Arthur Ilias, the head of the Urban Development Institute in Australia (UDIA), is the latest so-called expert to blame Millennials’ supposed spendthrift habits for not being able to afford a home. From The Daily Mail:

Mr Ilias says people born between the mid-1980s and 2000 prioritise ‘gadgets’ and luxury over entering the housing market…

‘Our kids today are happy to stay at home for as long as they can, have a great time enjoying their Master Chef lifestyle with all of their devices and gadgets’…

‘And then eventually rent somewhere when Mum and Dad say “enough is enough”…

If Ilias had actually examined the data, he would have seen that today’s millennials are actually more frugal than their baby boomer parents.

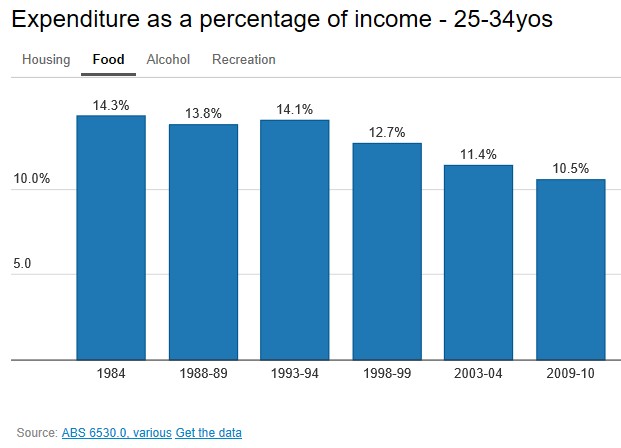

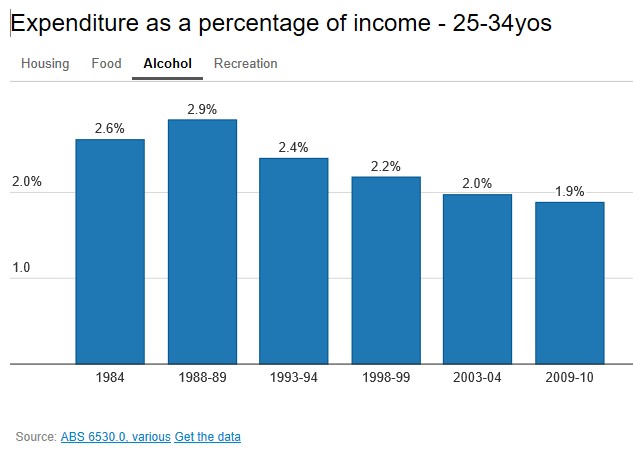

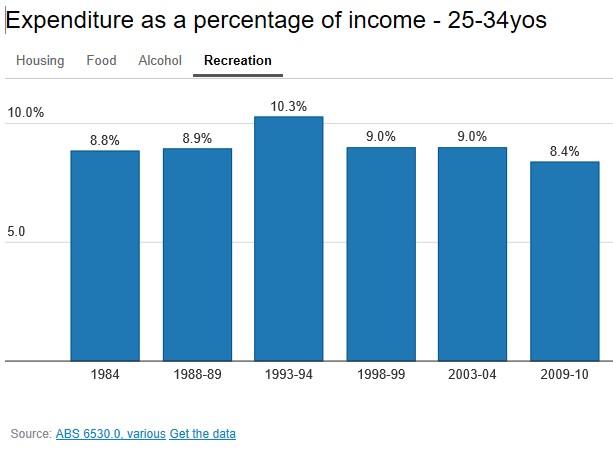

The ABS publishes survey data on household expenditure and its shows clearly that in 2010 (latest available), 25-34 year olds spent less on food, alcohol, and recreation (let alone cigarettes) than they did in 1984:

Advertisement

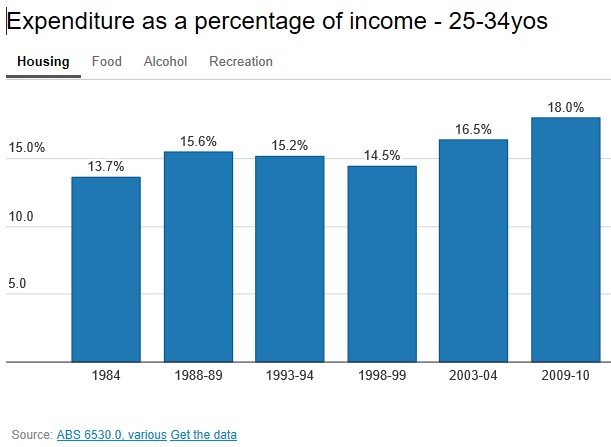

By contrast, they spent way more on housing than their baby boomer counterparts:

