by Chris Becker

Stocks here in Asia rose in sympathy with overnight markets as the mood from the Italian referendum is a definite “meh” to risk managers. Most currency traders were looking to a surprise from the boffins at Martin Place, but the RBA held this afternoon and the Aussie dollar remained elevated against most majors.

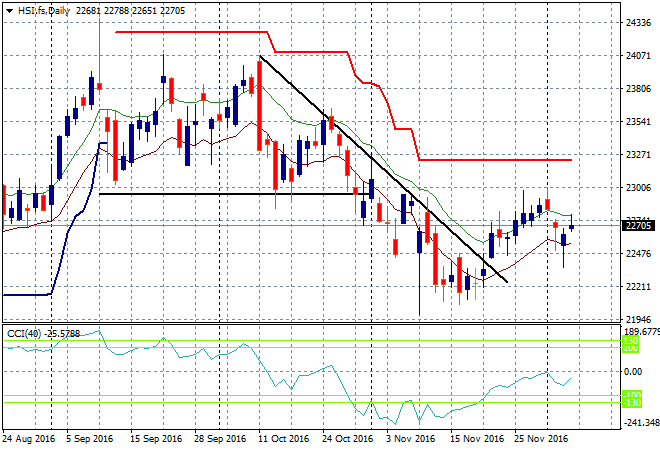

The Shanghai Composite is putting in a scratch session after slumping more than 1% yesterday and is holding on to some weak gains after the lunch break. The Hang Seng is doing much better, up nearly 0.8% as it tries to claw back the Monday losses. The daily chart still shows a serious level of resistance around the 23000 point level that the semi-independent bourse must crack if its little bear market rally is to have any legs:

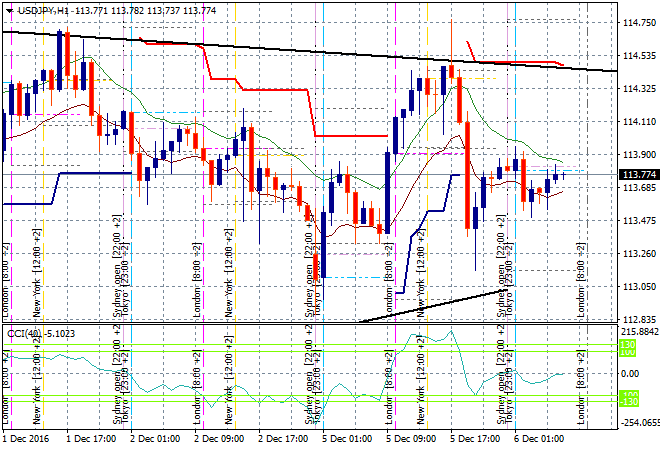

In Japan, share markets are up just under half a percent as the Yen remains steady at its point of control on the USDJPY pair, currently just below the 114 handle. USD has failed to make a new high against Yen for several days now and latent volatility is building here:

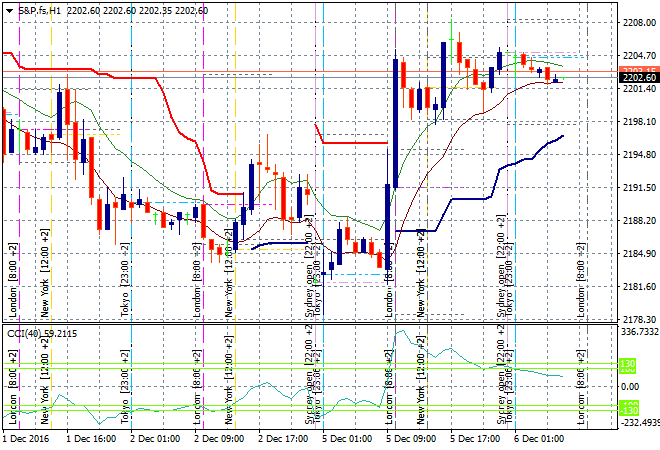

S&P Futures are steady during the Asian session where it looks like a solid open on Wall Street and in London later tonight:

The ASX200 closed up 0.5% to be above 5400 points again, with Megabank providing the heavy lifting – namely the ANZ and CBA chapters as BHP rallied 1.5% to remain above $25 per share. The RBA’s lack of action helped quieten markets going into the close, so this should stick failing an overnight catalyst.

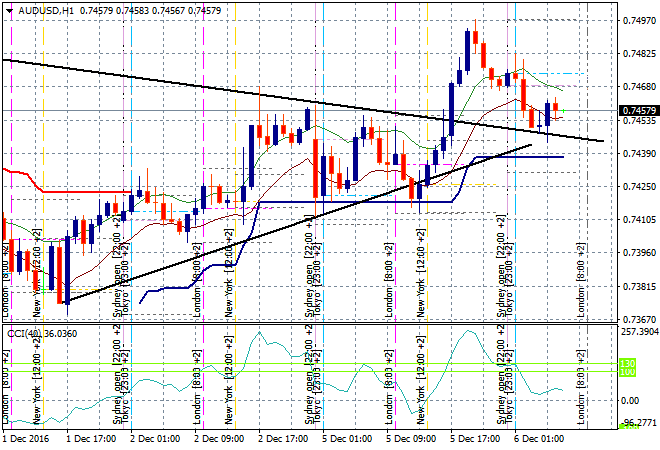

The Aussie dollar fell on the open this morning to its tentative hourly trendline and has come back slightly following the do-nothing RBA release, currently at 74.60 against USD and still remaining positive overall:

The data calendar tonight has a few low tier PMI releases to absorb in Europe, while in the States its just final prints for factory orders and the like.