Donald Trump’s win in the US Presidential election was the second major political event this year to completely wrong-foot the markets, along with the Brexit vote. In the immediate future, we question whether the US Federal Reserve will raise rates in December as well as the outlook for rate rises in 2017. While we’re not going to make too many predictions on the implications of a Trump Presidency, we find it difficult to reconcile the market’s “nothing to see here” pricing of gold and gold equities with the reality of the overturned status quo of politics in the US. In our view, the potential for market volatility, policy uncertainty, geopolitical power shifts and inflation risks have taken a step-change with this election result. In our view, the intra-day moves of the various markets is reflective of the medium term outlook and we think there is more of this to come.

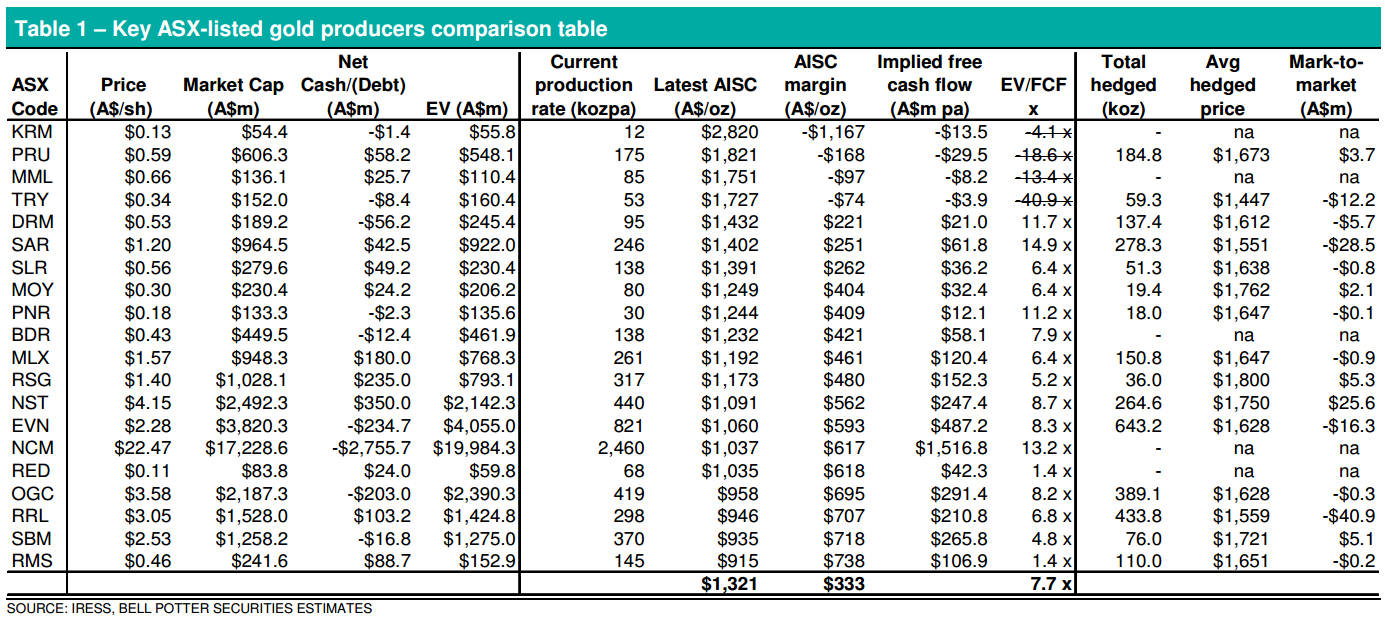

We regularly monitor the gold market and report on it in our Bells Gold Tracker. While we have noted some bearish movements over the last couple of months it has been our conclusion that overall we see market conditions that are supportive of the gold price. Key factors here include negative real interest rates, gold remaining cheap relative to the Dow Jones Industrial Average and bullion ETF’s remaining well held. Combined with the stepchange in the US political outlook, which has global implications, we view this new environment as further supportive of gold prices and gold equities and recommend increasing precious metals exposure in portfolios, via the listed producers in particular. We continue to advocate building a gold equity portfolio around core holdings of low cost, multi-mine producers with strong balance sheets. However, in a rising gold price environment, we would also highlight the operationally leveraged names as becoming more attractive as well. The table below is snapshot of key ASX-listed gold producers following their September quarter production and cost reports. In the context of looking for gold price exposure and leverage we have sorted the list by their last reported AISC and also marked to market their latest hedge book positions.

Of the producers we have under coverage, Regis Resources (RRL) best fits the core holding criteria. Producers offering operational leverage with above median/average All-InSustaining-Costs (AISC) include Metals X, Pantoro (PNR) and Doray (DRM). Of these, we expect material production growth and cost improvements to drive margin expansion and cash flow growth for MLX and PNR in particular. Kingsrose (KRM) is a turnaround story that recently raised fresh equity and its prospects will clearly be helped by a rising gold price. Specifically, for immediate gold price exposure, we would recommend:

• Regis Resources (Buy, TP$3.60/sh);

• Metals X (Buy, TP$2.10/sh);

• Pantoro Limited (Buy, TP$0.24/sh); and

• Doray Minerals (Buy, TP$0.68/sh).

I find this analysis unsettling in its assumption that political instability arising from the Trump victory is enough on its own to recommend gold. It’s not. No matter which policies Trump actually implements in power, the one very obvious conclusion is that the USD is in a bull market as US inflation outstrips the world and Fed is forced to chase it.

That is not a gold friendly environment at all. Indeed, as we saw during the GFC, when the USD really gets moving upwards then its gold that gets moving downwards.

By the same token, Trump policies have also increased the prospects of a relatively swift boom and bust cycle in the US, which will be bullish for gold before long given it will also end with the Fed taking policy into the negative. Moreover, my main reason to remain long gold medium term is Europe, where the Trump victory has steeply increased the dangers of euro disintegration and if that happens then I can see gold going nuts.

Advertisement

This is why on Thursday I suggested that those seeking to make money on gold short term should exit for lower prices but those seeking to use gold as a hedge should get ready to buy the dip.

For the former there is the one comfort that Aussie miners will be hedged by the falling AUD. Especially so once the bulk bubble bursts.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.