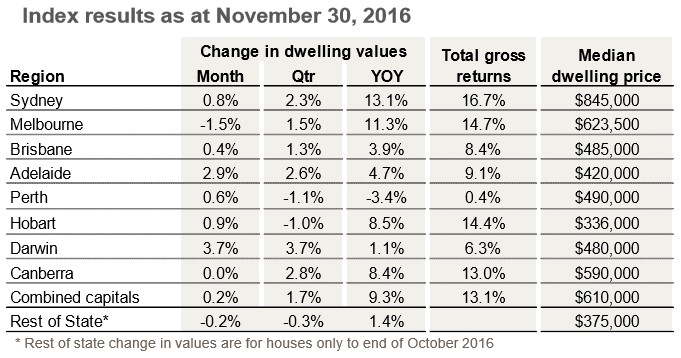

Following on from yesterday’s post on CoreLogic’s daily dwelling values index results for November, CoreLogic has released its full results, which also cover the smaller capitals and regional areas (see next table).

As shown above, the smaller capitals and the regions had a mostly positive month in November, with Darwin (+3.7%) and Hobart (+0.9%) reporting value gains, Canberra flat, and Rest of State (-0.2%) recording a fall.

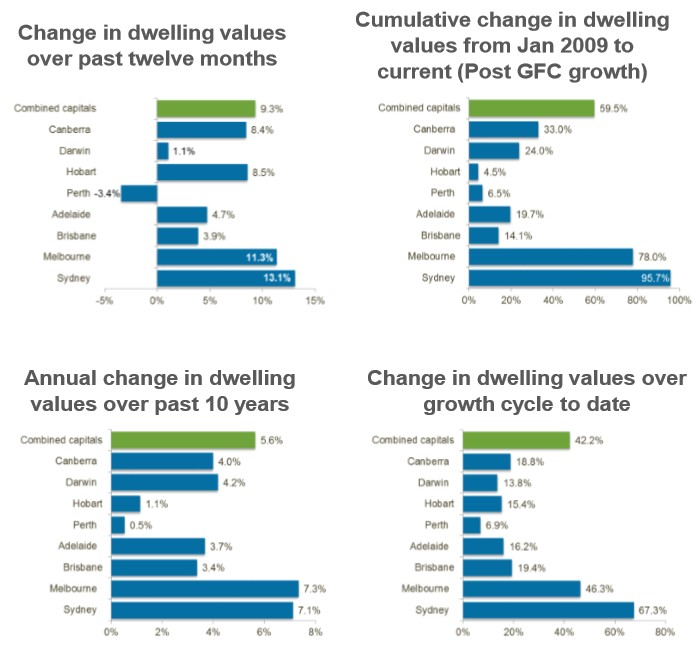

Below are the key charts summarising the situation across the markets, with Sydney and Melbourne dominating:

Advertisement

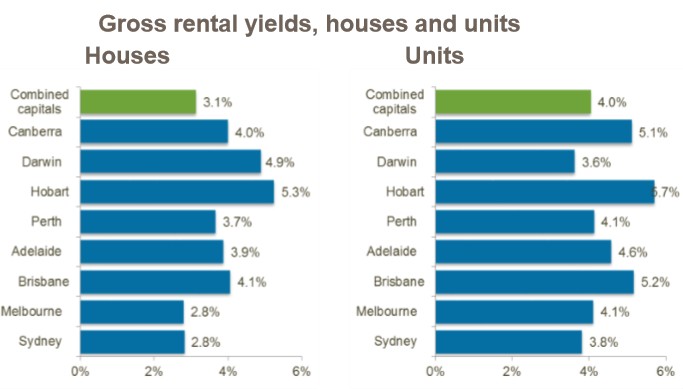

The combination of weak rents and capital appreciation continues to compress rental yields, which have fallen to record low levels:

Advertisement

According to CoreLogic:

Rental yields reached a new record low in November across the combined capitals index due to dwelling values continuing to rise at a faster pace than weekly rental rates. The average gross rental yield across combined capital city dwellings is now recorded at 3.2%, down from 3.5% a year ago and 4.1% five years ago.

