The International Monetary Fund (IMF) has released its Staff Concluding Statement of the 2016 Article IV Mission to Australia, which has once again called on policy makers to curb property tax lurks like negative gearing and the CGT discount:

The macro-financial resilience of the economy to housing market shocks could be enhanced through tax reform . The tax system provides households with incentives for leveraged real estate investment that likely amplifies housing cycles.

This is the third time in the past 14 months that the IMF has called on Australia to curb property tax lurks.

In October’s Fiscal Monitor, the IMF gave a subtle nod to unwind negative gearing and the capital gains tax discount by calling on governments to phase-out tax incentives that encourage the build-up of debt:

Advertisement

Over the medium term, phasing out the debt bias in taxation and penalizing debt financing in those sectors in which the negative externalities are relevant, such as the financial sector, should be considered as part of structural reforms to prevent excessive leverage from building up in the first place…

In last year’s Article IV Report on Australia, the IMF took direct aim at Australia’s tax/transfer system incentives for housing, claiming they incentivise investment in real estate, thus raising demand with “potentially negative implications for housing affordability, financial stability, and equity”:

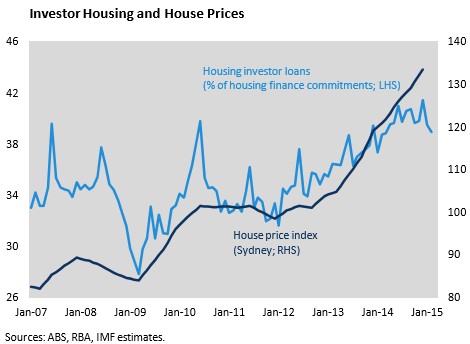

Australia’s tax and benefits system incentivizes investment in real estate. Both owner-occupiers and investors receive significant support through the tax system (Australian Government, 2014). This tends to increase demand for housing, with likely consequences for the real estate market. This in turn has potentially negative implications for housing affordability, financial stability, and equity.

The principal housing-related tax incentives are:

Owner-occupiers. Owner-occupied residences are exempt from CGT. While demand for the overall number of dwellings might be only little affected (since people who do not own homes would have to rent), it is likely to lead to over-investment in housing since this form of investment is taxpreferred (see Australian Government 2014), and thereby drives up the value of dwellings.

Investors. CGT for real estate owned for more than a year is effectively halved, to account for the erosion of real value due to inflation. This is reinforced by the deductibility of interest payments and maintenance expenses from taxable income from other sources (though rental income is taxed), an uncommon feature internationally and among Australia’s peers. While this deductibility is not different from that of other investments, it facilitates ‘negative gearing’. As with incentives for owner-occupiers, it drives up prices, but likely does not trigger a significant supply response, which is largely determined by more fundamental factors such as zoning regulations and infrastructure availability.

The CGT concession for investors and the tax deductibility of net losses on housing investments from other income increase incentives for ‘negative gearing’. When an investor expects capital gains, a property investment may be worthwhile even if rental income does not cover interest costs and maintenance expenses. This effect is enhanced if the resulting loss can be deducted from taxable income, and by concessional CGT treatment. In an environment of rapidly rising real estate prices, the incentives for this form of investment increase, since low-taxed expected capital gains increase. Negative gearing thereby acts as an amplifier of price movements in the real estate market and encourages investment that would otherwise incur ongoing revenue losses. At the same time, however, this tax treatment could subsidize rents, since at a given dwelling price it makes a lower rent acceptable to landlords. However, as it also increases dwelling prices, the net impact is not clear—moreover, if the motivation is to help low-income renters, this can be done much more efficiently (e.g., through direct transfers).

The transfer system also has an impact on real estate investment. When the level of the (meanstested) Age Pension is calculated, the value of owner-occupied houses is exempt from the assessment of assets (Australian Government, 2014). While there is an argument that owner-occupied real estate does not yield an income stream, it encourages investment in real estate, increases Age Pension costs and likely benefits wealthier households. The amount of additional expenditure this generates is difficult to estimate, but could be substantial.

Advertisement

It is also worth pointing out that in February this year, the IMF released its 2015 Article IV report on New Zealand, which recommended the Government quarantine (“ring fence”) negative gearing losses so that they can only be claimed against property-related earnings, not unrelated wage/salary earnings.

The IMF’s assessment is important because it provides a window into what the Treasury and the RBA actually think. This is because the IMF’s assessment is effectively a collaboration between Australia’s chief economic agencies and the IMF authors.

It’s fair to say, therefore, that Australia’s chief economic bureaucrats do not agree with Australia’s housing lurks, and wish to see reform. If only the Coalition Government would follow suit.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.