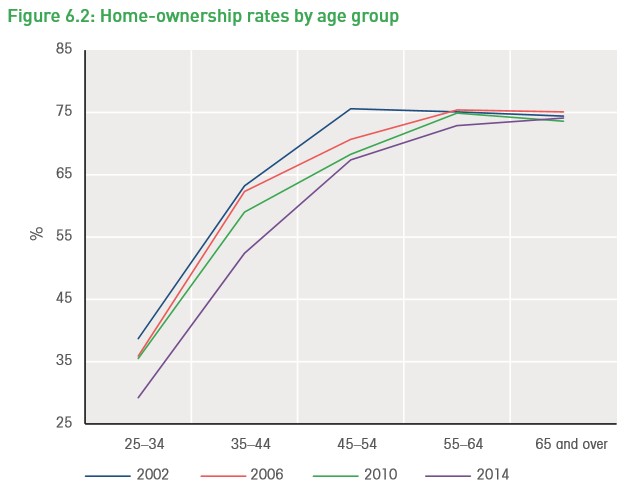

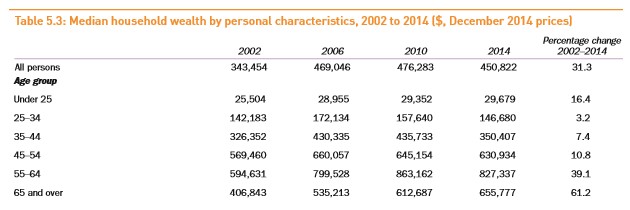

75% of retirees own their homes (most outright) and many have enjoyed massive windfall gains in wealth, thanks to the mammoth surge in Australian home values over the past 20 years (see below graphics).

However, this surge in retiree housing wealth has come at the direct expense of their children and grand children, whose wealth has barely increased, and who are now either locked-out of housing altogether or are required to undergo a lifetime of debt servitude in order to pay off a home.

Without reform to the Aged Pension, the burden of Budget cuts/tax increases will fall entirely on the growing pool of younger (and renting) Australians. This situation is clearly unsustainable from a Budget perspective and inequitable from an inter-generation one.

Unfortunately, while the economics (and logic) is straight forward, the political economy is not. Watch as landed retirees continue to fight like wounded bulls against further sensible pension reform.