Sydney and Melbourne share the lowest yield profile for detached housing, with an average of 2.8% in both cities, while the gross yield on Sydney units has fallen well below Melbourne’s at 3.8%.

Mr Lawless said, “With rental markets remaining soft, it is likely there will be further yield compression across those markets where residential property values are rising.” “The only market segments where yields have improved over the past 12 months were the Hobart and Canberra unit markets where rental rates have shown a higher growth rate than unit values.” “It appears as though the low yield profile is no deterrent to investors, with ABS housing finance data showing a consistent rise in finance commitments for investment purposes since May this year.

“Clearly investors are continuing to see housing as the preferred investment option, despite low yields and a mature growth cycle.

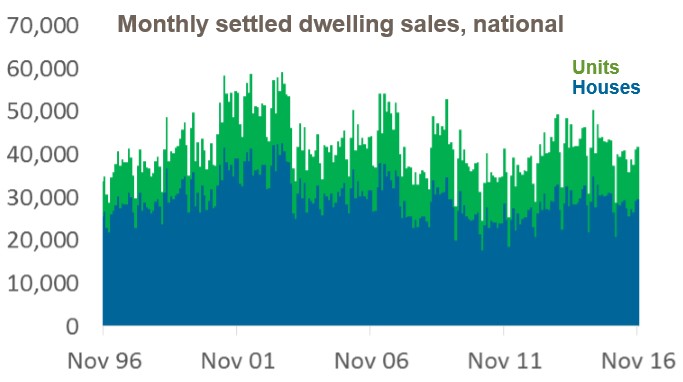

CoreLogic also reports that listings and transaction volumes are depressed despite a recent resurgence:

Settled transaction numbers nationally have reversed their downward trend over recent months with CoreLogic estimates of settled sales rising to the highest level in a year. Even though transaction numbers have improved, settled sales remain 9.6% lower than a year ago. Every state and territory has shown a reduction in settled sales over the year, however the largest fall has been in Victoria with a 14.9% year-on-year decline. In contrast, CoreLogic mortgage valuation platforms experienced record daily volumes earlier this week, reflecting the robust level of late season market activity.

As the last month of spring, November has seen listing numbers ramp up more substantially with the total number of homes advertised for sale over the past month now tracking higher than a year ago. The latest CoreLogic listing counts show there were approximately 113,500 properties advertised for sale over the past 28 days across the capital cities, which is 2.4% higher than the same time a year ago.

According to Mr Lawless, despite higher listing numbers at a combined capitals level, the hottest markets are still showing listing numbers lower than a year ago. Sydney listings are 9.4% lower than last year, while advertised stock levels in Melbourne are 2.9% lower. Hobart listings have fallen sharply compared with last year, to be 29% lower, whilst Canberra stock is 7.6% lower than a year ago.

He said, “Lower stock levels in these markets are likely to be one factor contributing to the upwards pressure on dwelling values. Vendors are still very much in the driver’s seat in these markets and buyers have little in the way of leverage to negotiate, or time to consider their purchase decision.”

Advertisement

Finally, CoreLogic suggests that the boom in home values is on borrowed time:

After four and a half years of strong value growth, Mr Lawless said it’s hard to imagine a reacceleration in property values could be long lived.

“Affordability constraints are creating high barriers to entry, particularly in Sydney, and lenders are becoming more cautious in their lending practices.

The supply pipeline is substantial for inner city units, which is likely to dampen value growth in these precincts as well as dent buyer confidence and push vacancy rates higher.” “Additionally, buyer enthusiasm could be muffled by speculation that interest rates may rise late next year, with fixed rates already starting to edge higher.”

“With household debt at record levels, Australians are very sensitive to the cost of debt, and an expectation that the period of record low mortgage rates is approaching an end may reduce buyer demand,” Mr Lawless said.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.