Amid uncertainty in the wake of the election of Trump to the presidency, Chair Yellen presented a positive view on the economy to Congress’ Joint Economic Committee. The clear implication for monetary policy being that the case for a rate hike “continued to strengthen”, with action to be taken “relatively soon”. Barring a material adverse shock, that means December.

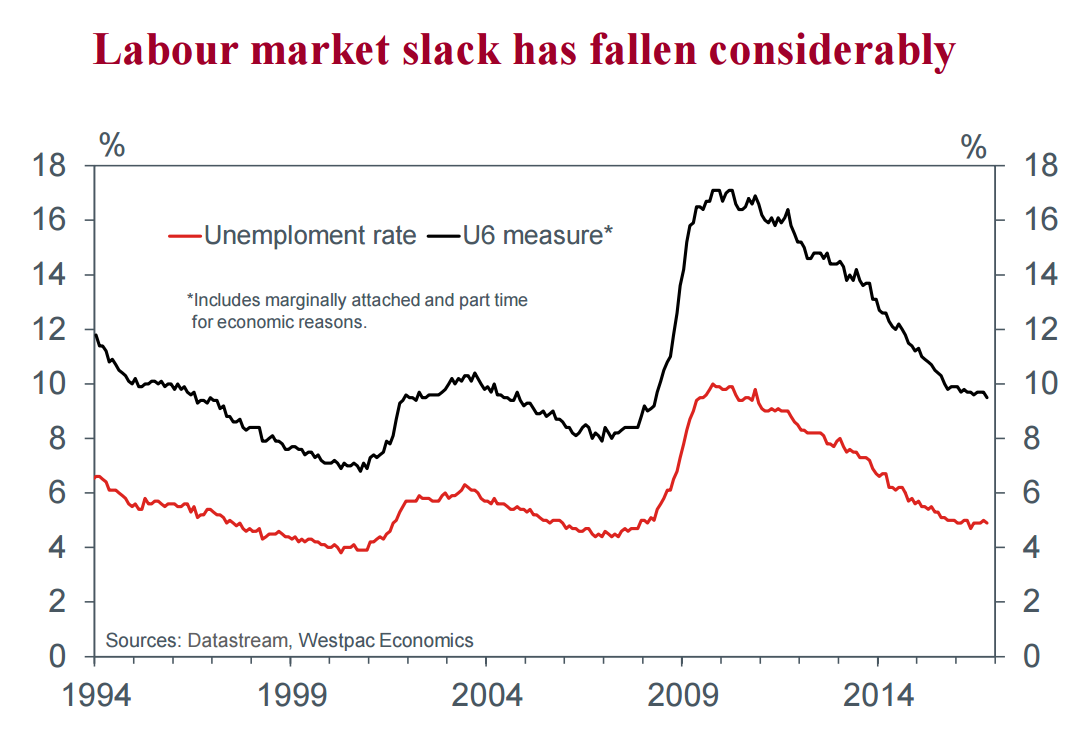

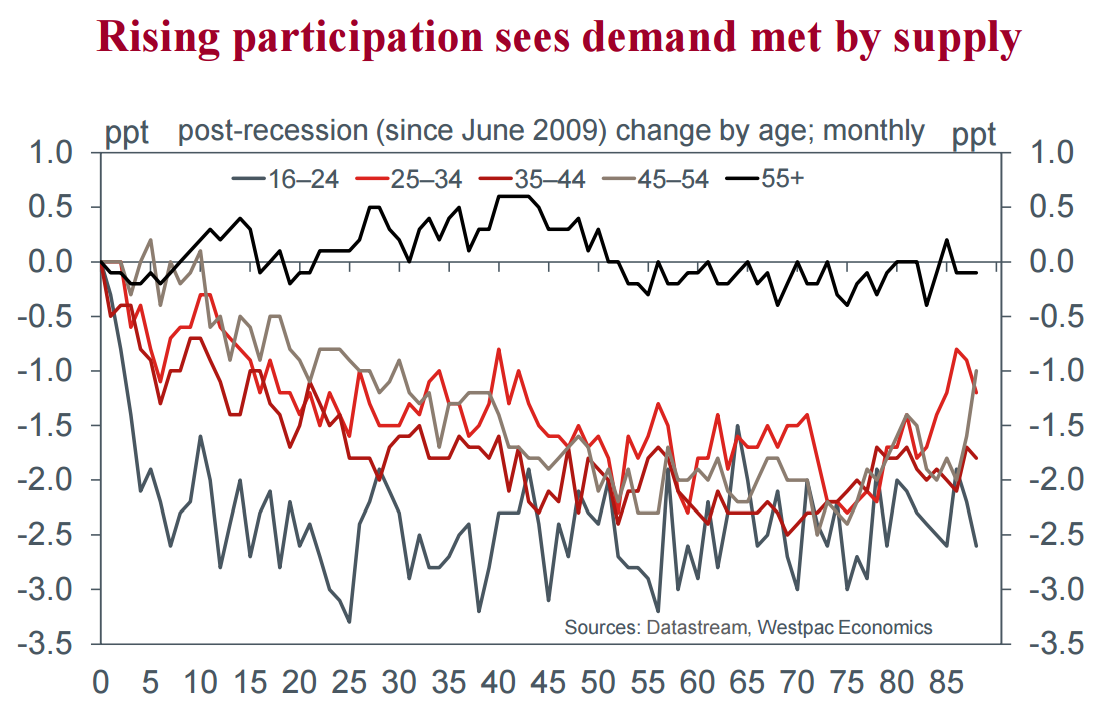

Central to the FOMC’s positive view on the outlook remains the labour market. Their decision to wait “for further evidence does not reflect a lack of confidence in the economy”; rather the Committee believed that “there was somewhat more room for the labor market to improve on a sustainable basis” and wanted to capture that benefit for the economy. The potential for further gains rests on rising participation amongst prime-aged workers (those aged between 25 and 54), allowing labour supply to meet rising demand despite the influence of an ageing population.

The result of this trend has been gains for household income and confidence in the outlook as well as the mitigation of wage pressures which could put the FOMC’s medium-term 2.0%yr inflation target at risk. Arguably the Committee wants to see wage growth firm, but only in a sustainable manner backed by a lasting improvement in productivity.

Just released for October, CPI inflation data highlights that underlying inflation pressures remain robust but contained. The past year has seen core inflation remain a little above the 2.0%yr medium-term target, with services inflation (particularly the shelter component) the driving force. This is not to say that there is a need for rapid action on policy, but rather that gradual increases in the Federal Funds rate are prudent to manage the balance between demand and supply and therefore inflation.

