THE WORLD’S PRIMARY ENERGY DEMAND GROWTH will slow and per capita energy demand will peak before 2030 due to unprecedented efficiencies created by new technologies and more stringent energy policies.

Since 1970, demand for energy has more than doubled. New technologies to 2060 will keep energy demand growth moderate relative to historical trends, and will help to enable industrialised economies to transition more quickly into service and sustainability-led growth. Efficiency gains will be made through the deployment of more efficient energy resources, combined with the effect of digital technologies that will help to enable smart grids, smart buildings, smart homes and offices, and smart cities. Advanced manufacturing, automation, telecommuting, and other technologies also will disrupt traditional energy systems.

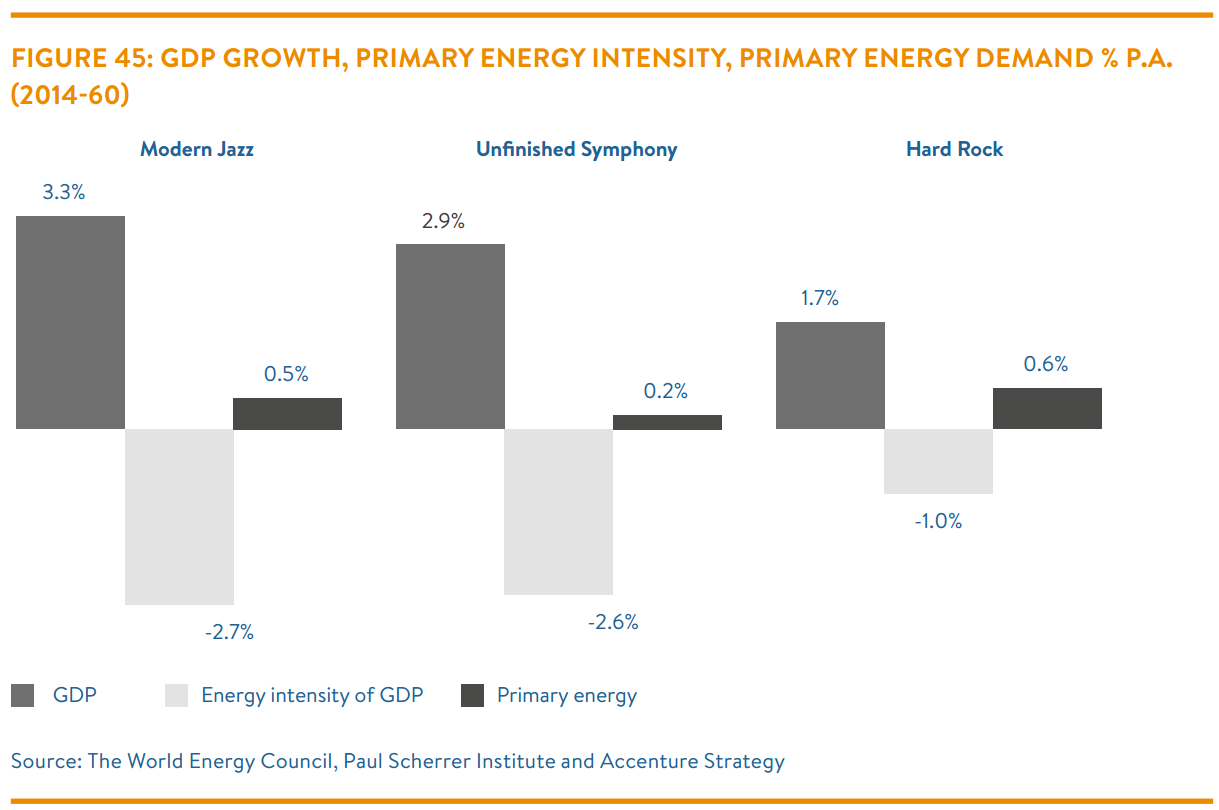

As a result, final energy consumption to 2060 grows 22% in Unfinished Symphony, 38% in Modern Jazz, and 46% in Hard Rock. Primary energy demand to 2060 grows just 10% in Unfinished Symphony, 25% in Modern Jazz, and 34% in Hard Rock. Per capita primary energy demand peaks before 2030 with a maximum annual per capita usage of energy reaching 1.9 TOE.

