Blinkered consultant offers serfdom as super-pension reform

The scourge of the neo liberal age is the management consultant type which never actually delivers much of an outcome for anyone, but regularly appears in private sector and public sector workplaces, usually under the guise of doing something ‘strategic’ which involves talking to lots of ‘stakeholders’ but sometimes looking at ‘processes’ and how ‘efficiencies’ could be extracted from these.

This piece from the Fairfax press written by Elizabeth Henderson, who has a law degree, a physics degree, and has completed a course from the Institute of Company Directors – the full bio here http://www.loquemur.com/bio – along with some nebulous senior positions with Westpac, some workplace advisory leeches, and Freehills. No problems with any of that but it does give the impression of someone who has never settled in anywhere, and probably isn’t using too much of the physics or the legal qualifications in hanging out her shingle as a management consultant. In this piece she is looking to cement in the idea that people will have to work longer, which isn’t fundamentally a bad proposition, but she lacks the vision to look at the whole box and dice when it comes to superannuation, pensions, and Australia’s taxation settings, budget outlays structure, and immigration levels.

My children and I were born into different technological worlds but one thing we have in common is none of us had heard of a fax machine until our early teens. My daughter once asked “Mum, what’s a fax?” I could’ve asked the same question at her age. Although 1990s office workers couldn’t imagine working without one, in truth barely a generation relied on the fax for any meaningful period.

Australians today can’t imagine working without retiring, spending decades of healthy, active years not needing to work.

In the late 19th century, half of American men aged 80, and three-quarters of British men over 65, worked and only a minority lived that long to begin with. Most people worked until they died. A recent ad features a child and his grandfather visiting a museum exhibit of a couple driving in a convertible. “What are they doing grandpa?” the child asks. “They’re in retirement,” grandpa responds longingly. Grandpa may well have had to explain the exhibit to his own grandfather too.

Elizabeth has a problem with evolution. Call me crazy, but I tend to the view that when it comes to inventions and ways of doing things, evolution tends to lead to better simpler easier ways of doing things, and so it is with the fax machine.

If Elizabeth had thought to go back beyond the fax machine for maybe thirty years or so she would find a few interesting things:

1. That there were loads of people using carbon paper in typewriters and smudging their fingers stabbing invoices, receipts and the like onto spiked trays, and

2. The majority of the people doing this type of work were women, and

3. It was probably the only type of work the women could get, and

4. It was expected they would probably spend most of their lives at home looking after family.

Since the early 1990s the fax has largely been replaced by email, and digital imagery and electronic signatures. As someone who manages a workplace where there is still need to deal with carbon copies, holed pieces of paper from the distant past, and facsimile machines, I am firmly in the ‘this is a major improvement in doing business’ school. As a former workplace relations man I would also observe that the demise of the typing pool and rise of women throughout the workplace outside the typing pool is generally a good thing.

Elizabeth then makes the conceptual leap from the supersession of the fax machine to the take up of the late 19th century as the direction we are heading when sorting out retirements for the populace. She is quite right that a century ago pensions barely existed, and that large numbers of men worked into their dotage in the US and UK – though she omits to mention that women almost universally did not do paid work in that era, and she doesn’t mention returning to a late 19th century female participation rate, nor go within a bulls roar of looking outside the English speaking world.

‘Most people worked until they died’ is the message Elizabeth is looking to sell, possibly with the addition ‘that’s all any of you should expect, too’ – and in doing so she presumably wants to earn her consultancy a fee for writing something some corporate client would like to tell the world, loud and clear.

The corporate clients want to tell the world this loud and clear because they don’t want to pay tax to fund those retirements, after a generation of selling the line that workplace should be more flexible, but that people can take on more debt because they are working longer, and generally being of the view that the dividends from any efficiency should go to the shareholders, who should be free to treat employees as chattels.

After the fax machine and the reference to the late 19th century she wheels out a reference to a recent advert featuring someone’s grandpa. This is interesting because many peoples grandpas are at this moment on particularly generous pensions, made even more generous by the tax free status of a house they bought in the 1970s which is now worth more than a million dollars, often after setting up SMSFs or negatively gearing real estate to avoid paying taxes for a large slab of their lives – and they think that is an entitlement.

Elizabeth’s basic contention is that in order to free her clients from the need to pay tax people entering (or in?) the workforce today should be anticipating working until they drop, while still providing entitlements for those retirees already in the banana lounge. It sounds like bullshit, and it is.

