Although it took the election of Trump to the presidency and his subsequent promise to ‘rebuild America’ to shift the market’s attention toward inflation, core and headline inflation have actually been in a solid uptrend over the past year.

From its low of 0.2%yr in September 2015, headline PCE inflation has risen to 1.4%yr at October 2016. Unaffected by energy prices, core inflation started this period at 1.4%yr and has since firmed to 1.7%yr. Notably, on a 3-month annualised basis, headline and core PCE inflation have converged of late, respectively 1.8% and 1.7%.

Inflation is therefore nearing the FOMC’s medium-term target and, together with a labour market effectively at full employment, is giving strong support to the removal of policy accommodation. (Note, while not the focus of the FOMC, CPI inflation is actually stronger again, with core CPI inflation above the FOMC’s 2% target on both an annual and annualised basis.)

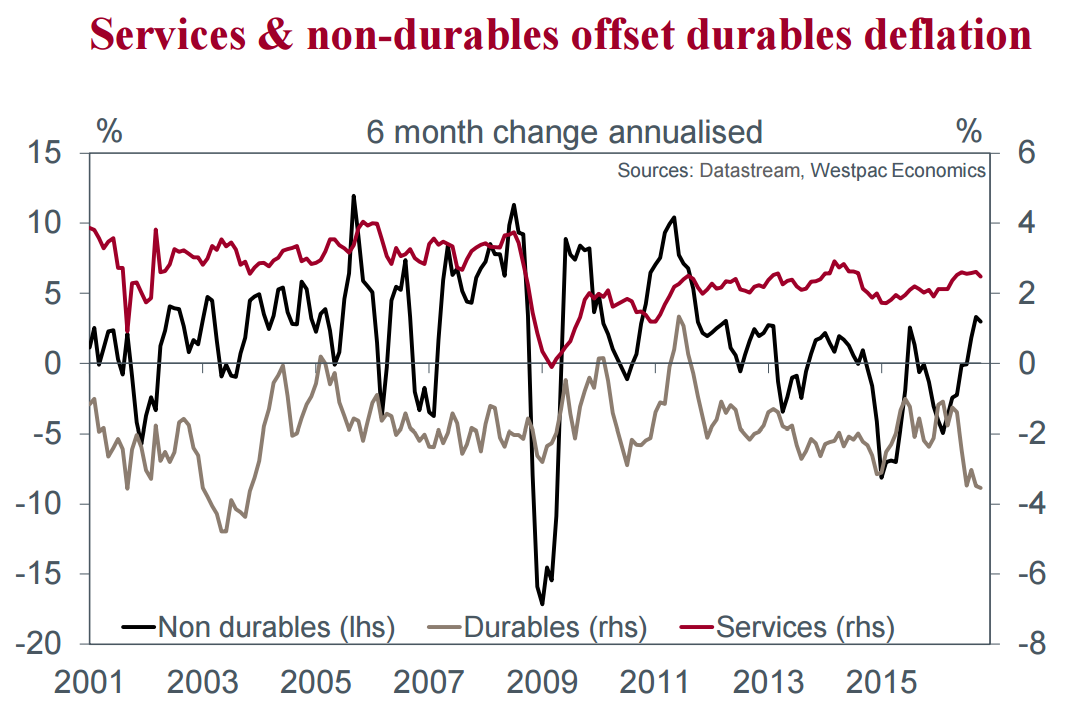

Partly due to strength in the US dollar as well as the soft state of global end-demand and cost efficiencies from globalisation, durables have been a persistent deflationary influence on the US. Of late, 6-month annualised durables deflation has been running steadily near –3.5%, a pace at the lower end of the range of the past 15 years. However, offsetting durables’ impact has been strengthening non-durables goods and robust services inflation.