Energy intensity will decline three times faster in Modern Jazz and Unfinished Symphony. Substantial efficiencies will be gained through the deployment of solar and wind electricity generation capacity. Conversion rates for these renewable energy sources are much higher than those for fossil fuel plants, meaning less energy will be needed from the primary source.

DEMAND FOR ELECTRICITY will double to 2060. Meeting this demand with cleaner energy sources will require substantial infrastructure investments and systems integration to deliver benefits to all consumers.

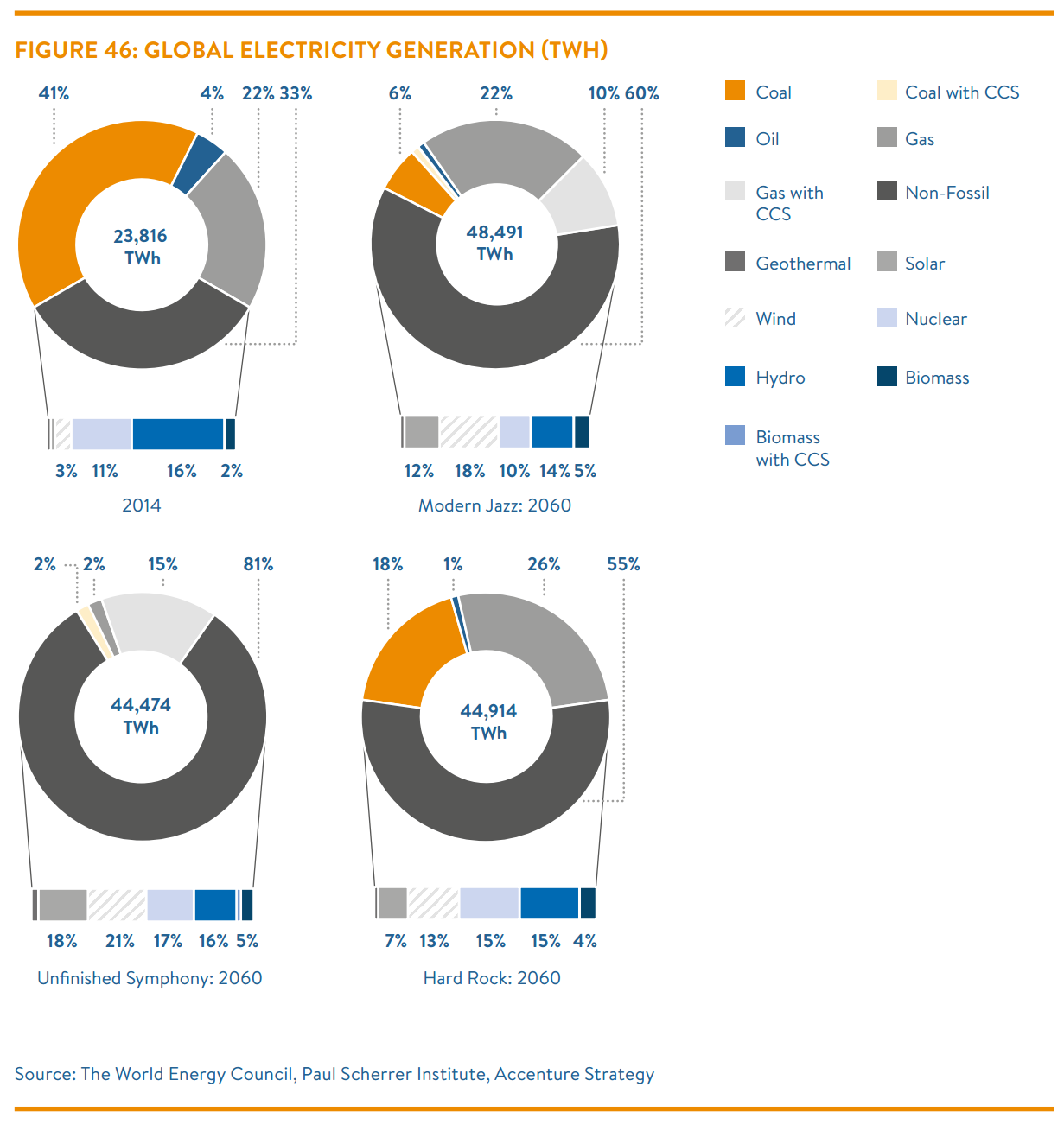

Technology-enabled urban lifestyles demand more electricity. The growth of the middle class, rising incomes, and more electricity-enabled appliances and machines contribute to electricity demand doubling to 2060. Electricity reaches 29% of final energy consumption in Unfinished Symphony, 28% in Modern Jazz, and 25% in Hard Rock. Electricity generation investment to 2060, in these scenarios, ranges from US$ 35-43trillion (based on 2010 market exchange rate).

New cleaner generation is needed to meet climate targets and utility business models are pushed to the limits by stringent policies and shifting consumer demands. The industry must find a way to navigate shifting dynamics. More stringent regulatory requirements for a low-carbon future will force companies everywhere to make significant changes in their business models or face collapse. This change is particularly pronounced for utilities who must respond quickly to changing demand patterns.

Modern Jazz sees the emergence of three models to manage renewable energy penetration and distributed systems: Utility-scale Low Carbon Energy Producers, Distribution Platform Optimizers, and Energy Solution Integrators. Unfinished Symphony sees highly integrated models and funding mechanisms to allocate the system costs of renewables to avoid zero-marginal cost destruction. Hard Rock sees an assortment of models that work well in a unique local context.

