Westpac has produced a useful update on Australia’s investment project pipeline that is well worth a look. Below are the key extracts.

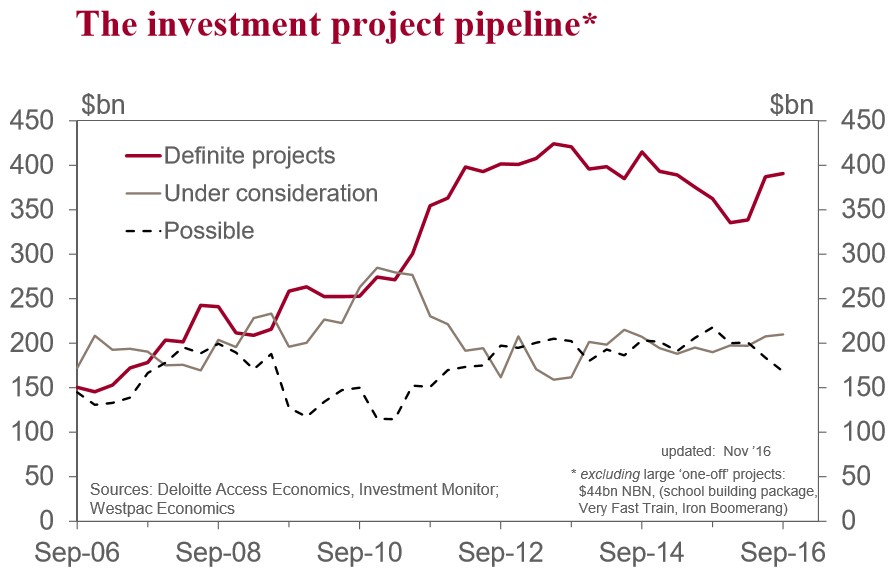

The end of the mining investment downturn, which remains the dominant dynamic shaping Australia’s investment project pipeline, is in sight.

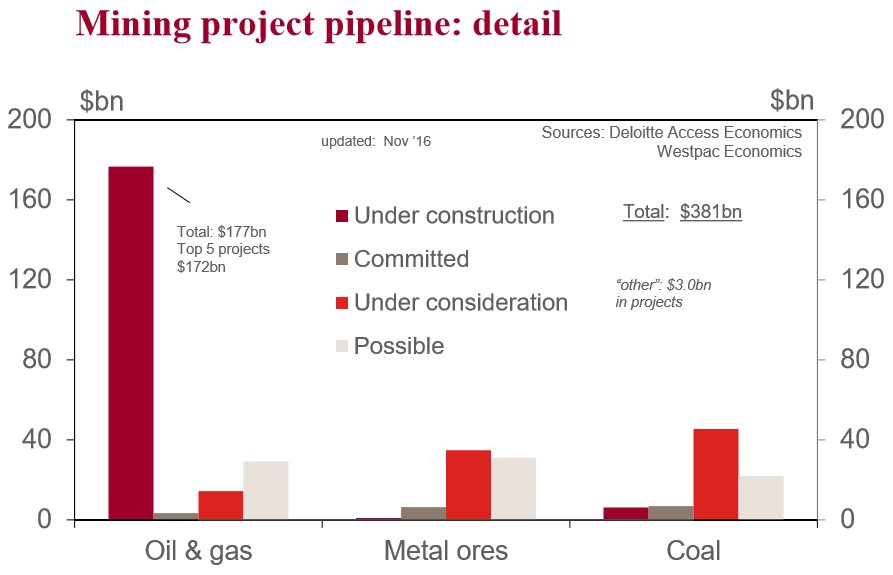

The 5 remaining mega gas projects under construction, with a combined value of $172bn, are due to be completed by end 2017.

This will see the value of definite mining projects (those under construction or committed) fall sharply, down from $201bn currently.

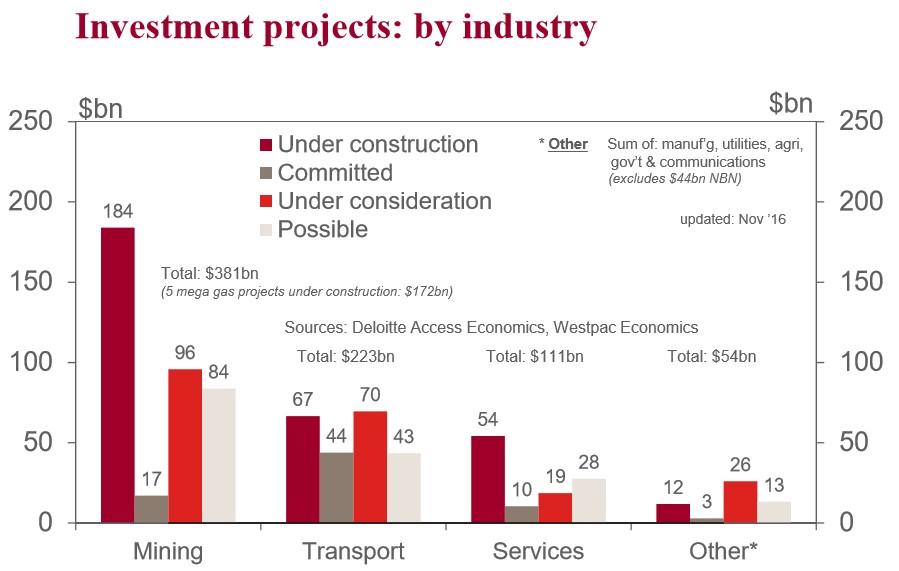

The other key dynamic, albeit less powerful, is the upswing in public transport projects.