Advertisement

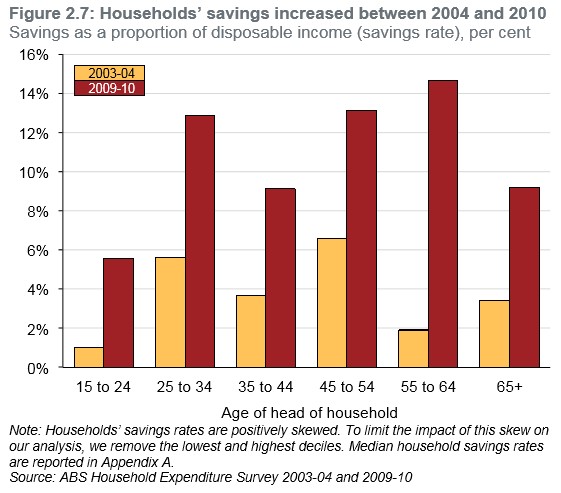

Research from the Grattan Institute has also found that younger Australians have been containing their spending and boosting their savings:

Savings are particularly important for young households that have few existing assets. Overall household savings increased markedly over the decade. The savings rate increased from just 0.4 per cent of after-tax income in 2003 to 10 per cent in 2013. All age groups saved more of their income, but households aged 55-64 increased their savings most (Figure 2.7).

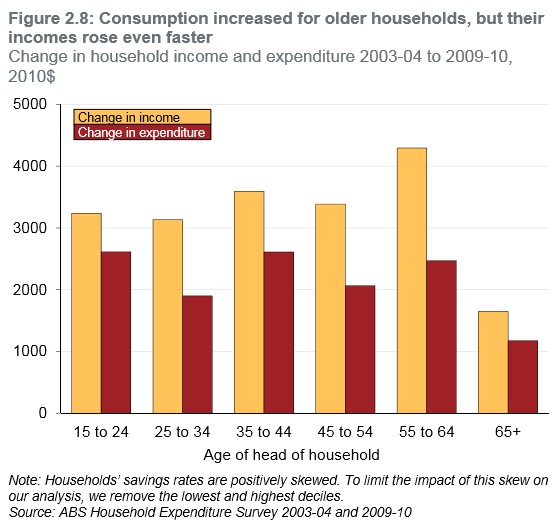

Even though their spending increased more than any other age group, their incomes grew even faster (Figure 2.8). Young households also saved more (Figure 2.7). They did so by containing spending as their disposable incomes increased (Figure 2.8).

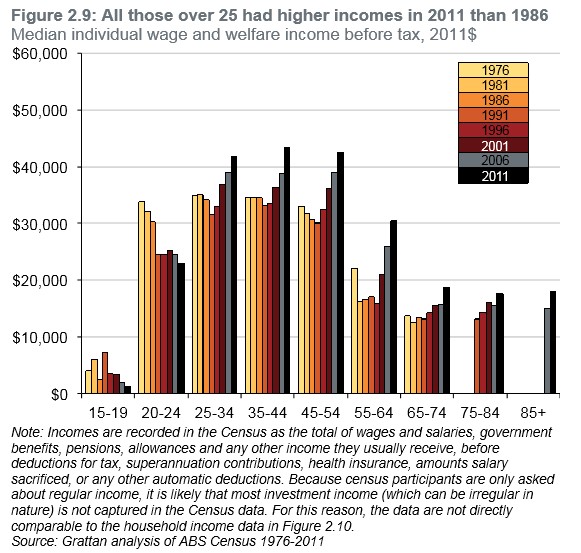

Grattan also showed that under-35s enjoyed less real income growth than older cohorts over the 35 years to 2011:

Advertisement

In short, Ilias is full of it. The data does not support his assertion that Millennials are enjoying a “Master Chef lifestyle”.

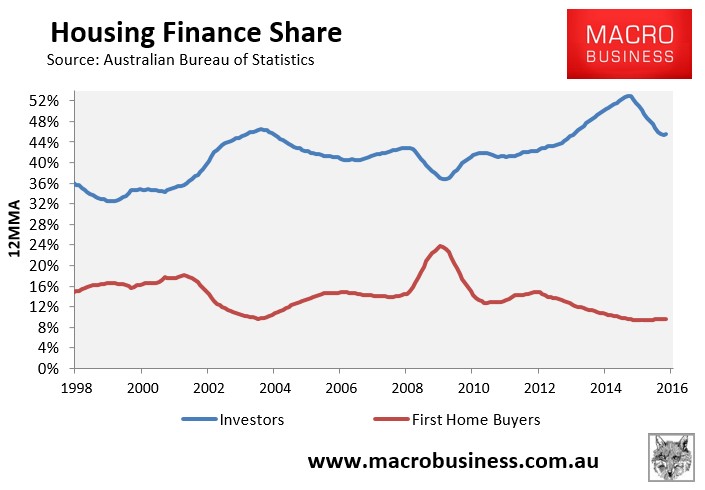

Instead of bashing Australia’s youth, Ilias should drop the UDIA’s staunch opposition to negative gearing and capital gains tax reform, given the data clearly shows that investors have crowded-out first home buyers:

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.