THE PHENOMENAL RISE OF SOLAR AND WIND ENERGY will continue at an unprecedented rate and create both new opportunities and challenges for energy systems.

Growth in non-fossil energy sources will dominate electricity generation to 2060, driven by solar and wind capabilities. The steep reductions in the technology learning curve seen in the last decade continue through to 2060 across the three scenarios and are most strongly observed in Modern Jazz and Unfinished Symphony where cost reductions are greater than 70% for the period.

Solar and wind energy account for only 4% of power generation in 2014, but by 2060 it will account for 20% to 39% of power generation. In Unfinished Symphony, strong policy supported by hydro and nuclear capacity additions will allow intermittent renewables to reach 39% of electricity generation by 2060. Large-scale pumped hydro and compressed air storage, battery innovation, and grid integration provide dependable capacity to balance intermittency. Modern Jazz sees intermittent renewables reach 30% of generation enabled by distributed systems, digital technologies, and battery innovation. For both resources (solar and wind), the largest additions will be seen in China, India, Europe, and North America. With less capacity for infrastructure build-out, Hard Rock sees the lowest penetration, with solar and wind generation reaching 20% by 2060.

Other non-fossil fuels, such as hydro and nuclear, will continue to grow. Regionally, there will be greater differences, for example, with hydro being particularly important in Africa and nuclear in East Asia (especially China), and both remaining significant to regional power companies.

DEMAND PEAKS FOR COAL AND OIL have the potential to take the world from “Stranded Assets” to “Stranded Resources”.