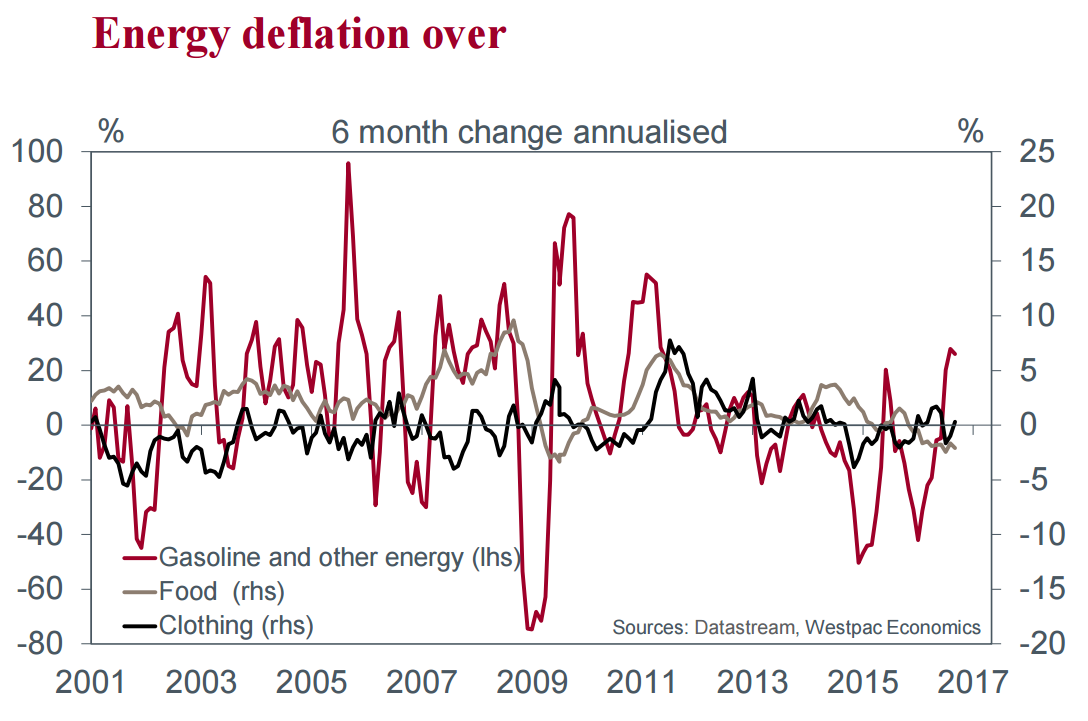

Starting with non-durables, energy prices have remained the key influence through 2016. From a recent low of –42% in February 2016, 6-month annualised PCE energy inflation has risen to +26% at October 2016. Needless to say, despite its small weight in the consumption basket (circa 2.4%), this abrupt shift in gasoline and other energy prices has been a primary contributor to the turnaround in headline inflation in 2016. Its contribution to 6-month annualised headline inflation has risen from –1.0ppts in February 2016 to +0.6ppts currently. Food has acted as a partial offset to energy inflation; while clothing has had little net impact.

