Morgan Stanley comes a breakdown of the ASX poor October:

S&P/ASX Indices fell through October with broad weakness across industrial sectors offsetting gains across Materials and some recovery in Financials. Further Resources earnings upgrades saw consensus FY17 EPSg edge up to +8.6%, helping bring the ASX 200 multiple back to 15.5x.

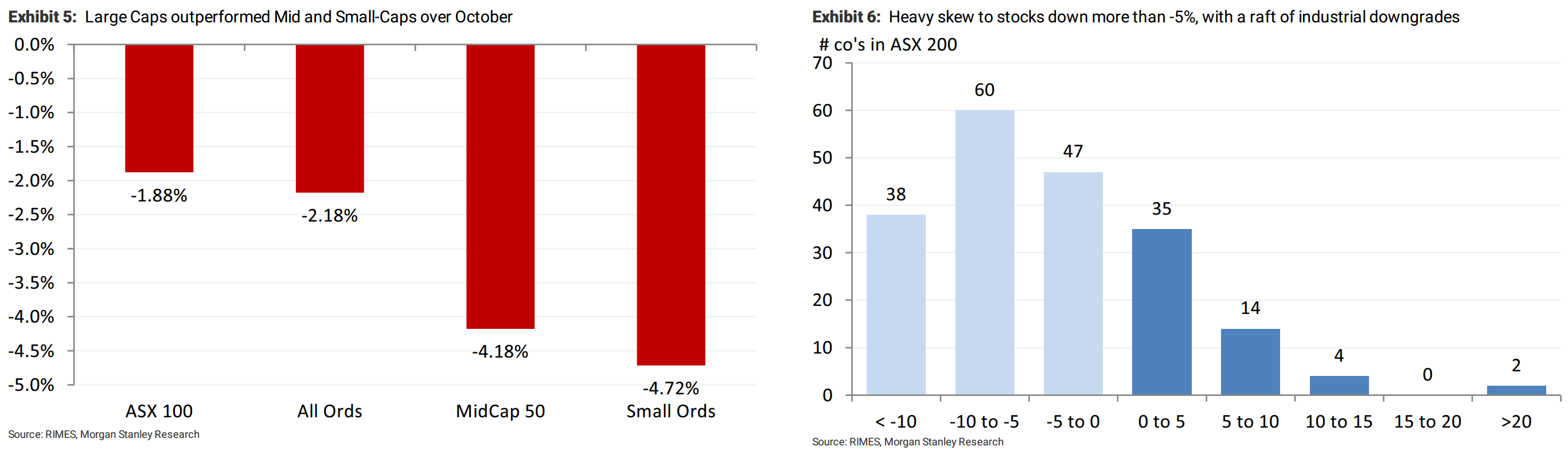

Australian equity market returns (ASX 200) continue to oscillate between up/down months overFY17, closing October at 5,318 (-2.2% TR). Large caps pulled one back, but the real story was continued earnings and price momentum for the Resources sector. Meanwhile,an unwind of bond proxy valuations played out through the month, with Real Estate and Utilities proving significant laggards. Health Care was the worst performing sector, with HSO falling ~28% (detracting 10 bps) following lower-than-expected hospital revenue growth in its recent tradingupdate, while CSL detracted a further 21 bps.

