Ahead of the December ECB Governing Council meeting, market participants had been debating if the existing program would be sustained or tapered, or indeed whether we would have to wait until March 2017 to find out what the ECB had in mind.

Thankfully, after having failed to do so in the past, the Council took a pro-active approach to policy, clearly outlining their plans past the current March 2017 end date.

As outlined in the decision statement, from April 2017 ECB asset purchases will continue, albeit at €60bn per month versus the current €80bn pace. To aid market functioning and the program’s effectiveness, the Council also announced that the minimum duration of purchasable assets will be lowered from two to one year and that securities with a yield below the deposit rate of –0.10% will now also be available for purchase.

While this may look like the first step in a linear tapering program, the Council went out of its way to emphasise it is not. Firstly, the next stage of the program will run until at least December 2017 – markets had only been looking for a commitment until September. More significantly, note that if “the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment of the path of inflation, the Governing Council intends to increase the programme in terms of size and/or duration”.

As it stands then, the ECB’s asset purchases will remain open ended and be calibrated to current and expected conditions.

For the ECB, there are two critical aspects of the economy to consider: (1) bringing headline inflation back to its 2%yr target, as per their mandate; and (2) reducing the still substantial degree of slack in the economy to sure up underlying inflation and real economic growth – herein confidence and credit are key.

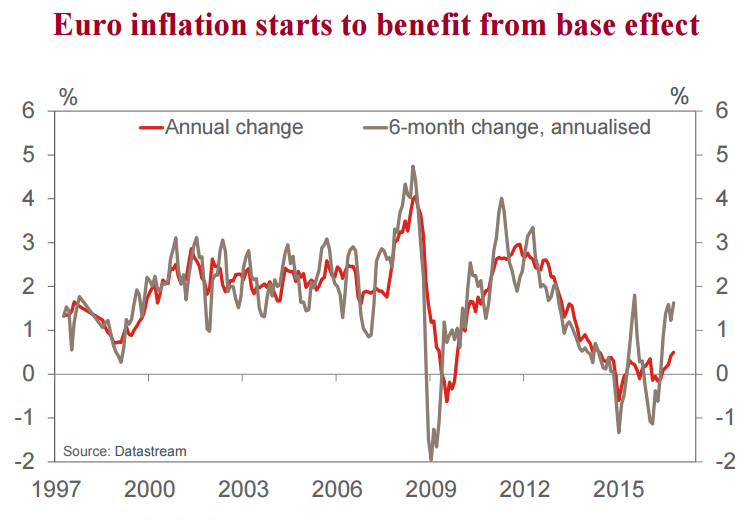

On headline inflation, “rates are likely to pick up significantly further at the turn of the year”. From 0.2% in 2016, headline inflation is expected to rise to 1.3% in 2017; 1.5% in 2018 and then 1.7% in 2019. Given their 2%yr target, if realised this profile would argue for a further tapering of purchases into 2018.

But the issue for the ECB is that the rise in headline inflation will come mainly as a result of “base effects in the annual rate of change of energy prices”. Speaking to a material degree of slack in the economy as well as downside risks to real activity, “there are no signs yet of a convincing upward trend in underlying inflation”.

