There is no doubt that Australia is experiencing a worsening problem regarding housing affordability…

The driver of reduced affordability has clearly been the rapid increase in the price of housing, relative to a more benign adjustment in household incomes…

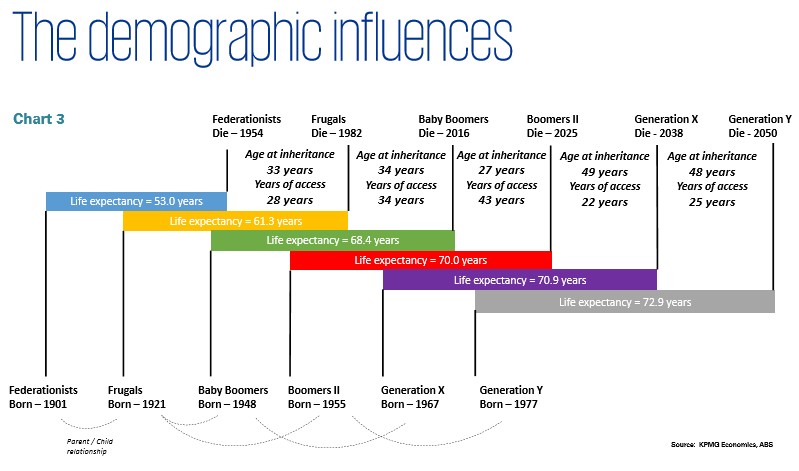

Average access to intergenerational equity – being the average amount of time a generation has access to potential wealth via inheritance from the immediately preceding generation – is anticipated to be greatest for ‘Baby Boomers’, and least for ‘Generation X’…

In the context of housing affordability, family wealth which has traditionally been inherited by successive generations and is often utilised for investing in dwellings, is therefore not being accessed by current generations as readily.

This point is particularly relevant for people who need to save for a deposit to purchase a property. If house prices are growing more rapidly than wages, then a potential purchasers ability to save the minimum deposit – which is expressed as a percentage of the house prices – becomes harder and harder. So access to intergenerational family wealth becomes more important in these circumstances.

Further, as ‘Baby Boomers’ live longer, and potentially draw down on the equity of their housing investment to fund their retirement, it is also likely that ‘Gen X’s’ will not only access family wealth relatively later in life, but it may also be of lesser value, relative to the inheritance ‘Baby Boomers’ received from their ‘Frugal’ parents….

We are now seeing a change in behavior by current generations regarding home purchasing which is new compared to previous generations. That is, some young people are now collaborating to buy, some are assisted by parents, while others are simply choosing not to buy…

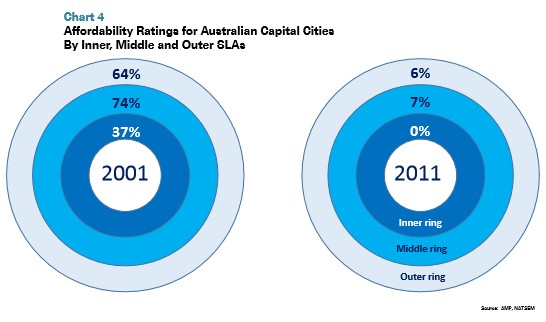

Low income households are only able to afford housing stock that is located on the fringe of cities, and even then this has become more difficult. However, this outwards push of the urban fringe also creates broader issues for society around provision of infrastructure into these ‘greenfield locations’, and the false economies associated with cheaper housing but more expensive private and public transport…

KPMG recognises the challenges associated with resolving the problem of housing affordability are complex and they involve a range of both supply and demand side factors. We have offered a number of solutions that provide a way forward for housing affordability to be improved on a permanent basis. These include:

1. CGT reduction: reducing the capital gains tax discount from 50% to 25%, thereby making property investment marginally less attractive

2. Aggregate property tax: abolish stamp duty on the transfer of residential property and conflate rates, land tax, insurance taxes and emergency service levies into a new Property Services Tax

3. Systemic reforms aimed at maintaining the supply and diversity of land and housing in established and growth areas, through:

a) Set targets: a stronger role for target setting for “net additions to stock” to drive Local and State Government planning schemes;

b) Affordable product: target setting would also focus on encouraging greater diversity of housing stock and deliberately encouraging smaller, well designed affordable products;

c) Streamline planning: making further improvements to the planning system to capitalise on the Government’s planned use of structure plans as a means of reducing the holding costs associated with planning delays – and providing developers in both the private and public sector with greater capacity and incentives to bolster supply at times when the market is under substantial demand pressure;

d) Empower public supply: supporting a stronger role for government land authorities to focus on housing affordability for middle income households within the context of a broader sustainability agenda.

4. Targeted Reforms aimed at improving access to those groups who are the most excluded from affordable home ownership. This package would focus on:

a) More low cost housing: the production of a greater volume of more sustainable, well-designed, lower cost house and land packages;

b) Improve assistance: better targeting of existing State first home owner assistance to increase the overall value and impact of that assistance;

c) Promote shared equity: the introduction of a shared equity program with a percentage of that equity exempt from rental interest charges for the life of the loan or a part of it to be provided by Government and/or the private sector.

KPMG also believes that the solution for Australia must involve all levels of Government working together, given the factors driving the problems are not under the remit of any one level of government. It should be a priority area of public policy.

While there is nothing ground breaking here, it is good to see KPMG focus on both demand and supply-side reforms, including fundamental reforms to the property tax system.

KPMG’s call to halve the CGT discount is particularly pertinent as it flies in the face of the Coalition’s stance of maintaining existing tax settings. It also follows similar recommendations from Deloitte last year, which called for the CGT discount to be pared-back:

Advertisement

Our conclusion? The current CGT discount is too generous, to the extent that it undermines the very principles of this nation’s progressive personal income tax system. It’s time for a change. Reform of the concession is long overdue.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.