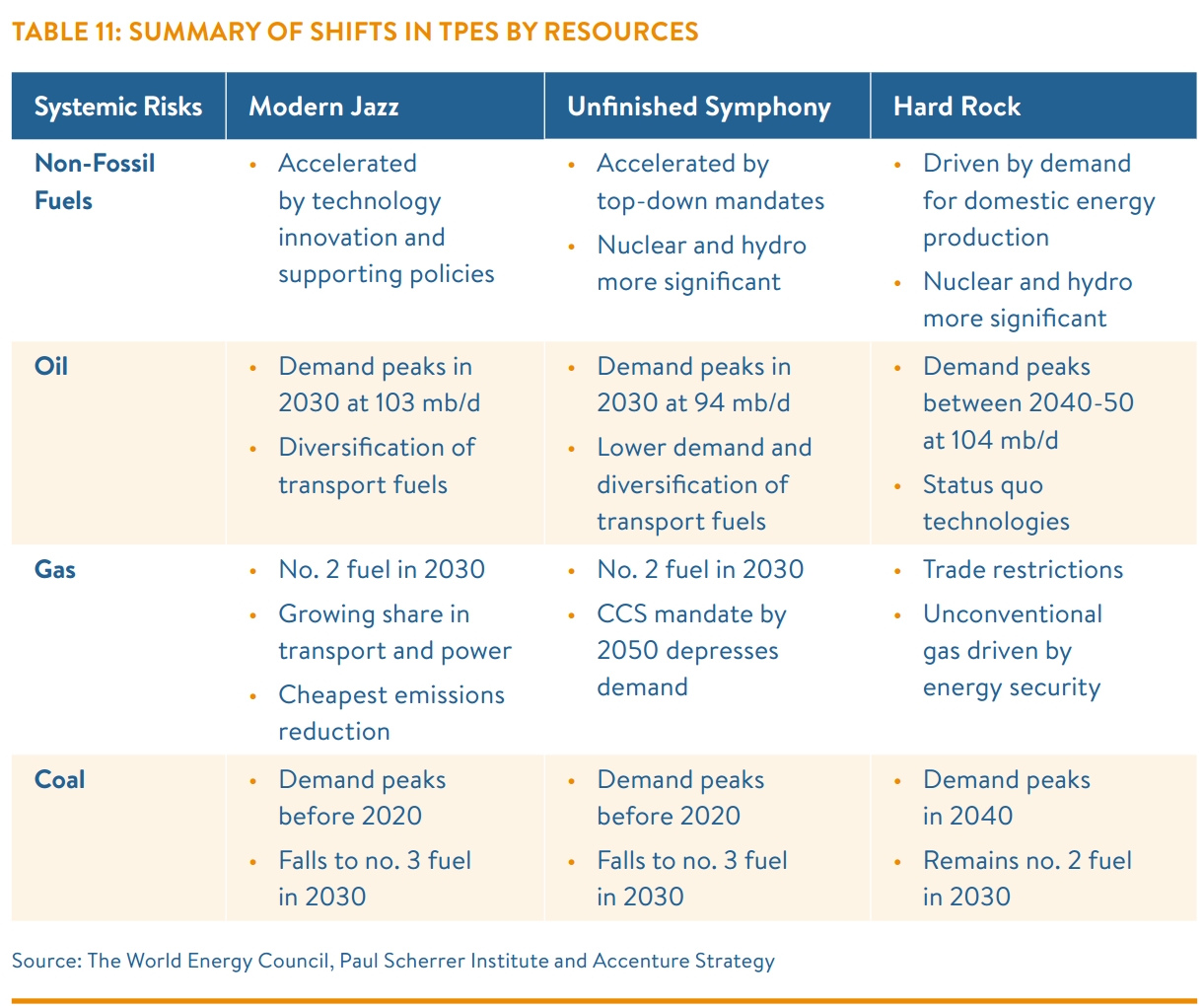

Fossil fuel share of primary energy has shifted just 5% in the last 45 years from 86% in 1970 to 81% in 2014. To 2060, the momentum of new technologies and renewable energy generation results in the diversification of primary energy.

Fossil fuel share of primary energy will fall to 70% by 2060 in Hard Rock, 63% in Modern Jazz, and 50% in Unfinished Symphony.

Coal peaks before 2020 in Modern Jazz and Unfinished Symphony. Unfinished Symphony achieves the most drastic changes with 2060 supplies falling to 724 MTOE. An emphasis on energy security means Hard Rock sees a higher reliance on coal, and peaking in 2040 at 4,044 MTOE. The biggest driver of variance is the degree to which China and India utilise coal to 2060.

Oil peaks in 2030 in Modern Jazz at 103 mb/d and at 94 mb/d in Unfinished Symphony. Despite growing demand for transport fuels, new technologies and competition from alternatives drive diversification and lead demand to slow beyond 2030. Hard Rock sees status quo transport systems dominate. As a result, oil sees a peak and plateau of about 104 mb/d between 2040 and 2050. Unconventional oil reaches 15-16mb/d in Modern Jazz and Hard Rock. MENA remains the dominant oil producer to 2060 in all three scenarios.

The rate of natural gas growth varies broadly across the three scenarios. Modern Jazz sees the rise of LNG and the largest role for natural gas. Technology developments continue in unconventional gas led by North America and later Argentina, China, and Australia. Hard Rock also sees growth driven by unconventionals, but lower gas trade and reduced technology transfer make resources more expensive. Stringent emissions mandates in Unfinished Symphony mean gas grows more slowly.

