From The Guardian this morning comes speculation that the Turnbull Government is considering making owner-occupied mortgages tax deductible in a bid to make housing more “affordable” by putting first home buyers (FHBs) on an equal footing with investors:

On Thursday Michael Sukkar, whose responsibilities include housing affordability, told Sky News the government wanted to give people a “realistic opportunity to save and purchase a home”.

Asked whether the government would consider adopting the US system where owner-occupiers deduct the cost of their mortgages from their tax bill, Sukkar said there was no “silver bullet” for housing affordability, including that option.

Sukkar suggested housing supply, not decreased demand, was the most important factor and reiterated government policy not to follow Labor’s lead by restricting negative gearing or reducing capital gains tax concessions.

But asked to rule out allowing owner-occupiers a new tax deduction to compete with investors, Sukkar said only: “I will examine, and I know that the treasurer will look at, all good ideas…

Asked if the owner-occupier deduction was under active consideration, a spokeswoman for Scott Morrison told Guardian Australia: “Housing affordability will be an important policy focus of the Turnbull government in this parliamentary term.”

Thankfully, economists have lined-up to lambast the idea:

The Grattan Institute’s chief executive, John Daley, told Guardian Australia the deduction would cost the budget $19bn a year and do little to improve housing affordability, compared with tackling negative gearing and capital gains tax concessions…

A University of New South Wales economist, Nigel Stapledon, told Guardian Australia the cost to the budget would be “pretty substantial”.

If you said to me in September 2015 that a Turnbull Government would consider making owner-occupied mortgages tax deductible, I would have laughed at you. But after witnessing its antics over the past 15 months defending negative gearing and the capital gains tax discount, as well as last month’s deplorable housing affordability inquiry, I certainly would not rule-out the Coalition introducing such a measure. They could try anything to support the housing bubble.

Any demand-side stimulus like this (or allowing FHBs to use their super savings to purchase a home) would be entirely self-defeating from a housing affordability perspective. Past experience has shown us unequivocally that such measures do not work.

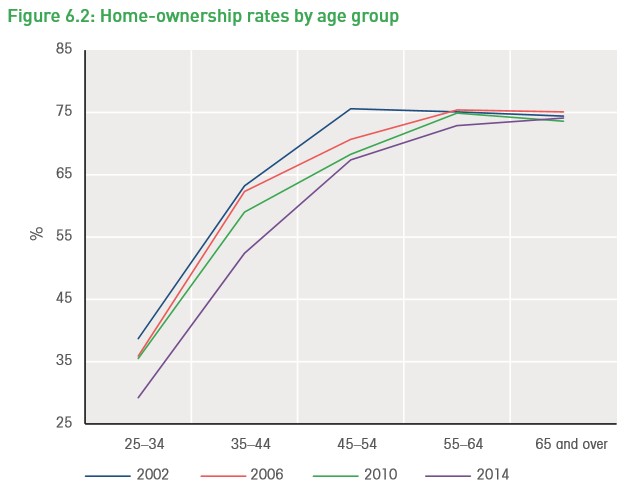

Despite the massive decline in interest rates and the myriad of subsidies provided to home buyers over the years, the home ownership rate has decreased, particularly for younger Australians (see next chart).

Allowing buyers to claim a tax deduction on their owner-occupied mortgage would simply increase their capacity to pay and would soon be capitalised into higher home prices. At the same time, the Budget deficit would be expanded considerably for no benefit.

The problem of unaffordable housing requires a combination of policy measures that tackles: tax lurks (including both negative gearing and the CGT discount); supply-side constraints; infrastructure bottlenecks; money laundering into, and foreign buying of, established dwellings; loose capital rules; over-investment by super funds; and excessive levels of immigration.

Just don’t expect the Coalition to address any of the real issues. It will continue to reach for gimmicks.