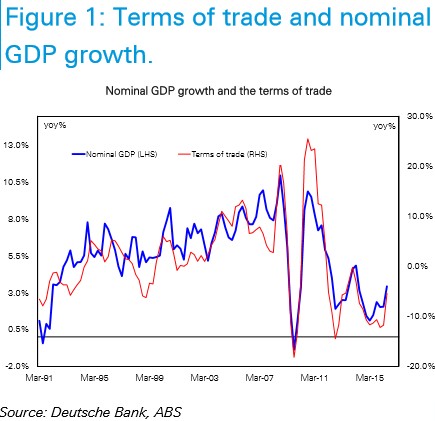

From Deutsche Bank comes a new report looking at Australia’s terms-of-trade bounce and whether it will stimulate the economy:

The surge in commodity prices is likely to see the terms of trade up around 10 per cent through the year come the end of this year and the start of next. As Figure 1 suggests, that could see nominal GDP growth running around 8% over the year – a return to the boom that existed just prior to the global recession. It’s tempting, therefore, to also expect the outperformance that was evident in the labour market around that time to return, with strong wages growth to also lift inflation.

It’s tempting to think that. But we see it as unlikely to happen.

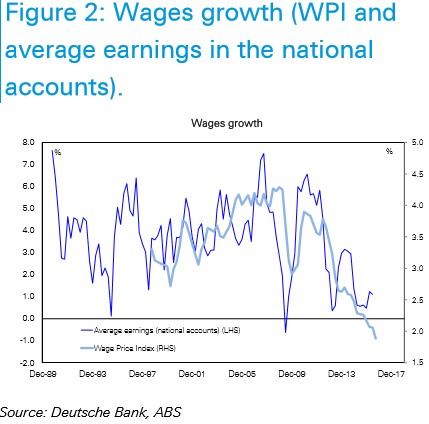

We expect a peak in nominal GDP growth of around 5¾ to 6% come end 2016 / start 2017, before declining to an average of ~4½% over 2017. This reflects: a partial pullback in commodity prices…the considerable weakness in wages growth; and the lack of domestic inflation pressures.

Indeed, for wages growth to hit the Federal Government’s May budget forecast the wage price index will need to start running at an annualized rate of 2¾% over each of the next three quarters, almost a percentage point higher than the annualized pace of growth seen to date over 2016…

So while higher commodity prices will produce a strong increase in the terms of trade and that will boost nominal GDP growth (predominately through higher company profits), the pace of nominal growth will end up being much more modest that the history shown in Figure 1 might imply…

Crucially, we also don’t expect a broader ‘flow-through’ into employment, wages, consumer demand, inflation and real GDP growth from this current increase in the terms of trade. This reflects our assessment that the channels through which commodity price shocks impact the Australian economy are likely to operate very differently this time around. In the first instance we think it unlikely that mining companies respond to the current lift in commodity prices by increasing investment. To the extent that higher commodity prices lift profits, we note that around half of that lift in profits will flow offshore (given the extent of foreign ownership in the sector) and will be reflected in the data through an increase in the net income deficit at the time those higher profits are earned, not when distributions are made. On the employment front we doubt the recent increases in commodity prices will materially change employment trends in the mining sector. In any event, this ‘mining company’ transmission mechanism is not the major channel through which higher commodity prices usually impact the Australian economy.

We have for a while (in fact, around a decade) argued that the public sector plays a key role in ‘transmitting’ terms of trade shocks through to the rest of the economy. During the pre global recession commodity price boom this meant that higher company tax and royalty revenues were handed to the household sector by the Federal Government in the form of income tax cuts and increases in transfer payments. Across the States revenue increases resulted in faster growth in spending…

We have also observed the reverse when commodity prices decline. During the 2015 round of budgets Australian governments generally stopped chasing commodity prices lower (i.e. cutting spending to partly offset lower revenues on account of a falling terms of trade) and instead fully absorbed the impact of a falling terms on trade in their fiscal positions… it is how the Australian economy avoided recession even though iron ore prices slumped from $US140/t to around $US40/t.

…given one ratings agency has put the sovereign credit rating on a negative outlook we suspect there is currently very little desire to undertake a fiscal easing at this point…

With governments therefore more likely to save rather than spend this current terms of trade bounce, and weakness in other elements of the nominal economy suggesting little scope to do so even if they wanted to, we are expecting higher commodity prices to have only a very muted impact on the broader economy (outside of a brief bounce in nominal GDP growth).

Good analysis and similar to the conclusions drawn by Houses & Holes this morning:

…there are good reasons to expect the current terms of trade bounce to have materially lower impacts on nominal growth than previous versions. Corporate profits and government revenue will rise but the spillovers to investment, wages and wider spending will be much more limited. There is no need to build out entirely new commodity supply chains this time. The government will use the windfall for budget repair. And consumers will get some higher mining dividends and share pries and that’s about it.

Advertisement

It’s a very different terms-of-trade “boom” this time around.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.