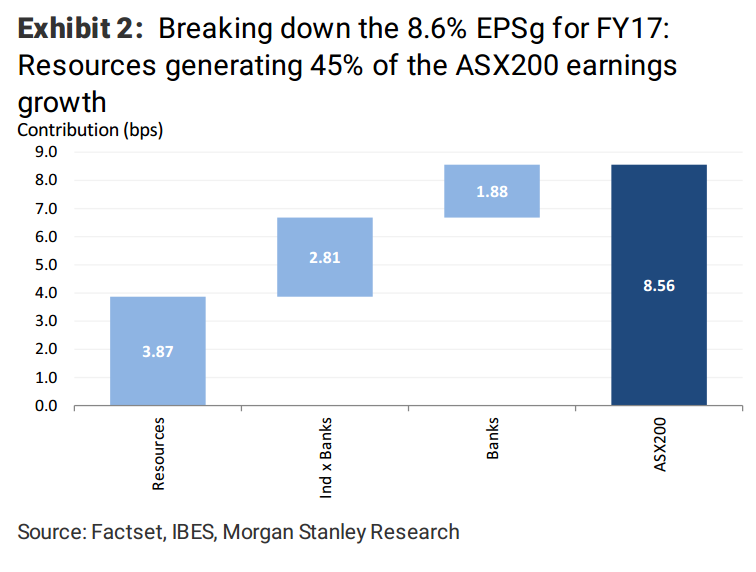

FY17 EPSg now at 8.6%; FY18 lower at 7.2%. The latest IBES consensus aggregate EPS growth estimate for FY17 now sits at 8.6% (previous month-end +7.8%), largely a reflection of the continued positive earnings revisions within the Materials sector, with FY17 EPSgup another 2ppt to 39% and factoring a lower (final)FY16 base. Resources account for 45% of the FY17 EPSguplift (see Exhibit 2), with 33% from Industrials-ex-Banks and 22% coming from the Banks. The largest single stock contributor is BHP (+2.4ppt), whilst WES earnings imply a detraction of -0.5ppt.

ASX 200 multiple falls from 16.2 to 15.5x: The combination of a down-month and higher forward index EPS level has seen the 12m-forward mutiple de-rate from 16.2x to 15.5x over the month. Industrials-ex-Financials are now trading below 19x, while stronger earnings momentum has cut the Resources multiple from an April peak of 25x to 18.8x. Materialsand Financials up..but market still down: It is not often that the market falls when

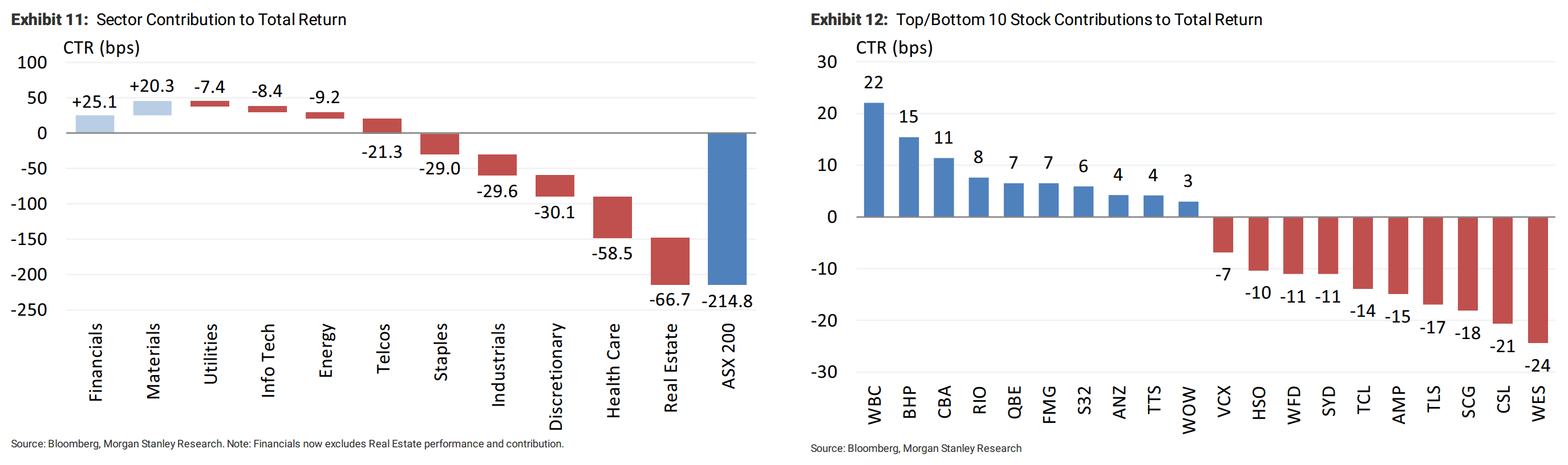

Materials and Financials are up, as was the case in October. Materials momentum added a further 20bp to ASX 200 returns,and a rebound in Financials (+25bp) was offset by negative returns across all other sectors. Most-impacted were Real Estate (-67bp), Health Care (-59bp) and Discretionary (- 30bp). At a stock-level, WBC (+22bp) and BHP (+15bp) were the largest single stock drivers, whilst WES (-24bp), CSL(-21 bp) and SCG (-18bp) were the largest detractors over the month.

Still playing Resources reflation: We continue to recommend a broad-based OW across Materials and Energy. The key drivers of this call remain in place: 1) An earnings upgrade cycle,2) Growth support,3) Underweight positioning,and 4) Improved supplyside dynamics. Our key Model Portfolio positions include BHP, WPLand OSH, with broader mining exposures including RIO, S32and WSA

That last chart is for all of 2016. It clearly shows the shift from the deflation trade of chasing yield to the inflation trade of chasing commodities. I remain of the view that it’s a short term trade and 2017 will see a return to deflation as China eases, commodities fall again and some central banks are tricked into tightening too early.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.