by Chris Becker

Press the buy button, go have lunch, press the sell button. Repeat. Trading the US presidential washup is getting a little too easy, as US markets make new highs and the wave of positive sentiment lifts Asian shares as well. The only fly in the ointment so far is a slight blip up in Aussie dollar after being so oversold post-election as the USD soars against, well, everything.

The Shanghai Composite is having a breather today, down a few points after lunch at 3246 points but still on its way to my target at 3400. The Hang Seng is doing slightly better, up only 0.15% to 22704 points, trying to make headway after its breakout of its downtrend yesterday.

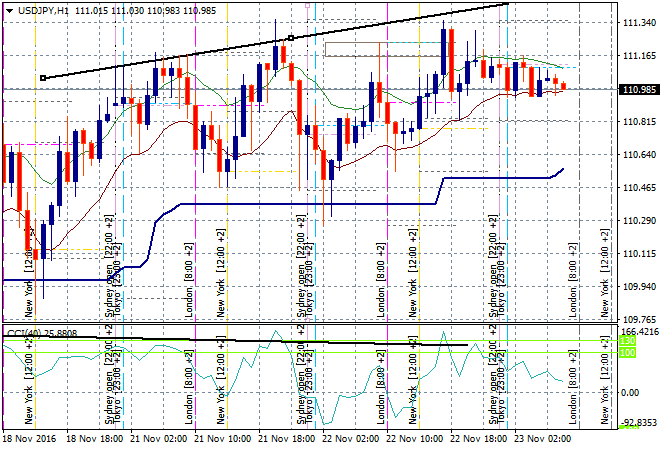

In Japan, share markets are closed for Labor Day and this has also seen a boring day in Yen trading, with the USDJPY pair hovering around the 111 handle:

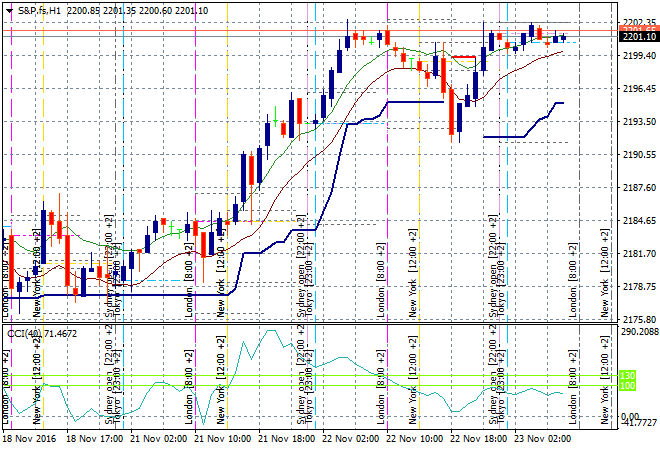

S&P Futures are back where they started in the previous session heading into the European open with 2200 points remaining firm here. Tonights durable goods order might put a dent in this rally if it falls short:

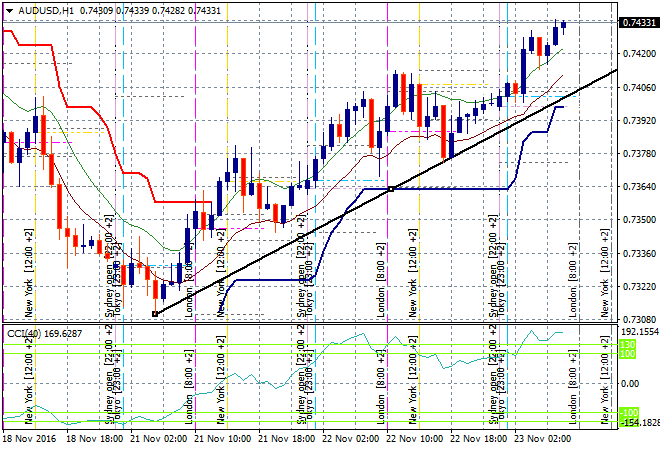

Meanwhile, the ASX200 is having another stonker of a day, up 1.3% to 5484 points, nearly up to my target at 5500 points. Both banks and miners (i.e the entire market) are doing the heavy lifting today as short positions are squished.

This action is rhyming with the rise in Australian dollar, which has rallied through to 74.30 against the USD and higher against Yen too. Resistance at 74.70 is my target here and on the hourly and 4 hourly its a little overdone, so a pullback is to be expected:

The data calendar ramps up tonight with quite a few releases to watch, starting with a slew of preliminary manufacturing PMIs from Europe and Germany, followed by a one-two punch for Pound traders, the UK budget statement and US durable goods at the same time. We also get initial jobless claims and US house prices later in the session.