Former Treasurer Peter Costello continues to whinge about recent reforms to superannuation, complaining that they have increased complexity which he argues is eroding the public’s confidence in the system. From The Australian:

“With growing complexity, extreme complexity, people will shy away from (the super system). And I think they are right to shy away from it because you never know what the rules will be,’’ he said.

Costello then warned that Australia’s credit rating could be downgraded and urged the Government to undertake reforms to strengthen the Budget position:

“I think the prospect of a downgrade can and should be used to galvanise public opinion to know that international people outside Australia are registering concern about our financial position,” he said. “This should be taken as a message to the public that we need to change our ways.”

Mr Costello’s hypocrisy never ceases to amaze. He complains that superannuation is a complex system and people need certainty, as well as the need for budgetary reform, and yet never acknowledges that he made a raft of costly changes as Treasurer that made the retirement system far less sustainable and equitable, costing the Budget billions.

Let’s recall the key deleterious changes to superannuation made by Peter Costello.

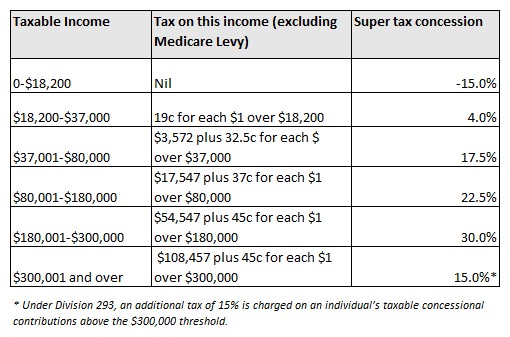

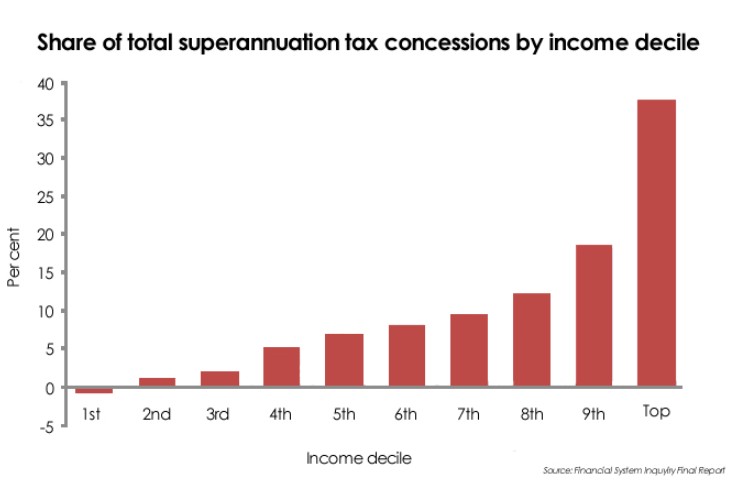

First, in 2005 Costello eliminated the 15% contributions surcharge on high income earners, thus ensuring high income earners received an even greater share of superannuation tax concessions (see below table and chart).

Second, in 2005 Costello also introduced generous ‘transition-to-retirement’ rules, which effectively allowed those aged over 50 to lower their income tax – affectionately described in the industry as the super saver’s version of “having your cake and eating it”.

The Productivity Commission recently slammed Costello’s’transition-to-retirement’ rules, noting that they “appear to be used almost exclusively by people working full-time and as a means to reduce tax liabilities among wealthier Australians” and called for a review of their “efficacy and sustainability”.

Third, in 2006, Costello reduced the tax rate on superannuation earnings for those aged over 60 from 15% to zero – a move dubbed by Saul Eslake as “one of the worst taxation policy decisions of the past 20 years”.

This followed Costello’s decision in 2001 to introduce the “Senior Australians Tax Offset” (now called the “Seniors & Pensioners Tax Offset” or SAPTO), which allowed a couple who has reached Aged Pension age to earn a ‘rebate income’ of up to $28,974 each ($57,948 combined) for the 2015-16 year without paying income tax.

As a result of these changes, younger Australians were required to pay full income tax on their wages/salary earnings and 15% tax on their superannuation earnings, whereas older Australians in many cases paid absolutely no tax.

Indeed, the latest Household, Income and Labour Dynamics in Australia (HILDA) survey, released in July, showed just how inequitable Costello’s reforms to superannuation were. As noted by Professor Helen Hodgson:

The more concerning finding for policy makers is that wealth inequality has increased, and that superannuation holdings and investment properties are factors in this inequality. HILDA data shows that in 2014 the mean superannuation balance of the top 10% of people aged 50 to 69 was $991,268, up from $650,619 in 2002, compared to $210,798 in 2014 for the sixth to ninth decile and $13,719 for the bottom 50% (although a significant number of retirees in this age group do not have any superannuation balance).

There is a strong correlation between high superannuation balances, income and non-superannuation wealth. People in the top decile have access to higher levels of income to make higher levels of concessional contributions, and the ability to find the funds to make non-concessional contributions into a tax preferred investment environment.

As has been noted previously, the current superannuation system allows high income and high wealth individuals to over-accumulate in tax preferred superannuation, which increases wealth inequality as well as intergenerational inequality.

The Government proposals to restrict the level of contributions and to reduce the amount that can be retained in a tax free environment are important tools to address increasing levels of wealth inequality in our community.

We should also remember that Costello greatly loosened the assets test to qualify for the part Aged Pension and the Commonwealth Health Card, thus further worsening the Budget.

It is precisely Costello’s meddling with the retirement system that has greatly worsened the equity and sustainability of the Budget and placed Australia’s credit rating at risk. It is also why Australia’s politicians have had to introduce remedial measures (admittedly too soft) to unwind some of Costello’s largesse.

Peter Costello should stop lecturing us about reform. He has done enough Budget damage already.