Westpac is out with its full year result via CLSA’s Brain Johnson:

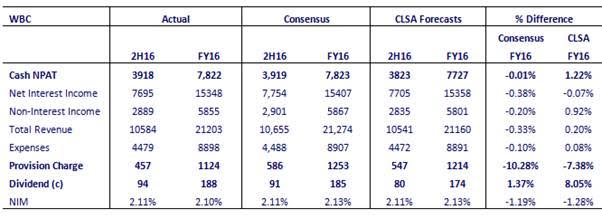

The WBC FY16 result of A$7822m was in-line with consensus and a slight beat on CL numbers. The final dividend was held flat at 94c above consensus and CL expectations. Breaking down the FY16 result; the margin was inline, with modestly below consensus expectations on revenue and expenses offset by a lower than expected loans loss charge but a higher than expected tax rate with benefits related to the finalisation of prior period taxation matters in 1H16 not repeating. Overall the result was Ok at first glance with issues well flagged the 3Q16 asset quality and capital update with the slight earnings downgrades. WBC are flagging previous 15% ROE target is not achievable with a new target of 14% to 15%.

Net interest margin was 2.11%, a decline of -3bps from 1H16. Key features included:

3 basis point increase from asset spreads. The full period impact of Australian mortgage repricing, including for additional regulatory capital requirements, was partly offset by broad based lending competition and higher short term funding costs;

2 basis point decrease from customer deposit spreads, driven by increased competition for term deposits and the impact of lower interest rates on transactional deposit spreads;

3 basis point decrease from term wholesale funding spreads reflecting the lengthening of the average tenor in preparation for the implementation of NSFR and investors requiring increased spreads for new issuance. This saw new issuance spreads above maturing deals;

Capital and other decreased 1 basis point primarily from the impact of lower interest rates; and l Liquidity costs were little changed, with the cost of increased holdings of high quality liquid assets to meet the LCR requirement, offset by a lower CLF fee following a $7.4 billion reduction to the CLF from 1 January 2016.

Non-interest income decreased A$77m, or 3% compared to First Half 2016, with trading income lower by $96m, primarily in the commodities portfolio and subdued activity impacting customer sales.

Operating expenses increased A$60m or 1% compared to First Half 2016, driven by increased costs related to the Group’s investment programs (A$67m) which are mostly reflected in higher technology expenses. Productivity benefits increased 27% to A$147m and these more than offset growth in operating costs ($99 million) and higher regulation and compliance costs (A$41m).

Impairment charges for Second Half 2016 were A$457m, down -A$210m compared to 1H16, and were equivalent to 14bps of average gross loans. The decline was mostly due to lower new IAPs as the first half included a small number of institutional downgrades as indicated above.

Total stressed exposures increased (FY16 1.2%, 1H16 1.03%, FY15 0.99%)

The effective tax rate of 30.5% in Second Half 2016 was higher than 29.3% in First Half 2016, primarily from benefits related to the finalisation of prior period taxation matters in First Half 2016, not repeating.

Outlook

Continued discipline on growth/return

New liquidity rules see tighter link between loan and deposit growth

Active margin management required given competition and higher funding costs

Target expense growth at bottom end of 2-3% range

Productivity gains similar to FY16

Asset quality expected to remain sound

Continue to invest to support franchise growth and productivity

This resolves none of the structural issues that has MB giving the banks a wide berth: extreme payout ratios leading to unusually high vulnerability to bad debts, regulatory tightening and funding cost pressures.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.