Australia introduced the aged pension in the early 1900s when life expectancy at birth for men was 55 and for women, 60. If you made it to pension age, and most didn’t, you’d expect to live on the pension for no more than a decade.

The Inter-Generational Report uses forecasts that factor in life expectancy increases during a person’s lifetime. Using this data, a 60-year-old Australian today can expect to live to their late 80s, a child to their 90s. That’s averages. Half of Australia’s children today will probably live past 100.

Australians are living longer, and are likely to continue to live longer, thus making it all the more important that we sort out some way of funding their existences and providing them with meaningful jobs, is the point Elizabeth wants to make.

I’m from the first cohort of Australians to have superannuation their whole working life, accumulating it since my late teens with little time out of full-time work since finishing university. Super was supposed to work for me. Yet there’s no way I could retire in my 60s and avoid the pension, let alone maintain similar quality of life. It’s not due to poor returns or exorbitant fees. The key variables are retirement age, retirement savings and age of death. We can only influence the first two and the third is galloping ahead at such a pace that massive adjustments are required to the other two.

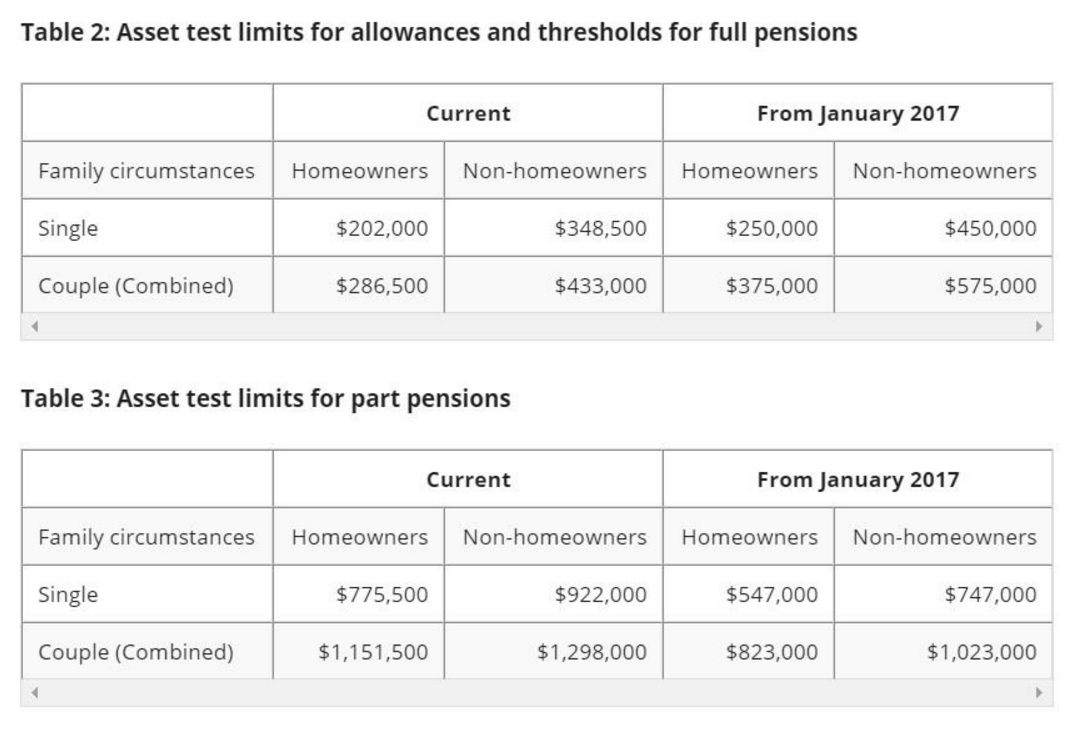

When she says ‘It’s not due to poor returns or exorbitant fees,’ she means that pension beneficiaries have in many instances been avoiding paying tax through SMSFs or negatively gearing, taking their superannuation entitlements as a lump sum and blowing this or stashing it in such a way as to retain entitlement to the aged pension, while at the same time the contribution side has never been made as large as it should have due to conservative governments baulking at increasing the mandatory contribution, and governments from both sides baulking at bringing the family home into the asset basket used to determine how much pension people get.

They still get quite a lot of they are millionaires – even after recent changes.

Similarly Elizabeth doesn’t look at any other mechanisms for funding retirements (eg land tax, reverse mortgages). It is also worth mentioning that through the entire piece there is no mention of what all these people will actually do to earn their keep, amidst thoughts that large numbers of jobs will simply be made redundant through automation, and at what point low wages or part time work ceases to make sense vis a vis the vicissitude of age. Meanwhile back at the ranch.

