WA bust drives mortgage arrears to new highs

From Moody’s:

Moody’s Investors Service says that delinquencies for Australian auto loan asset-backed securities (ABS) and residential mortgage-backed securities (RMBS) increased over the eight months to August 2016 as well as year-on-year.

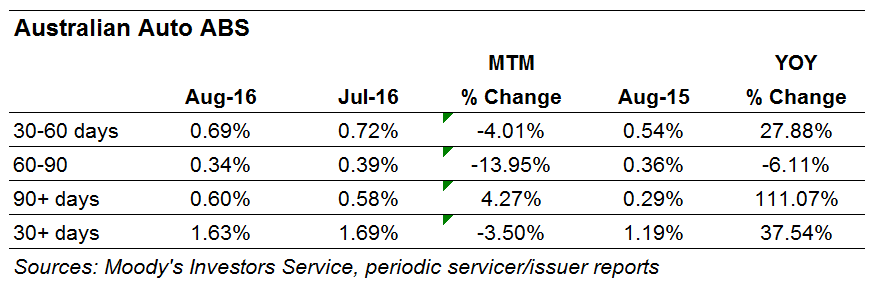

Specifically, 30+ day delinquencies for auto loan ABS transactions rose to 1.63% in August 2016 from 1.35% in January 2016 and 1.19% in August 2015.

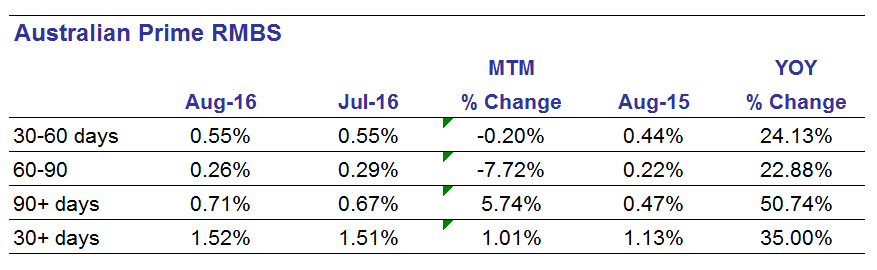

Delinquencies for prime RMBS transactions rose to 1.52% in August 2016 from 1.35% in January 2016 and 1.13% in August 2015.

“Looking ahead, we expect that delinquencies for Australian auto loan ABS and prime RMBS will rise slightly over the remainder of 2016, because of below-trend nominal GDP growth,” says Alena Chen, a Moody’s Vice President and Senior Analyst.

In addition, Moody’s semi-annual study of RMBS delinquency rates — which compares the performance of residential mortgage loans on a state, region, and postcode level — shows that delinquency rates have increased across all Australian states.

In Western Australia, Tasmania and the Northern Territory, the 30+ delinquency rate climbed to the highest levels since Moody’s records began in 2005, while in South Australia, the delinquency rate was just 0.1 percentage point below the state’s record-high reached in April 2013. The 30+ delinquency rate in New South Wales also increased 0.04 percentage points, but at 1.05%, delinquencies remained at an historically low level for the state.

And the charts:

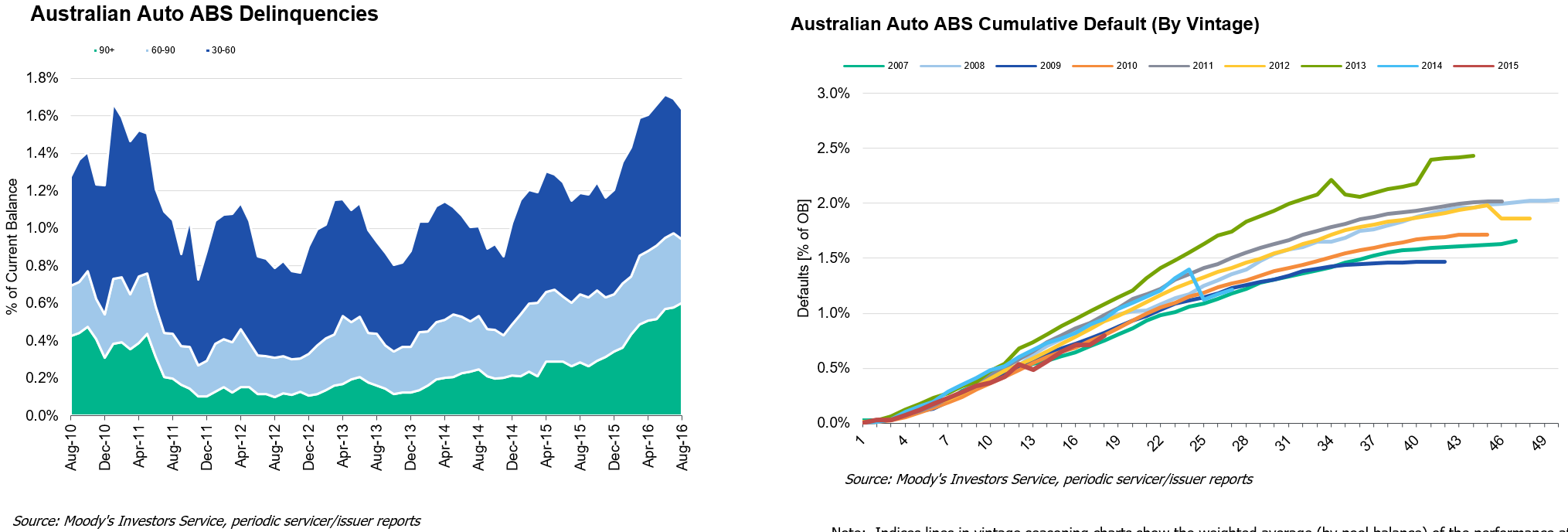

Note the 2013/14 vintage spikes. They have WA written all over them. In seasonal terms, it is quite unusual for arrears to keep rising all year. We an expect another big spike in the New Year to challenge the GFC highs.

Meanwhile auto loan delinquencies are further along given they are non-revolving with fixed interest rates, offering a truer picture of underlying stress:

I expect RMBS to follow ABS to GFC highs in due course.

It’s not disastrous by a wide distance but the trends are bad enough to keep pressure on bank earnings growth, especially anyone with WA exposure (hint, hint CBA).