Demand peaks for coal and oil have the potential to take the world from stranded assets predominantly in the private sector to state-owned stranded resources and could cause significant stress to the current global economic equilibrium with unforeseen consequences on geopolitical agendas. Carefully weighed exit strategies spanning several decades need to come to the top of the political agenda, or 3 4 11 the destruction of vast amounts of public and private shareholder value is unavoidable. Economic diversification and employment strategies for growing populations will be a critical element of navigating the challenges of peak demand.

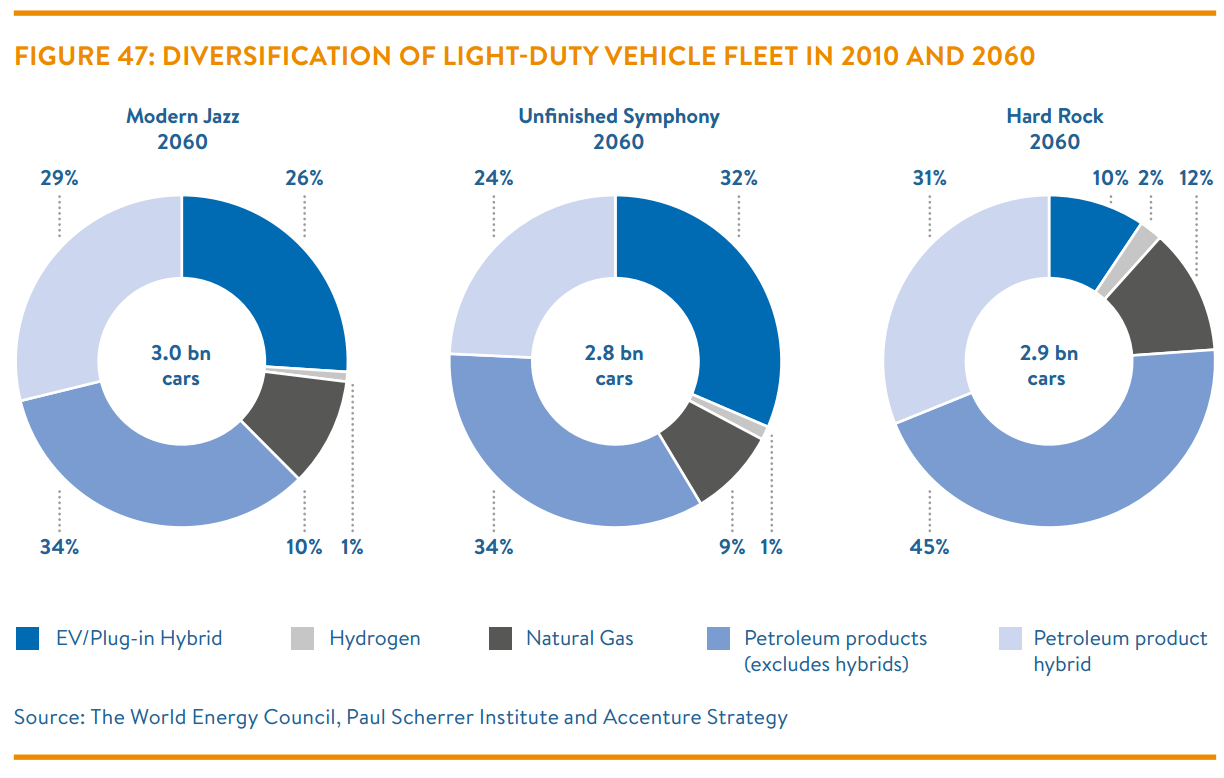

TRANSITIONING GLOBAL TRANSPORT forms one of the hardest obstacles to overcome in an effort to decarbonise future energy systems.

The diversification of transport fuels drives disruptive change that helps to enable substantial reductions in the energy and carbon intensity of transport. Oil share of transport falls from 92% in 2014 to 60% in Unfinished Symphony, 67% in Modern Jazz, and 78% in Hard Rock. Advances in second and later third generation biofuels make substantial headway in all three scenarios, ranging from 10% of total transport fuel in 2060 in Hard Rock, 16% in Modern Jazz, and 21% in Unfinished Symphony.

