The notion that Australia’s unions are warriors for fairness just got kicked to the curb, with the Australian Council of Trade Unions (ACTU) engaging in a despicable robo-calling campaign against the Coalition’s equitable changes to the Aged Pension. From The Canberra Times:

Pick up the phone tonight and you might find a stranger on the line: Leanne.

Leanne doesn’t have a last name – or a return number – but she does have an earnest message about her father and the Turnbull government’s changes to the age pension…

The robo-call is anonymous, with no authorisation or hint of its origin, but Fairfax Media has confirmed it is the work of the Australian Council of Trade Unions, which has launched an 11th-hour campaign against the January 1 changes.

The Abbott-era reforms, passed with the help of the Greens in 2015, will redistribute some income to needier pensioners while saving $2.4 billion over four years from the wealthy.

The asset limit will increase substantially, meaning those underneath it will gain an average of $30 a fortnight. But those above the threshold – about 330,000 people – will lose part or all of their pension…

ACTU secretary Dave Oliver said the cuts would upend the carefully-planned retirements of thousands of pensioners, and the ACTU would use “any means” necessary to fight back…

“We make no apologies about using any means to fight for those targeted by the cuts who have worked hard their whole lives and are entitled to a comfortable retirement.”

The ACTU’s criticism of the pension reforms do not pass scrutiny.

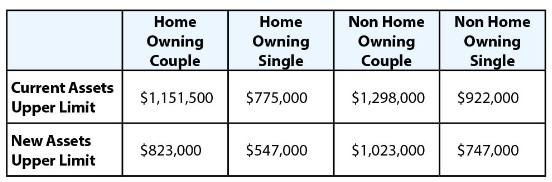

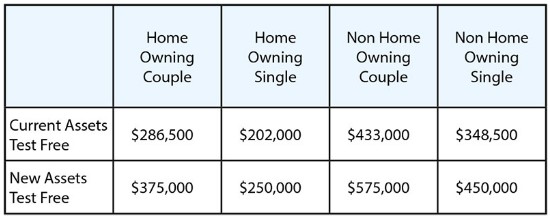

To recap, the 2015 Budget announced that the thresholds for the Aged Pension would be adjusted so that those with financial assets (in addition to the family home) of $547,000 for singles ($823,000 for couples) will no longer qualify for the part-pension (see below table).

According to these changes, financial assets above $375,000 for a couple will lose access to the Aged Pension at the rate of $3 per $1,000 in assets, up from $1.50 currently. It is important to note that this change merely restores the settings back to their pre-2007 state before Treasurer Peter Costello recklessly loosened the financial assets test.

However, while access to the part pension has been curtailed, the assets threshold has also been increased, thus benefiting those retirees with fewer financial assets (see below table).

Thus, the pension changes agreed by the Abbott Government and the Greens will make the system more equitable. As such, they are supported by the Australian Council of Social Services, which noted the following after their passage:

“The changes to the Pension assets test passed by the Parliament last night help ensure that the Pension is going to people who need it, including improving the adequacy for people who have limited assets. The tightening of the assets test to pre-2007 levels reinforces the role of the pension as a safety net payment to prevent poverty,” said Dr Cassandra Goldie.

“ACOSS also welcomes passage of legislation abolishing the Seniors Supplement. This Supplement is very poorly targeted, going to older people who are not eligible for the Age Pension due to their substantial assets”.

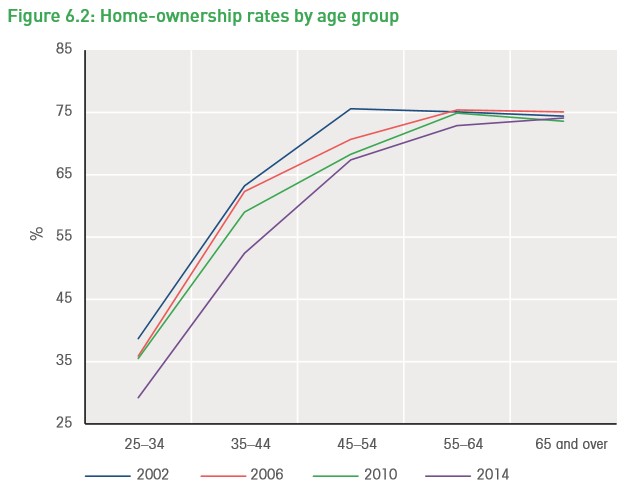

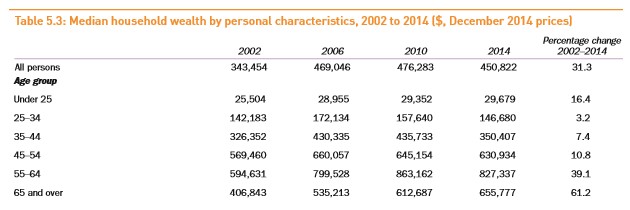

We also should acknowledge that the 75% of retirees that own their homes (most outright) have enjoyed massive windfall gains in wealth, thanks to the mammoth surge in Australian home values over the past 20 years (see below graphics).

This surge in retiree housing wealth has come at the direct expense of their children and grand children, whose wealth has barely increased, and who are now either locked-out of housing altogether or are required to undergo a lifetime of debt servitude in order to pay off a home.

How is it fair that these same mega-mortgaged or renting younger Australians are expected to fund the retirements of older home owners, who are in many cases far wealthier than they are?

If the ACTU cared at all about equity it would instead argue to have the family home included in the assets test for the Aged Pension, with part of the money saved redirected to significantly increasing the base rate of the pension as well as the assets test threshold. This way, welfare would be far better targeted to those pensioners without any significant assets – either financial or non-financial.

Meanwhile, home owning retirees that miss out on the pension could maintain their income levels by taking out a reverse mortgage through the government’s Pension Loans Scheme – a state-run reverse mortgage scheme that allows eligible retirees to borrow against their homes to receive payments from the government equivalent to the full Aged Pension.

The interest rate through the Pension Loans Scheme is only around 5.5%, repayable upon their estate or sale, and these home-owning retirees could continue to live in their home as they do now. For all intents and purposes, they would experience no change in their living standards, but with far less drain on the Budget over the longer-term.

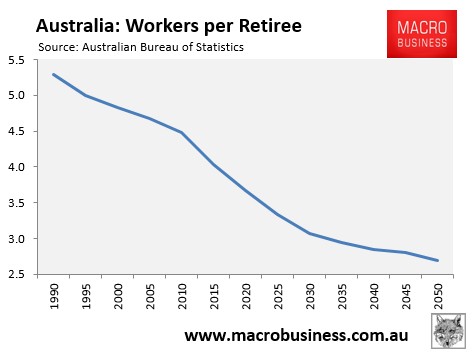

With the Aged Pension costing the Budget some $44.2 billion in 2015-16 and rising to $52 billion by 2019-20, and the ratio of workers supporting the elderly shrinking (see next chart), the system as it currently stands is not sustainable and inequitable from an inter-generational perspective.

The ACTU should acknowledge these truths rather than running a scare campaign against these modest but sensible pension reform.

unconventionaleconomist@hotmail.com