Definite public transport projects are now valued at $100bn. This represents a sharp increase on a year ago, up $45.4bn, including a $5.3bn rise in Jun.

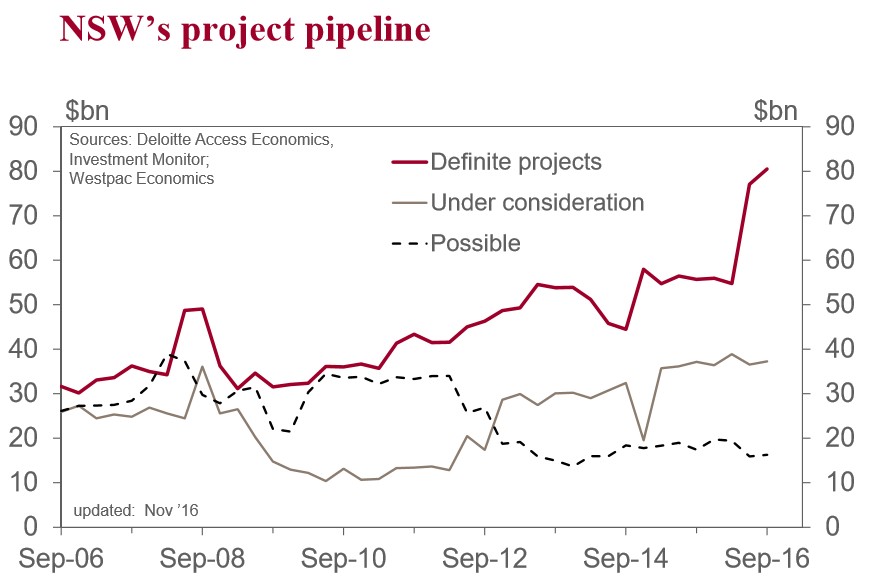

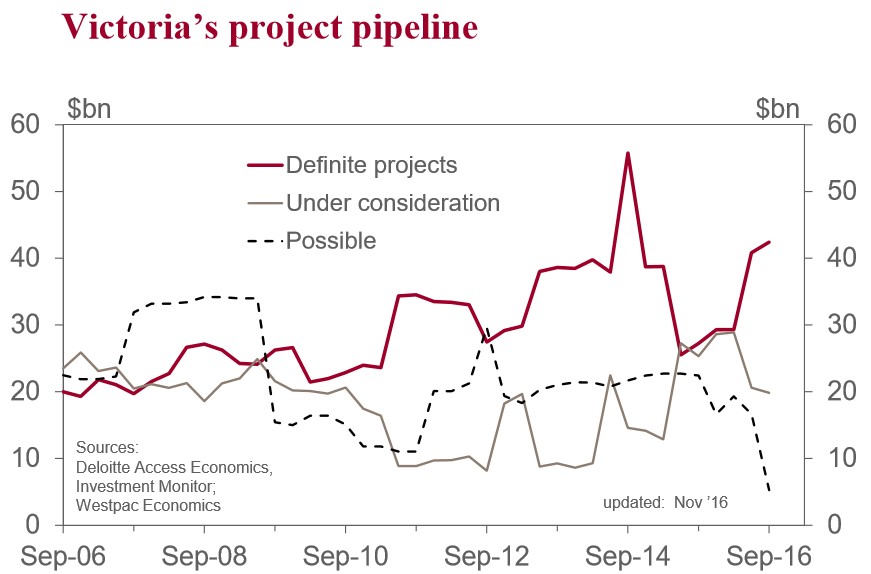

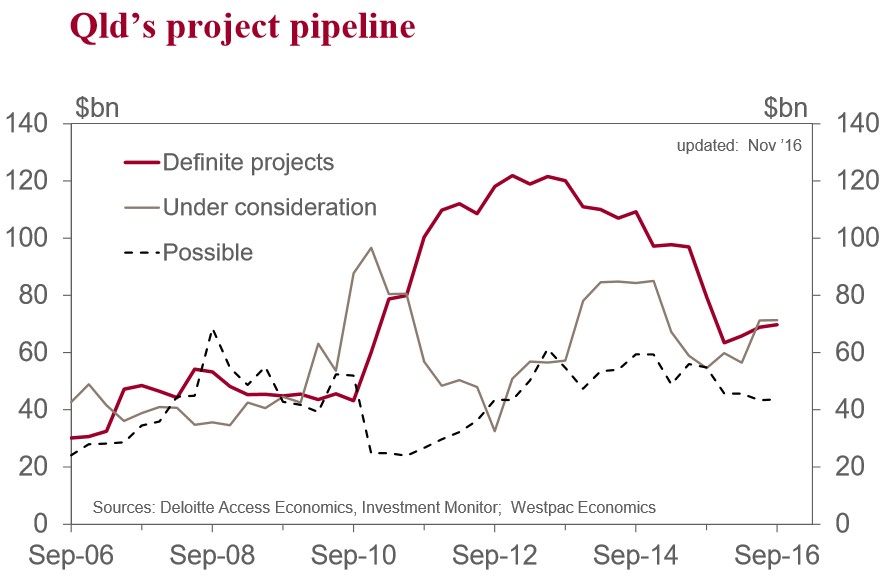

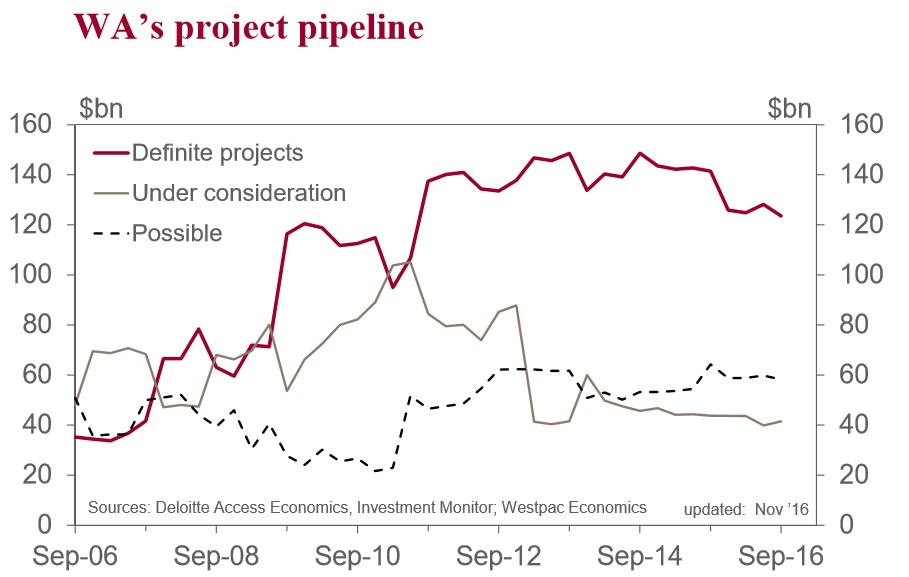

State by state, there is a stark divide. The mining investment downturn is being felt in Qld, WA and the NT. While it is the state governments in NSW and Victoria, which are benefitting most from the housing boom, that are leading the way on public investment.

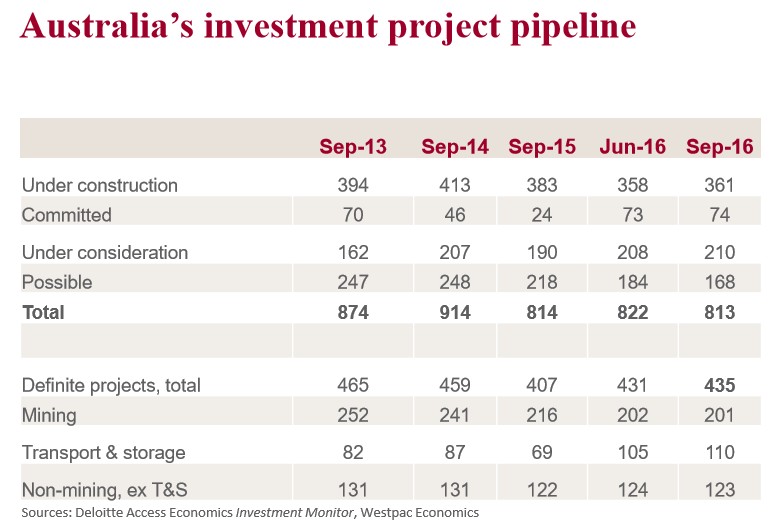

Australia’s investment project pipeline was $812.8bn in September 2016, as reported by Deloitte Access Economics in their Investment Monitor. The database includes 1,102 investment projects valued at $20mn or more.

This is $9.7bn lower than three months ago. Projects completions were worth $6.8bn in the quarter, while project deletions were $18.1bn, including the cancelling of the ‘possible’ $12bn Port Hastings development in Victoria.

44 new projects were added to the database, with a value of $6.3bn.

Cost revisions added $8.9bn, including WestConnex, which increased to $16.8bn from $11.5bn following an updated strategic business case.

The value of definite projects (under construction or committed) increased to $434.7bn in September, +$3.6bn on June and $28.2bn above a year ago.

Note, the Wheatstone LNG project, valued at $29bn in the database, has reportedly experienced a cost blowout of $6.6bn.

Note: the database includes the full value of a project until it is completed or deleted. This differs from the ABS notion of the ‘work pipeline’, which is the value of work yet to be done on projects currently under construction.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.