Lot’s of excitement in the MSM yesterday about a returning Australian trade surplus, triggered by UBS:

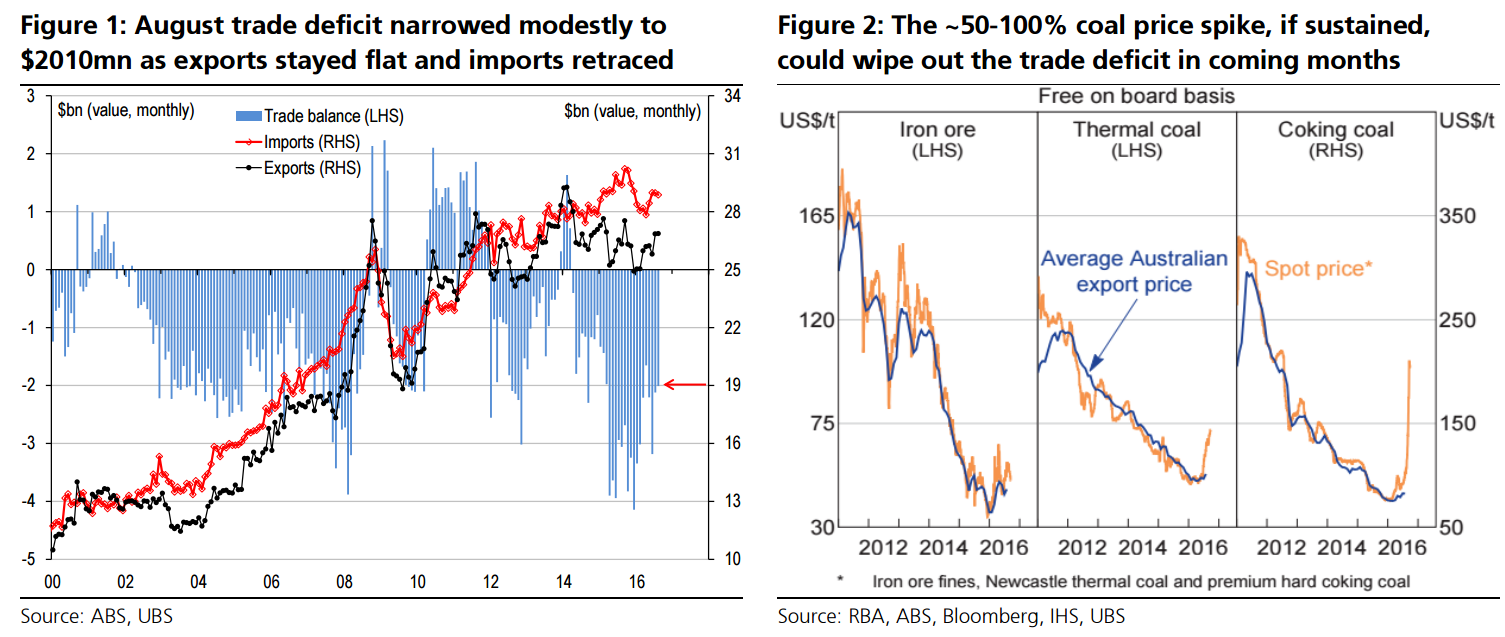

August trade deficit continues narrowing trend to $2.0bn, after revised $2.1bn The trade deficit was smaller than expected in August at $2.0bn (UBS: $2.25bn, mkt: $2.3bn), the smallest deficit since Apr-16, narrowing slightly from a revised $2.1bn in July (was $2.4bn) – continuing the improving trend from a record ~$3bn average in the last year or so. In August, export values were flat m/m (after +4.1%). The y/y picked up to 2.1% y/y – driven by booming services (+13.7%, fastest since 2007), while resources edged up (+0.7%), partly offset by falls in manufacturing (-2.1%, worst since 2013) and rural (-7.0%). Elsewhere, on the imports side, values eased m/m (-0.4%, after 0.0%), keeping the y/y falling moderately (-1.7%).

Implications: net exports ~flat for Q3 GDP; deficit could disappear on coal Overall, the trade deficit continued its improving trend of recent months. Indeed, the massive spike in coal prices recently means export values will likely surge across September and October, which will narrow the trade deficit sharply further – albeit the extent is hard to quantify given the unclear relationship between spot, contract, and ‘received’ export prices (see Figure 2). Nonetheless, with coal exports around ~$2.8bn per month – equivalent to a ~10% share of total exports – the price spike, if sustained over coming months, could potentially be large enough to wipe out the overall trade deficit by itself (ceteris paribus). Meanwhile, for Q3 real GDP, our preliminary estimates imply that net exports volumes are on track to make a broadly neutral impact on growth, albeit today’s revisions and large export price moves add considerable uncertainty.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.