Weeoo, weeoo, weeoo. The Pascometer is screaming:

…according to the bond market reaction, he will burst Australia’s east coast housing bubble by causing interest rates to rise.

That would be the relatively nice way to prick the bubble. The more common fear is that he could start a trade war with China that would cause a global recession – one we wouldn’t escape. That definitely would not be a nice way to achieve lower housing prices. So let’s hope there is enough sanity left in Congress to prevent such madness and just consider the more benign interest rate story.

…With the advent of Trumpistan, there is the possibility Trump will be an inflation driver. That would start changing the economists’ forecasts. It certainly makes them less certain.

The idea is that the immediate uncertainty could stay the Federal Reserve’s hand next month, but a big-spending, big-deficit Trump could push up rates a little further down the track.

…Genuinely stronger inflation in the US though would play a role in lifting global inflation – a more fundamental and important shift. If it happens, Australian individuals will have to start thinking about the chances of a rate rise. The increased borrowing power delivered by interest rate cuts has been the key factor is pushing east coast housing prices ever higher this year. Given the record household debt those cheap rates have encouraged, it will only take a tiny touch of the monetary brakes to have impact – taking the top off the bubble.Nonetheless, a bit more inflation is what the world needs. And greater fiscal stimulus through investment in infrastructure is what most economists, including our Reserve Bankers, have been calling for. The potential problem with Trump’s “plan” though is that he also wants to boost defence spending, sharply cut taxes and do it all in a hurry.

If Trump keeps most of his pledges, the chance of “nice” inflation recedes and the possibility of global recession increases. And with that, the consensus view of further RBA rate cuts become much more likely, along with higher unemployment and, therefore, lower housing prices.

As we all know, it usually pays to do the opposite with The Pascometer. At this stage I remain skeptical that the Australian rate cycle has bottomed. Trump’s inflationary policies are going to be more or less counterbalanced by the tightening Fed and bond vigilanties. A more sobering risk to local rates is the arrival of Trump politics. Once immigration growth is lowered then there’ll be a better chance for wages and income growth in the existing population. Protectionism may revive as well with the same result. Though neither is an immediate risk. Another inflation risk is that the Australian dollar is going to fall, quite possibly to new lows and quite quickly. However, all of these will confront the resumption of falling terms of trade when the amazing bulk commodity bubble bursts so I still don’t buy it.

For me it is only a matter of time before an external shock pops the east coast property bubble. As I’ve argued for a few years, we’re out of policy ammunition to support it. The last 100bps of monetary easing is virtually meaningless. Fiscal policy is shot and facing sovereign downgrades. The population ponzi is political poison now. Moreover, the prospects for the economy one year out are terrible as the dwelling boom rolls over. Hiking rates into that is an amusing thought for a crashnic!

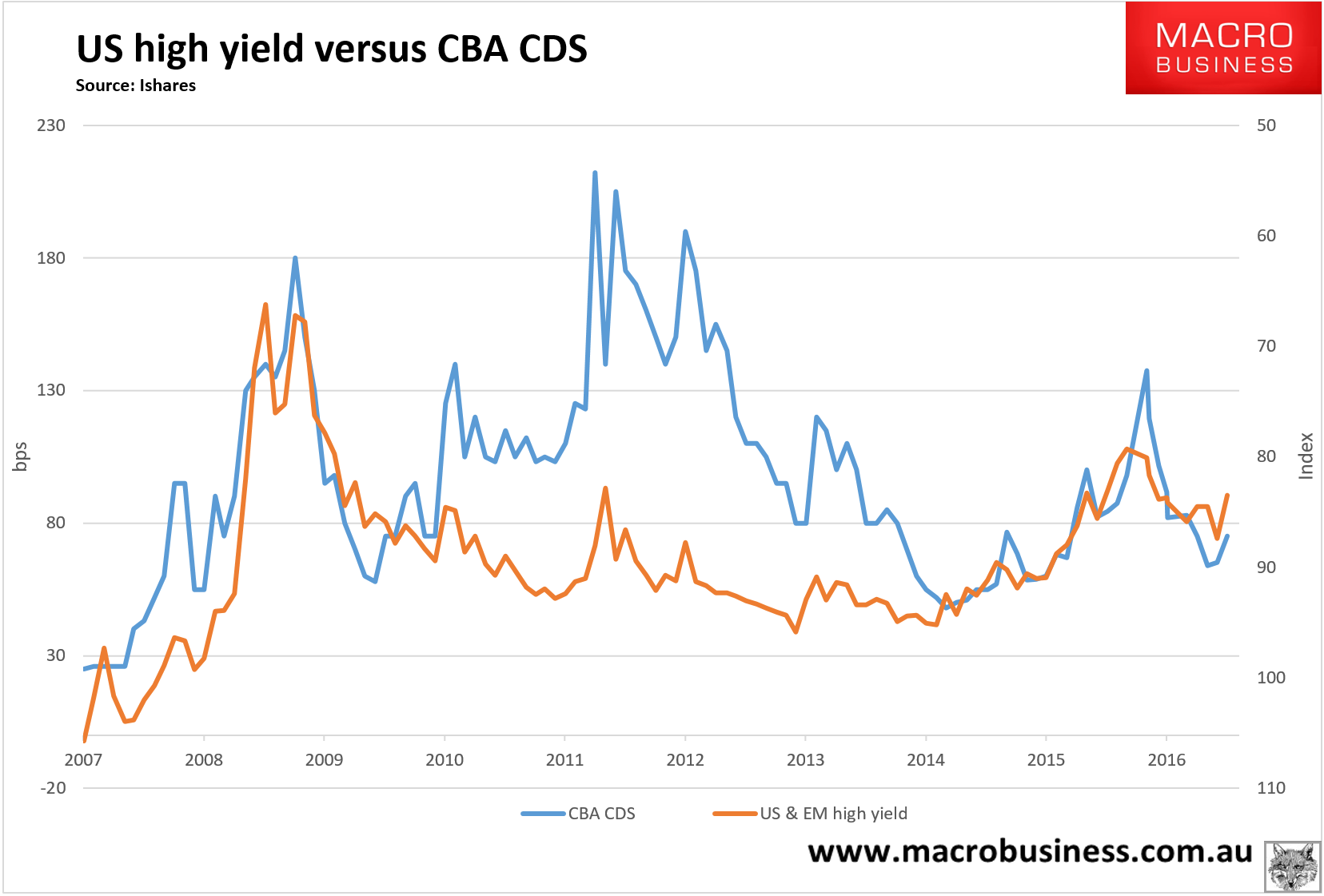

However, I do not think that it will be inflation or a rising cash rate that will do it. A greater danger is rising offshore funding costs for the banks as emerging markets come under severe strain because capital flows out towards the US as its dollar soars. US and EM high yield debt is correlated with the bank’s offshore funding costs:

As the USD rises and pressures EM interest rates, the key for Australia is the bulk commodity bubble. Where it goes, local inflation and interest rates will follow. If the EM bust really gets moving then the cash rate will fall not rise as an offset.