1. The referendum is not a make-or-break moment for Italian politics. Although important, near-term risks stemming from the referendum outcome may be overstated. A No vote would maintain the (perhaps not ideal, but wellknown) institutional status quo, although it could lead to government resignations. We reckon on balance the reform is positive for Italy’s future political stability and ability to implement reforms, but experts’ views, which are increasingly diverging on its merits suggest that investors should be cautious in drawing firm conclusions either way.

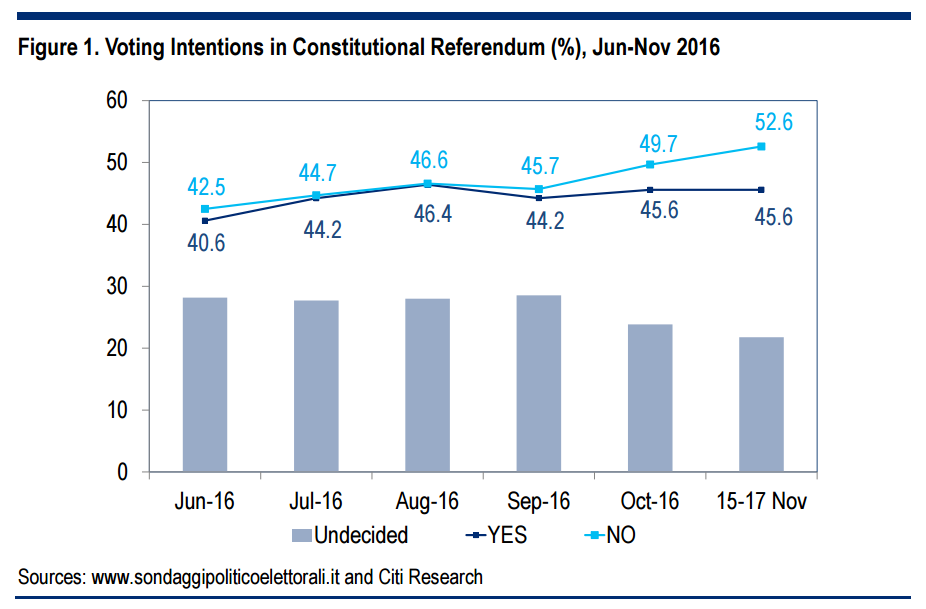

2. Opinion polls clearly point to a No outcome, risks may be skewed the other way. The average of 11 polls before the blackout started (Fri 18 Nov) showed support for No at 52.6% vs 45.6% for Yes (Figure 1). The 7pp-lead is just outside the margin of error of most polls (+/- 3pp). The trend over the past month has been in the favour of No, alongside a small decline in the share of undecided – and the most undecided are centre-right/right voters, whose party’s official position is for a No vote. However, (i) the share of undecided among those intending to vote remains high, at 20-25%; and TV programmes may have more influence on undecided voters than their party’s position.2 (ii) The ballot question is a clear Yes-answer for many Italians.3 (iii) Most polls are conducted via fixed-line phone calls; the only online poll to our knowledge by Termometro Politico (fieldwork: 17 Nov) showed a much tighter result (23.3% for No, 22.7% for Yes). Note there is no quorum for the vote to be valid. We keep our base case view that No is the most likely outcome and reckon this is probably also the base case for most investors. The probability of a Yes outcome, though, may be higher than generally assumed.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.