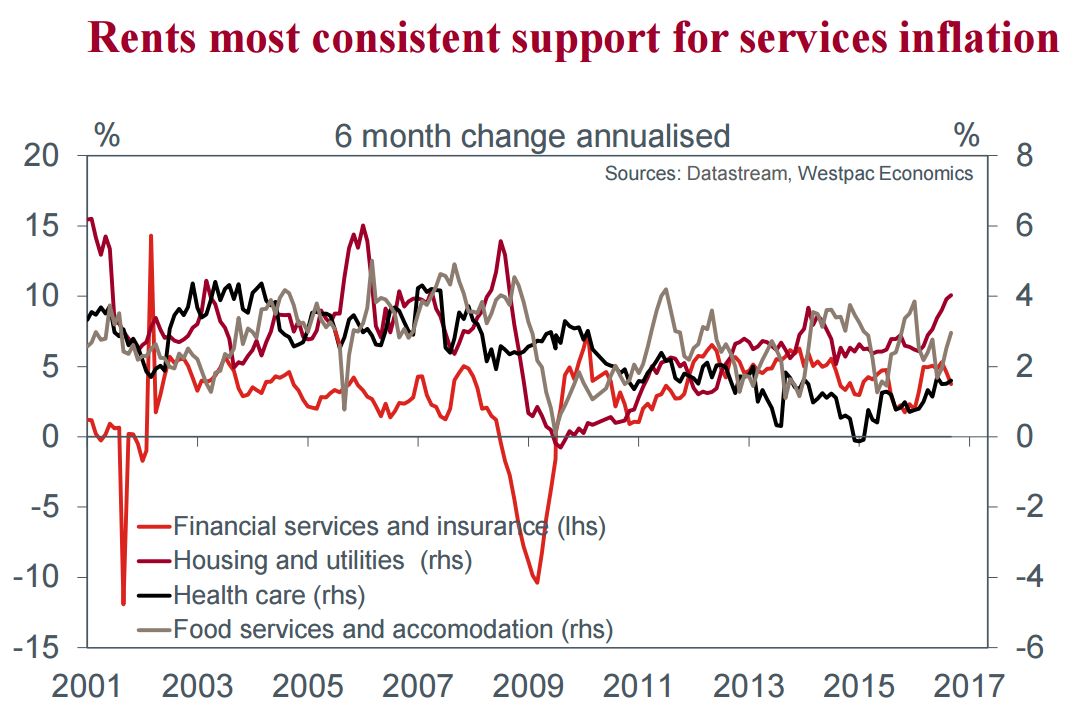

If we then turn to services, we clearly see the material impact reduced slack in the labour market is having on inflation. Since the beginning of 2015, services inflation has been trending up from 1.7% to 2.5% on a 6-month annualised basis. As we have often cited, a key contributor to this acceleration in services inflation has been housing and utilities, where price growth has risen from 2.4% to 4.0% at October as strong growth in rents (circa 3.5% annualised) persists and the previously deflationary impact of commodity prices on utilities has reversed.

In addition to the strong inflationary bid from housing, more recently we have also seen stronger price growth for health care and food services and accommodation. Both sectors have likely been materially affected by higher minimum wage requirements instituted in many states over the past 18 to 24 months, and it seems many businesses have responded by raising prices for end users of their services. Health care inflation has also been aided by affordable health care, which has seen a greater proportion of the population insured. However, these price gains have come at the expense of consumers who increasingly face higher premiums.

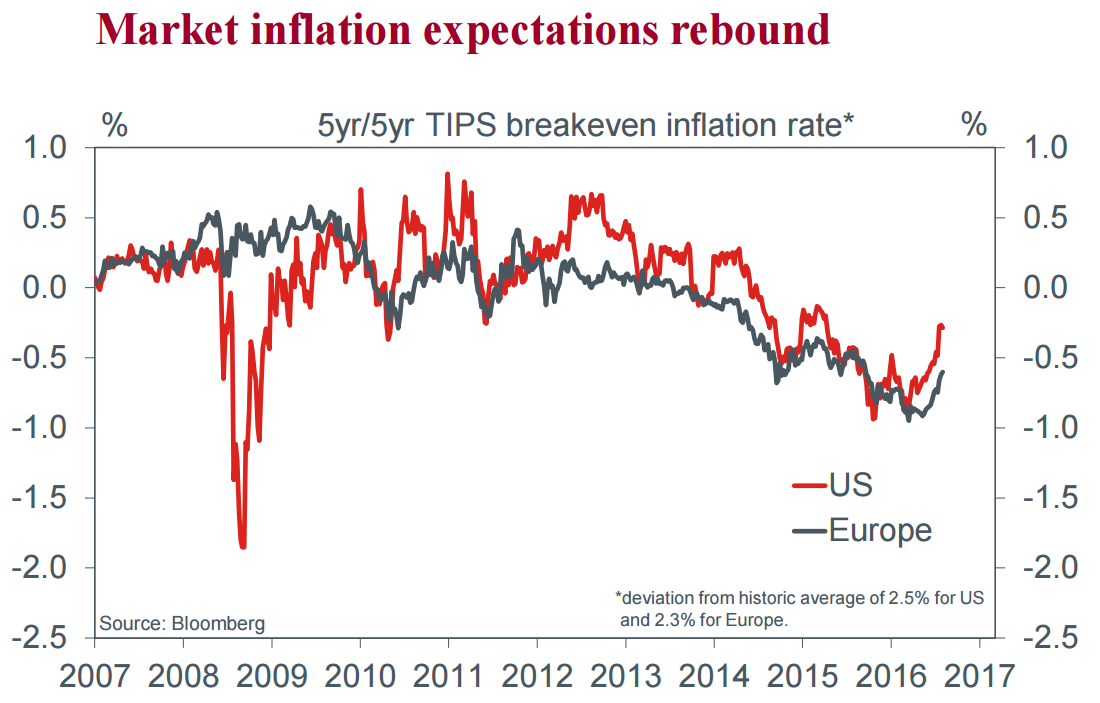

As a final point, it is worth mentioning that household expectations are yet to respond to accelerating PCE and CPI inflation. Historically these term expectations have been well anchored, limiting demandside pressures for wages/inflation. If this remains the case, then inflation should stay near the FOMC’s medium-term target and continue to allow the Committee to slowly normalise the Fed Funds Rate as befits the state of the real economy.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.