Disruption is also created by electricity in personal transport systems. A growing global middle class drives the light-duty vehicle fleet to grow 2.5 to 2.7 times to 2060. Modern Jazz and Unfinished Symphony see rapid penetration of electric and hybrid plug-in vehicles globally which reflect 26% to 32% of the light duty vehicle fleet in 2060. Hybrid petroleum vehicles reflect another 24% to 31% share of the fleet.

Progress is made through differing mechanisms. In Modern Jazz, consumer preferences and growing availability of vehicle charging infrastructure through distributed energy systems drive penetration of alternative transport solutions. Conversely, in Unfinished Symphony, government support schemes and integrated city planning result in fewer overall vehicles and penetration of alternative transport solutions, especially in urban areas. Hard Rock sees less infrastructure build-out and therefore less penetration of alternative fuels.

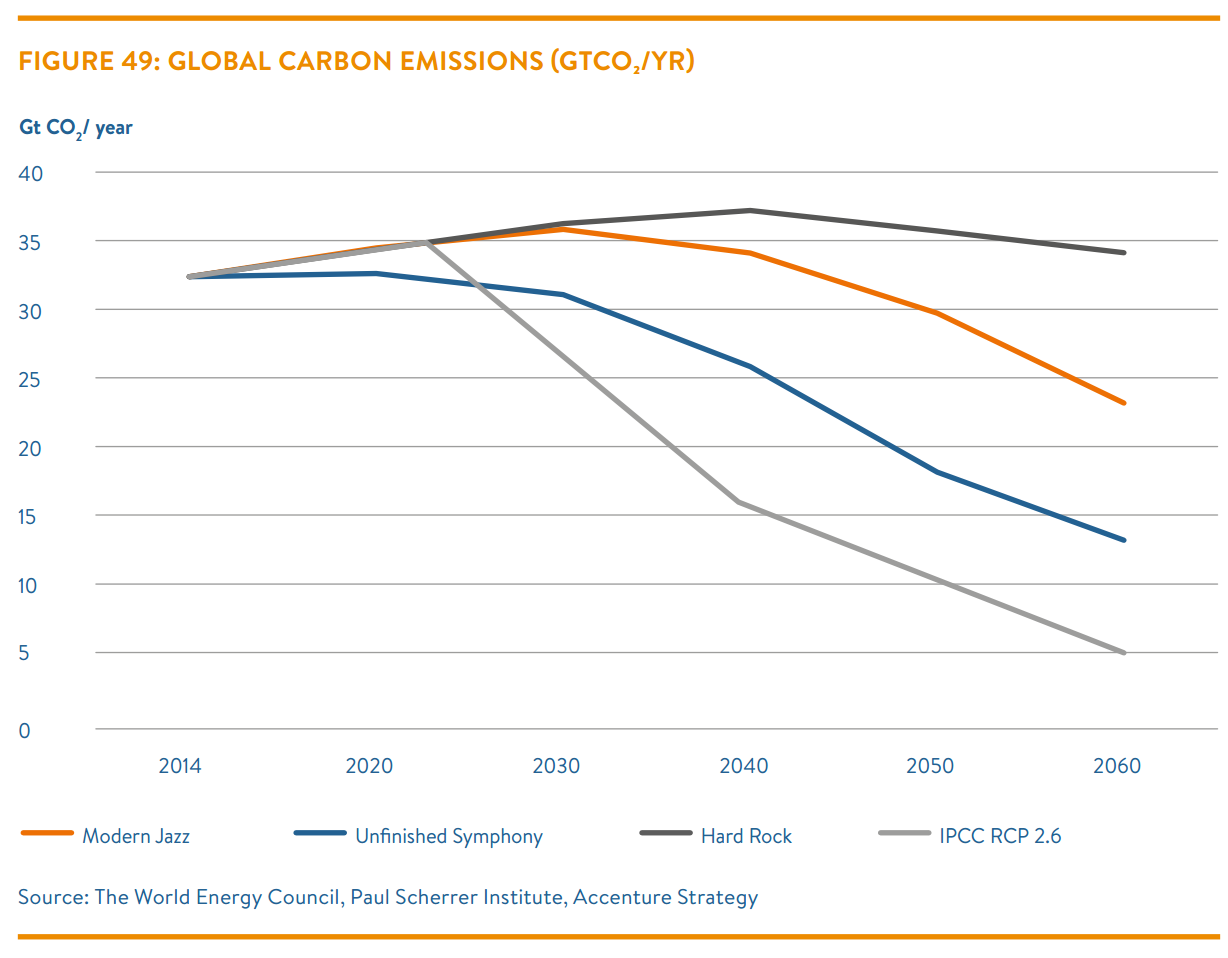

LIMITING GLOBAL WARMING to no more than a 2°C increase will require an exceptional and enduring effort, far beyond already pledged commitments, and with very high carbon prices.

Substantial reduction in carbon intensity drives carbon emissions to peak between 2020 and 2040 across the three scenarios. Still, to reach global climate targets, the world needs an exceptional and enduring effort on top of already pledged commitments, and coordinated global action at unprecedented levels, with meaningful carbon prices. These characteristics are most apparent in Unfinished Symphony where the world comes closest to meeting climate targets. Joint strategic planning efforts, unseen over the last decades, drive global carbon emissions in 2060 to fall 61% below 2014 value.

In Modern Jazz, the deployment of new technologies creates efficiencies and enables continued reductions in the learning curves of solar and wind. Global carbon emissions fall by 28% from 2014 to 2060. A fragmented global economic and political system means Hard Rock sees an overall emissions increase of 5% to 2060, despite lower upward pressure from economic growth. Without global commitment, reductions in carbon and energy intensity for Hard Rock are less than half of what is seen in the other two scenarios.

In all three scenarios, the carbon budget is likely to be broken in the next 30 to 40 years. Modern Jazz and Hard Rock exceed the 1,000 GtCO₂ carbon budget in the early 2040s and Unfinished Symphony exceeds the budget before 2060.

GLOBAL COOPERATION, SUSTAINABLE ECONOMIC GROWTH, AND TECHNOLOGY INNOVATION are needed to balance the Energy Trilemma.

