The little boom we’ve had in the NAB business survey is over. This significant to the extent that the survey is biased towards the eastern services economy so it indicates that the offset to the mining downdraft is slowing:

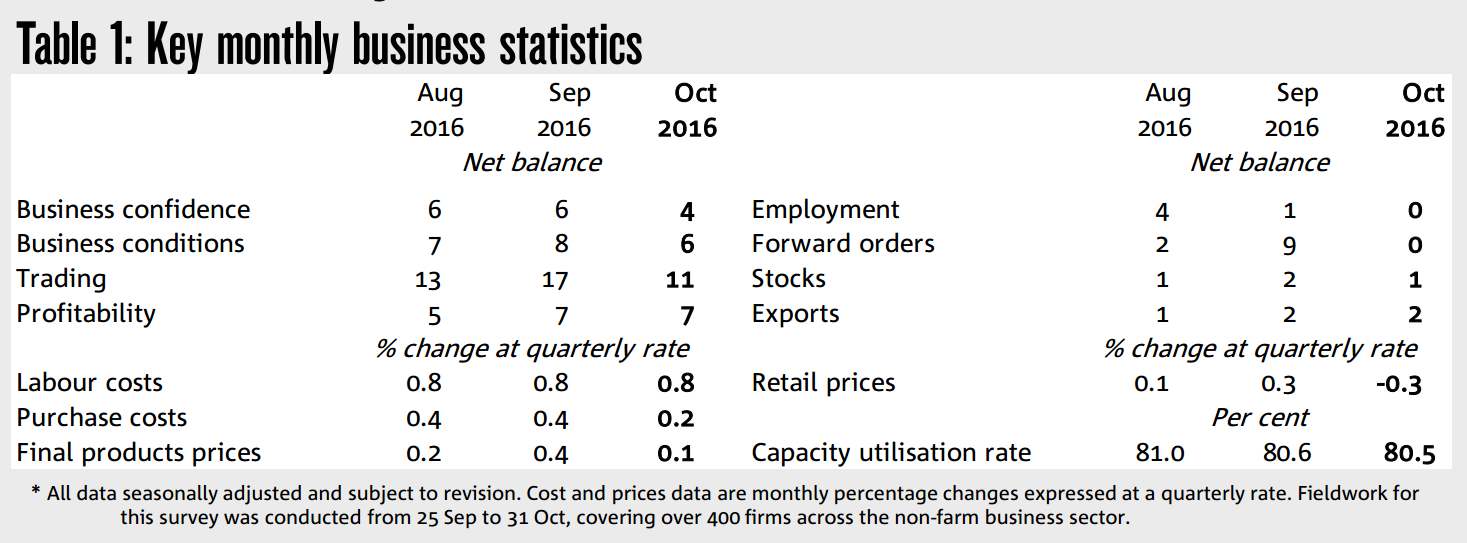

The NAB Monthly Business Survey is now suggesting some moderation in the non-mining economic recovery, with the aggregate level of business conditions (a combination of trading, profitability and employment conditions) dropping in October – the trend has also steadily eased from its most recent peak in May. Despite the subdued trend, business conditions remain at above average levels and business confidence has been tracking broadly sideways for some time – albeit easing in the month as well. In October, the business conditions index fell 2 points, to +6 index points, which is slightly above the long run average of +5. There was a narrowing in business conditions across industries in the month, although this was partially the result of a deterioration in conditions for the best performing (services based) industries. However, a noticeable improvement in retail conditions was encouraging, although the trend remains quite soft. By component, both trading and employment conditions deteriorated – although the former remains elevated – while profitability was steady. Inflation measures in the Survey have been subdued and generally moderated further in the month.

• Business confidence has proven to be relatively resilient this year, but did moderate in October – falling 2 points to +4 index points (below the long-run average of +6). While we would like to see confidence at higher levels as a precursor to stronger non-mining business investment, this could still be interpreted as a solid outcome, particularly given the global political uncertainty ahead of upcoming elections. However, other leading indicators were not encouraging either, with forward orders falling significantly, while capacity utilisation – of relevance to future employment and capital spending – eased further.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.