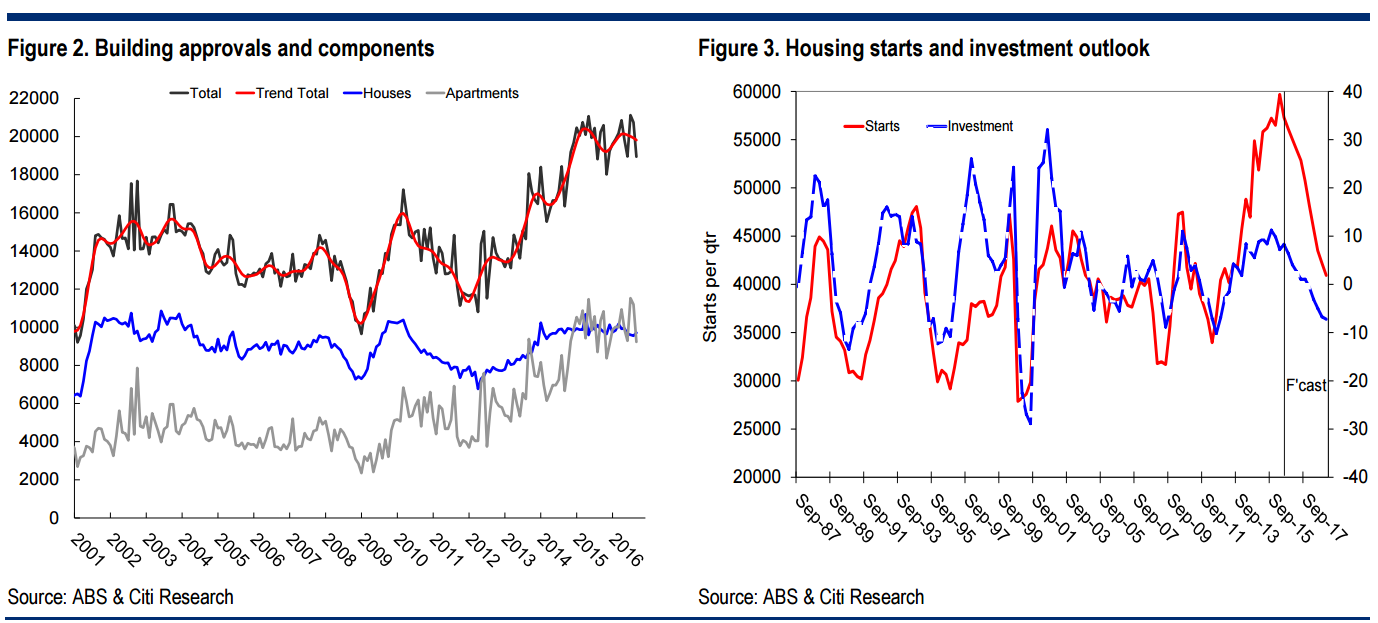

Building approvals sank by 8.7% in September, almost three times the expected consensus decline but close to our forecast of -8.0%. All of the headline fall was from an unraveling of previous apartment strength, down 16%. This shouldn’t have been a surprise. The previous strength was never sustainable as we highlighted in our research on apartments titled Apartment Oversupply: When, Where and How Significant / Equity Market Implications. The headline fall would have been larger if not for a 2.3% increase in private house approvals. Regardless, the number of approvals in the month was close to 19k, which remains elevated when compared to historical levels (Figure 2).

Signs of a downswing. The super cycle in housing starts has peaked but the high level of apartments that are approved but not yet started, the August rate cut and a possible further easing will support activity well into next year. Indeed, apartment oversupply is already apparent in several key postcodes in Melbourne and Brisbane with re-sales only being achieved with lower prices. However, underlying housing demand appears sufficiently strong to prevent contagion across the broader housing market. In September, we lifted our forecast for housing starts this year to close to 230K, a record, with a projected decline to 205K next year and 170K in 2018 (Figure 3). Taking into account expected moderate growth in renovations and the lower construction value per start due to the high share of apartments, we anticipate dwelling investment to contribute slightly to economic growth next year despite lower housing starts.

Non-residential investment spending increased strongly. Up by 119%, this mostly reflected a large increase in private sector building in NSW, followed by VIC. But these numbers are volatile and we still don’t expect the pipeline of investment projects in these states to outweigh the drag from previous strong mining investment for a few more years.

That is a quite sensible assessment. Although the big decline is not until 2018, growth impacts will fade next year to next to nothing on the high construction plateau. Remembering that capex-led growth adds nothing if it is not building more than the year before, no matter how large the amount.

The 2018 crash is looking formidable. As Morgan Stanley recently noted, it could cost 200k jobs, the same scale as the mining investment cliff. Although the dollar value of the mining crash is much greater, the employment and local production intensity of the dwelling construction boom is much higher.

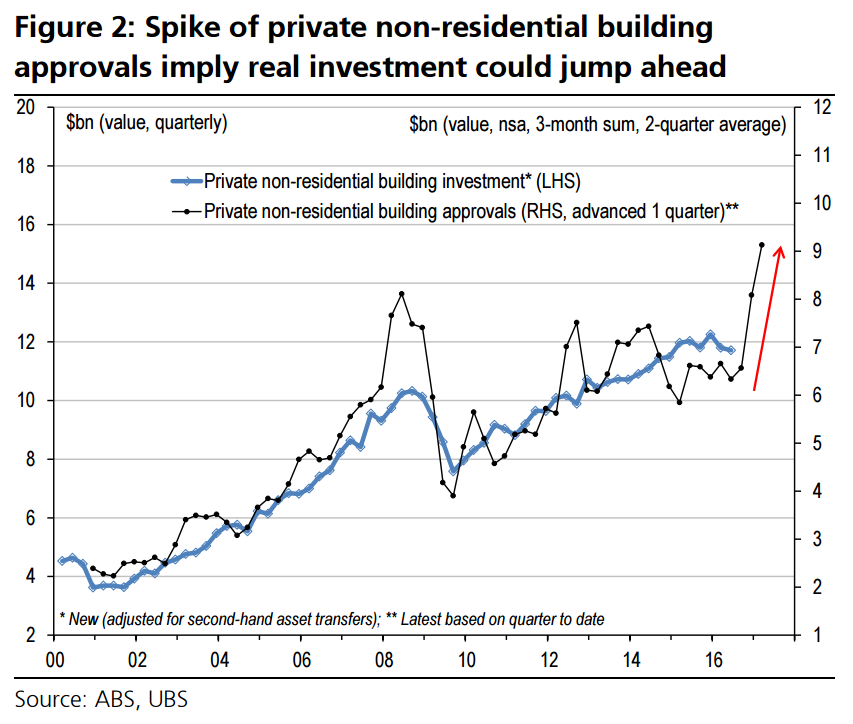

As Citi notes, there is one offset coming in the public investment boomlet, chart from UBS:

Advertisement

But it can only mitigate not offset the much larger dwelling boom draw down.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.