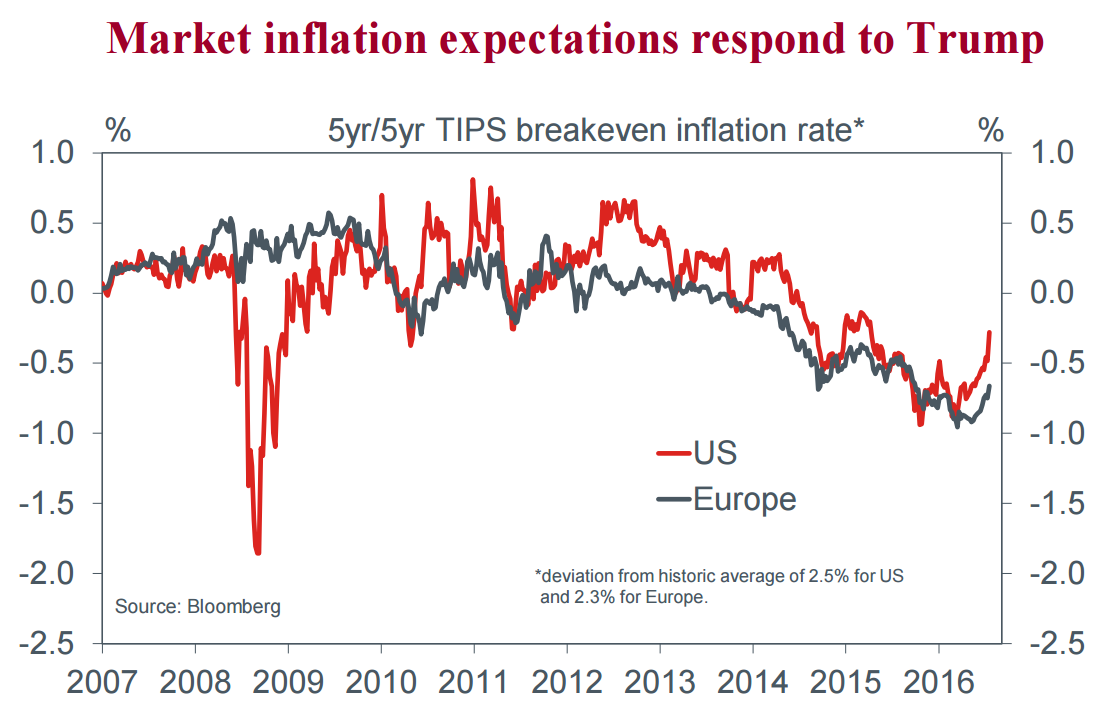

A topic not discussed by Chair Yellen, but one that will likely gain significantly more attention ahead, is the impact inflation expectations can have on term interest rates. While the market has only priced in the December hike and a circa 60% probability of two further hikes in 2017, term Treasury rates have jumped higher in the wake of Trump’s victory. As we saw in 2013’s taper tantrum, sharp increases in term interest rates can shock the economy, particularly housing and business investment, and result in an unwanted slowing in economic growth. This is a potential risk that the Committee must guard against, one that calls for considered and clear policy actions to guide expectations.

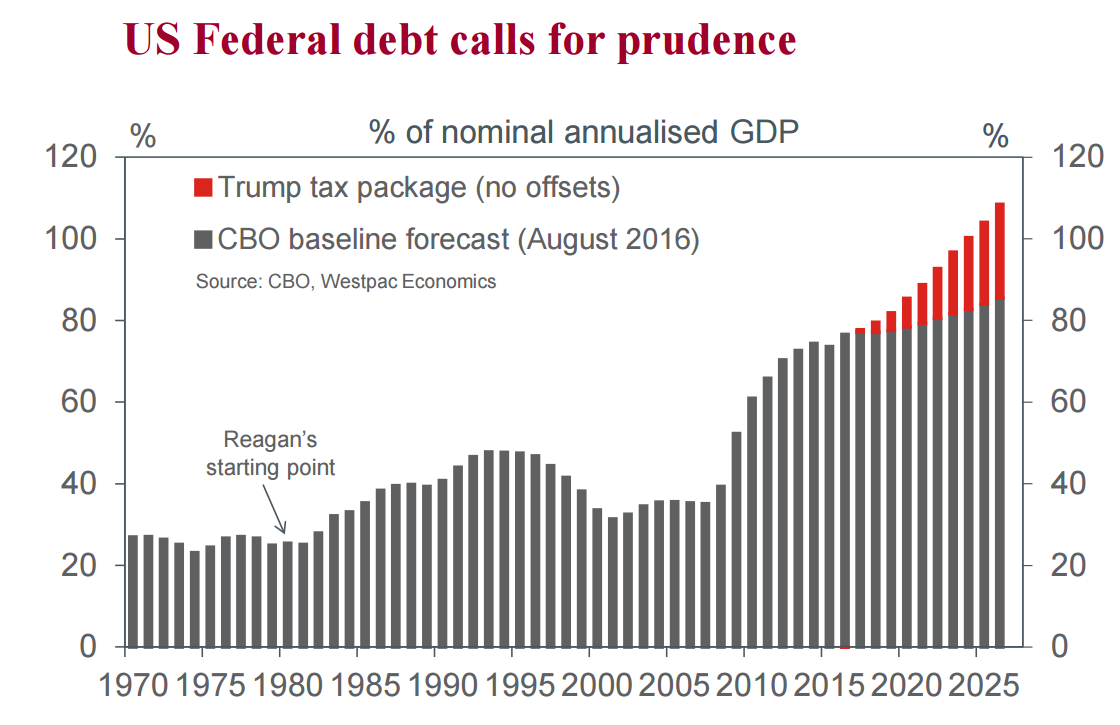

Turning then to fiscal policy, there was little in Chair Yellen’s prepared remarks, but a few comments from the Q&A are worthy of discussion. First Chair Yellen emphasised that, with the economy at full employment, a large scale fiscal intervention to spur growth is unnecessary (and we might add potentially destabilising). Rather the focus needs to be on productivity and developing the long-term growth potential of the US economy. Chair Yellen also raised the issue of long-term debt sustainability and maintaining scope to support demand in the future, should a negative shock occur.

With interest rates set to remain at historically low levels and given the US’ existing stock of debt and other liabilities (pension and health benefits to an ageing population), there is a need to maintain capacity in case growth disappoints and puts the recovery at risk.

All told, Chair Yellen’s perspective is in line with our own and calls for three hikes to end-2017, beginning in December 2016. Fiscal policy could create concerns vis a vis inflation, but this will only be known in time. Indeed it is likely that considerable uncertainty will remain around fiscal policy for a protracted period.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.