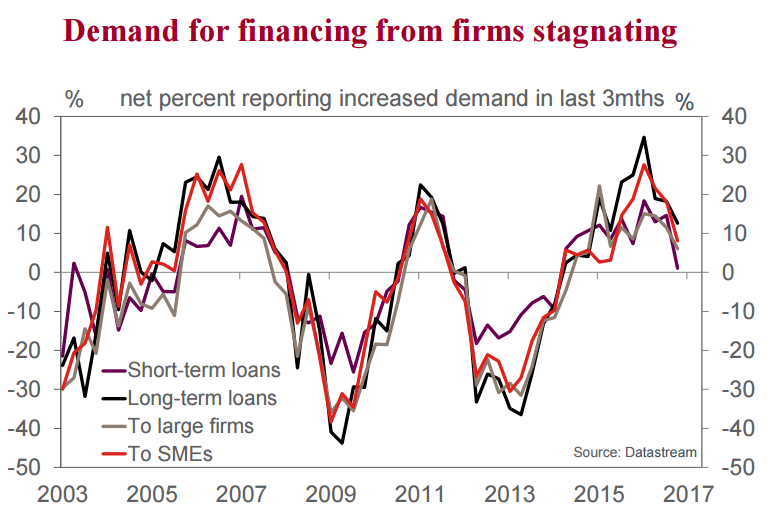

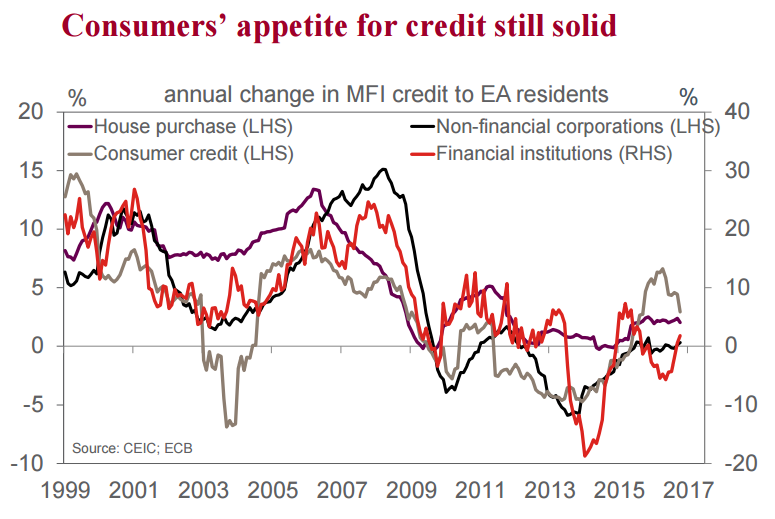

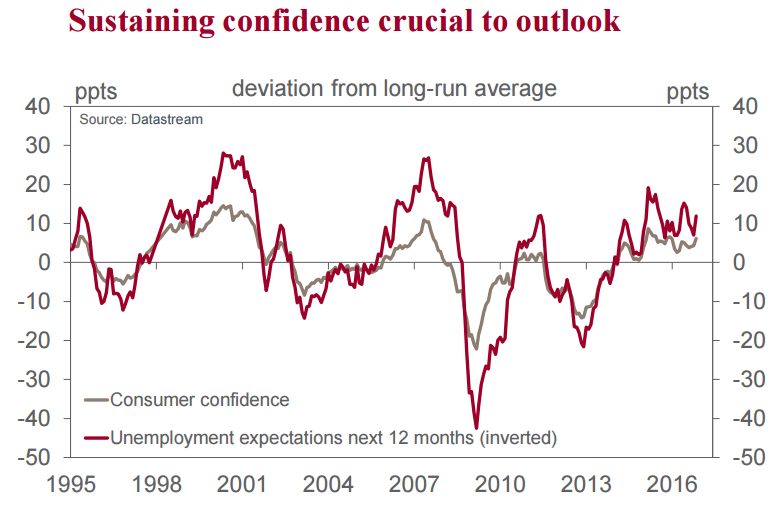

This is where confidence and credit come in. On both fronts, the ECB has had some success in the most recent phase of its alternative easing program. Business and consumer confidence have both risen materially, the former aiding employment prospects and the latter household spending. However, business investment remains mixed (to say the least) and household incomes are yet to receive a material boost. Further, of late momentum has waned for confidence and credit, casting some doubt over the growth outlook.

So, while the published ECB growth profile remains constructive (the Council anticipating gains of “1.7% in 2016 and 2017, and by 1.6% in 2018 and 2019”), downside risks are ever present. Our own forecasts incorporate some of these downside risks, with growth of around 1.2%yr expected through 2017–19. If we are correct, the ECB will have to maintain purchases well into 2018 (and possibly beyond). To do otherwise would be to put at risk confidence; the provision of credit; and medium-term inflation prospects.

Very dovish says ANZ:

EURO TREND WEAKENING IN PLACE AS ECB RAMPS UP QE·

The ECB delivered a bazooka. It extended QE (by EUR540bn), allowed the purchase of bonds with a minimum one year maturity and the purchase of bonds with yields below the deposit rate (-40bps).

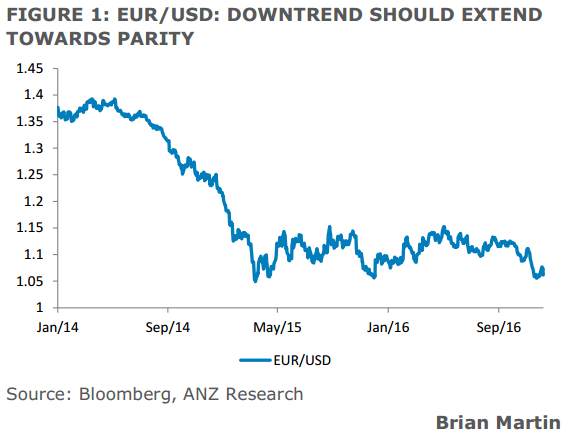

The euro fell and the forthcoming political cycle suggests portfolio outflows from the euro area will continue. Further EUR underperformance vs USD, AUD, NZD and Asia is expected.

European interest rates are not going up. Based on the ECB’s guidance it could be 2020 at the earliest before “normalisation” starts.

Dovish enough, is my answer, and trapped by disintegration politics.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.