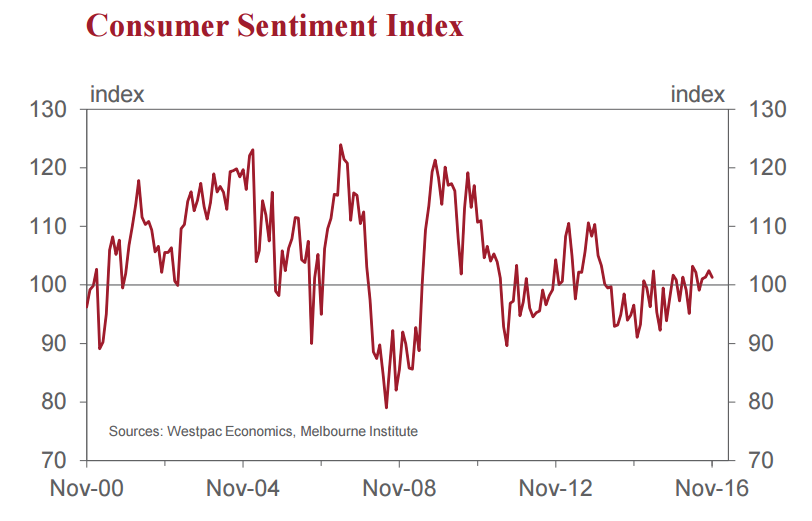

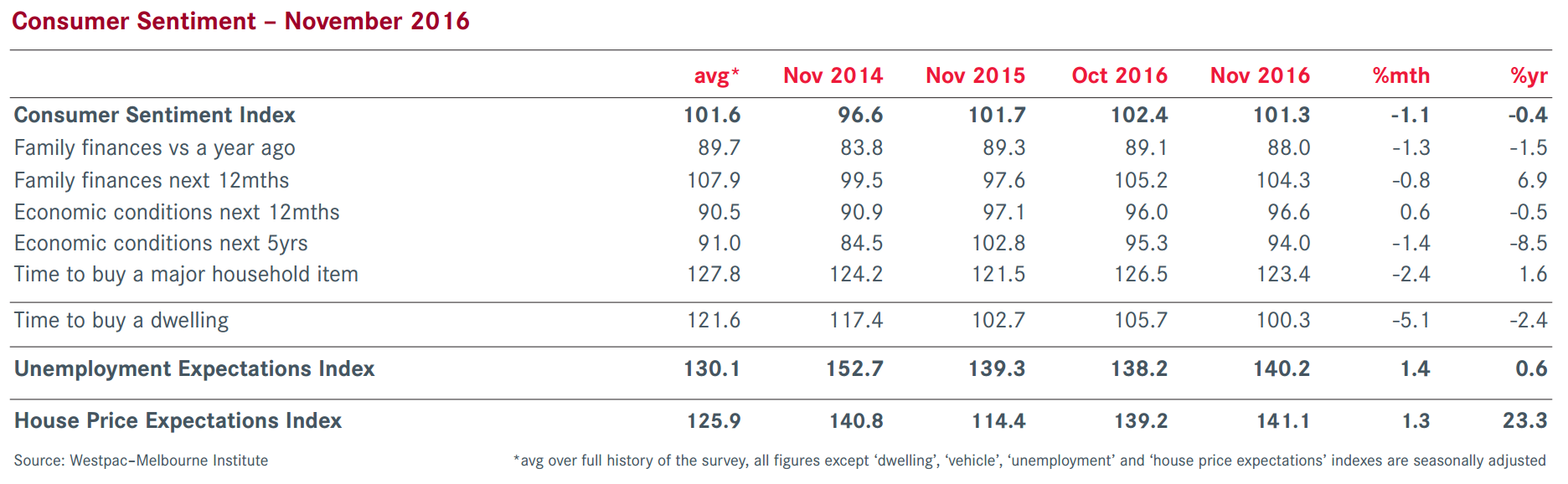

• The Westpac Melbourne Institute Index of Consumer Sentiment fell by 1.1% in November from 102.4 in October to 101.3 in November

The Index continues to hold in a very tight band. Over the last six months the Index has held within the range of 99.1 to 102.4.

However if you compare the average level during this period with the average over the comparable six month period in 2015 there has been a clear lift in the Index of 4.7%. Most of that improvement has been in the components of the Index that measure expectations which are up by an average of 7.3% on last year, whereas the components which measure current conditions have increased by only 1.2%.

Developments of note over the month have included weakness in the share market as investors dealt with the uncertainties around the US election (ASX down by 4.4% since the October survey); a spectacular surge in coking coal prices (spot prices are up around 150% since August); a disappointing jobs report (annual employment growth slowing to 1.4%); and an unchanged rate decision from the Reserve Bank.

Markets had been giving a decent chance to a November rate cut in earlier months so the fall in confidence amongst respondents holding a mortgage of 3.1% was somewhat understandable.

Although down 3.4% in the latest month the lift in confidence in Queensland – the ‘Sunshine and Coal’ state – over the year has been spectacular. The Queensland index has lifted by 15.9% since last November compared to falls in the other major states – NSW (–2.6%); Victoria (–5.4%) and WA (–7.2%).

Disappointment in the jobs market has been signalled in the Westpac Melbourne Institute Index of Unemployment Expectations. The Index rose by 1.4% from 138.2 to 140.2. It is now up by 2.9% over the last six months and slightly above the level a year ago. Recall that higher reads mean more consumers expect unemployment to rise over the next 12 months and hence mark a deterioration.

Four of the five components of the Index fell slightly in the month. Both measures of family finances were down a little – the subindex tracking views on ‘family finances compared to year ago’ fell by 1.3% while the sub-index tracking expectations for finances over the next 12 months fell by 0.8%. ‘Economic conditions over the next 12 months’ increased by 0.6% but ‘economic conditions over the next 5 years’ fell by 1.4%.

In a slight disappointment for the outlook for Xmas spending there was a 2.4% fall in the ‘time to buy a major household item’ sub-index.

In November we traditionally gauge respondents’ Christmas spending intentions. The question is “Do you think that you will spend less, about the same, or more on Christmas gifts compared to last year?” Last year we recorded a net balance – the proportion expecting to spend more minus the proportion expecting to spend less – of minus 13%. This year the net balance has declined to minus 20.1%. That is around the average since we started asking the question in 2009. That is a disappointing result given the promising improvement in spending plans in 2015.

Confidence in housing has also deteriorated. The ‘time to buy a dwelling’ index fell by 5.1% from 105.7 in October to 100.3 in November. We saw significant falls in NSW; Victoria; and Queensland.

Despite confidence in housing deteriorating house price expectations continue to rise. The Westpac Melbourne Institute Index of House Price Expectations increased by 1.3% to be up 23% on a year ago and reach its highest level since July 2015.

The Reserve Bank Board next meets on December 6. There is little chance of any change in rates at this meeting. The key issue is whether the Bank decides to further cut rates in 2017. Whereas lower than expected inflation was the driver of the two cuts in 2016 the decisions in 2017 will be determined by developments in housing and labour markets. Westpac is expecting economic growth and employment growth to lift in 2017 boosted by higher commodity prices; ongoing strong residential construction; and booming exports. While the pace of house price appreciation can be expected to slow the case for lower rates under those circumstances does not seem to be strong.

We expect rates to remain on hold in 2017.

And we expect Bill Evans to be wrong again. The dwelling boom will not add much more to growth (though won’t subtract yet either). The mining capex cliff will continue. The bulk bubble will add little to wages. And booming exports will do nothing for domestic demand. The only upside risk for 2017 is government spending.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.