by Chris Becker

A more positive end to the week in Asia with gains across most stock markets, save mainland Chinese, as the USD continued to surge against the majors after hawkish comments from the Fed Chair last night.

The Shanghai Composite is down a few point just after the long lunch break and looks set to close just above 3200 points again, while the Hang Seng is doing a lot better, up 0.25% to 22310 points. It’s still trying to get out of its corrective phase and this little blip is not yet enough, but price momentum is promising.

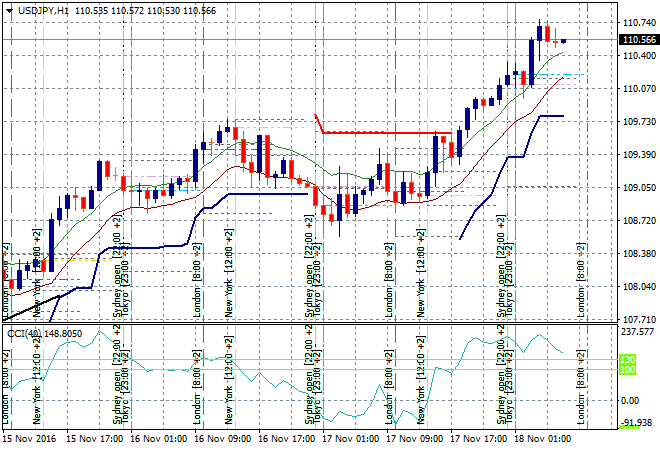

In Japan, the Nikkei followed the bullish overnight futures, up nearly 1% to 18000 points even as Yen continues to sell off. After breaching the 110 handle overnight, USDJPY tried for 111 but remains stable here at 110.55 going into the London session in a move that is looking extremely overbought and above my previous target:

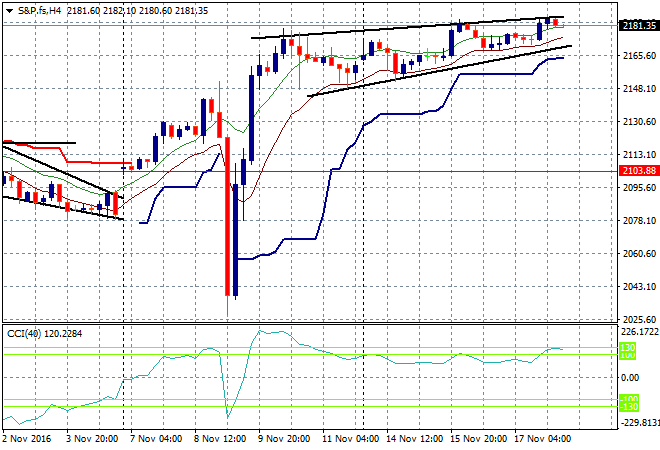

S&P Futures are down slightly heading into the European session where I’m watching this possible bearish rising wedge pattern to break either side of those trendlines as the earnings season wraps up. The bulls remain in charge post Trump:

The ASX200 is up modestly, closing around 0.3% higher to 5351 points in a second positive session as support builds. Resistance overhead at 5400 points is still too high a target for mind though unless the Aussie dollar sells off further.

And indeed, the Pacific Peso, after breaking down from support overnight is selling off once more and now below 74 cents against the USD. Its steady against Yen, but this is setting up for another re-weighting of interest rate risk with 70 cents or even lower on the cards:

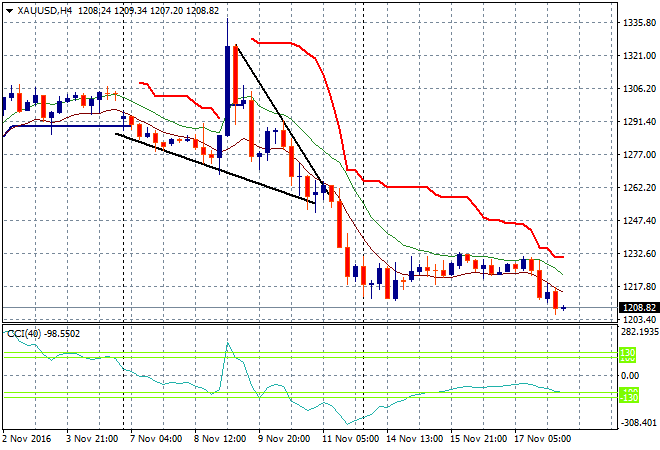

Gold is following the same trajectory, falling nearly $7USD per ounce in the Asian session and now below its start of week low, which presages further falls later tonight:

The data calendar finishes the week tonight with a speech by Mario Draghi in Frankfurt, followed by a few other wonks and Fed officials that may move currencies slightly. In releases we get Canadian CPI and the Baker Hughes oil rig count that will probably have little impact on crude.

Have a good weekend and see you on Monday for my Trading Week report.