Each scenario emphasises one of the three dimensions of what World Energy Council calls the Energy Trilemma. This definition applies to the energy sustainability of three core dimensions: Energy Security, Energy Equity, and Environmental Sustainability. Modern Jazz and Unfinished Symphony both provide models for sustainable economic growth and technology innovation. Modern Jazz achieves the highest energy equity. Unfinished Symphony demonstrates the importance of global cooperation in achieving environmental sustainability. Hard Rock demonstrates how, when economic growth comes under pressure and social tensions increase, governments tend to lower consideration of global impacts and focus on domestic energy security.

RECOMMENDATIONS The world is on the cusp of change. The energy industry is facing decades of transformation. The challenge to the world’s industry leaders is to maintain the current integrity of energy systems worldwide while steering towards this new transformed future. This requires new policies, strategies and the consideration of novel and risky investments. Each scenario provides insight into high impact areas of consideration for industry leaders and highlights areas for action:

• Reassess capital allocations and strategies

• Target geographies and new growth markets in Asia, MENA and Sub-Saharan Africa

• Implement new business models that expand the energy value chain and exploit the disruption

• Develop decarbonisation policies

• Address socioeconomic implications of climate change policies

Leaders are faced with important decisions in the context of high political, financial, technological and social uncertainty about the future of energy. The decisions taken in the next 5 to 10 years, in response to these and other implications, will have profound effects on the development of the energy sector in the coming decades.

The differing outcomes across the three scenarios provide leaders with short-term signals. These signals are invaluable to the robust development of medium and long-term enterprise strategies, government policies, investment and divestment decisions. For example, leaders may want to explore what assets in their portfolio may become stranded assets by 2030 or 2040 in Modern Jazz, Unfinished Symphony or examine Hard Rock realities.

These scenarios can also be applied to assess the consequences of climate change policies and to consider the robustness of portfolios for large-scale infrastructure investments, such as power plants for the period to 2060. In exploring these and other complex decisions, the Modern Jazz, Unfinished Symphony, and Hard Rock Scenarios provide energy leaders with an open, transparent, and inclusive framework to think about a very uncertain future.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.