In their book The 100-Year Life, Linda Gratton and Andrew Scott consider the implications of longevity on retirement scenarios for different generations. Their modelling demonstrates the post-war generation could achieve a reasonable retirement income with affordable savings during their working lives, supplemented by corporate and government pensions.

Yep, and they generally had cheap housing, and being in the workplace during the era when mass credit (debt) was made available they got first access to it, bid up the prices of assets, and now are in a position to enforce subsequent generations to do then same.

However, someone born in 1971 with a life expectancy of 85 and retiring at 65 would need to save about 17 per cent per annum to retire on half their final salary, assuming they get a modest aged pension from the government. Quite confronting considering Australia’s compulsory super rate is 9.5 per cent per annum and the Inter-Generational Report predicts someone born in the early ’70s will live closer to 90.

For someone my age, retiring at 65 essentially requires income earned from two thirds of my adult life to stretch over the remaining third.No wonder the system is buckling under its own weight for Generation X.

Elizabeth does have a valid point here. The system as it is currently set up makes absolutely no sense whatsoever for anyone under the age of 50. If we had political leadership in this country we would expect policy changes, but the current regime (and opposition) is largely about running the current system until it simply seizes up, and enjoying the parliamentary perks until that moment arrives.

The answer is to fund the superannuation system properly, to make it work as an actual savings system (as opposed to a tax avoidance system), include the principal place of residence as part of the basis for calculation of access to the government funded pension, and to remove incentives to take lump sums and blow the cash. Beyond that there is a case for working out what careers will gainfully keep people occupied as they get older, making it worthwhile for them to continue working, and assisting and promoting people taking up opportunities to do so.

Increasing the pension age to 70 (well below what’s realistic) should be a no-brainer, not a political football. The complaint that workers in physical jobs can’t keep working past their 60s or re-skill doesn’t stack up. Medical advances are not only increasing life expectancy but also leaving people fitter and healthier for longer. Anyway, exponential growth in technology wand automation means regular re-skilling will be the norm for 21st century humans, whether they’re 65 or 35.

Yep, I would even buy this but Elizabeth is missing the strategic picture. Australia currently has a taxation structure which rewards avoiding tax – capital gains taxes, negative gearing, SMSFs, PPOR concessions etc. Getting rid of the distortions and enabling people to make choices on the best allocation through life, and particularly underpinning a framework which makes home ownership – which has been demonstrated to reduce health and aged care costs for the elderly – cheap and accessible, rather than a cash cow for governments and a ticket clipping exercise for the FIRE sector.

Get rid of this and the super system will work better – more:

A bigger political challenge is restructuring super so it works. Tinkering with tax rates and concessions, contributions caps and limits doesn’t address structural deficiencies caused by 21st century demographics. A more fundamental problem is people accessing super two or three decades below their life expectancy. Or whether it’s realistic for people to lock money away for 60 years, in what more resembles a time capsule than an investment. Especially with politicians licking their chops to get their hands on it either through taxes or by forcing super funds to invest in pet projects.

The bigger political challenge is ultimately going to be to front up to the public and identify this equation, and at that point work out who has dibs on the proceeds, or to sell the idea that we need to contribute massively more to the superannuation system. For sure there is a case for saying that people may need to work longer, but at the same time there is a case for saying that we may not have the jobs to give them anyway, which means that we approach the point of working out if society is a by-product of the capitalist system.

Concepts like a Universal Basic Income or altering the way the superannuation system is used over a lifetime, e.g for funding education, business start ups and home ownership, like an actual savings and investment scheme.

There needs to be a whole new look at wealth creation, wealth distribution, taxation, and the allocation of government monies, and the role of people in that – and that is before we get around to the question of how many more people we need.

Most likely, we’ll choose to return to our forbears’ practice of working as long as we can. Like the fax machine, “retirement” may prove to be a transitory innovation.

Well that maybe the case but only if we tell ourselves that we can’t think of a better way. Given that much of the world is coming out of third world status on the back of globalism, it would be truly Trumpetarian if the best that the management elite could do is tell us that for that to happen we need to send our aged back into neo-feudal serfdom to survive. And if that is the message then enlisting today’s teenagers to contribute to society may be a hell of a tough ask.

And if we are looking for some vision in order to address the issues of today and tomorrow, it is probably best to be very, very careful in the choice of management consultants. It would seem that some don’t have much.