Fairfax’s Peter Martin has written a ripper article arguing that low interest rates have ’tilted’ the mortgage burden so much that many recent buyers may never repay their mortgages:

On Tuesday, in his first speech as governor, Lowe explained that headline inflation had fallen to just 1 per cent – the lowest, with two brief exceptions, since the recession at the start of the 1960s…

It’s fallen because producers and workers worldwide lack pricing power…

You might be thinking that low wage rises aren’t a problem so long as prices are increasing by less. But that ignores a little-recognised phenomena known as “mortgage tilt”.

When you take out a mortgage in a world of high inflation, your payments are “front-end loaded”…

In a world of low inflation the “tilt” becomes much less severe. If repayments consume a large proportion of your wage at the start, they’ll keep doing it for decades…

To the extent that “tilt” is one of the reasons, deeper cuts in interest rates won’t much help.

We’ve a problem, one born of success. Low inflation looks good, until you’re in it.

I have been making this same argument for years and are relieved that somebody else ‘gets it’: low interest rates are not a ‘gift’ to the younger generations. Not only do they make it harder to raise a deposit for a home (via lower returns on savings), but they also mean that a mega-mortgage today will remain a very big mortgage in a decade’s time thanks to anaemic inflation and wages growth.

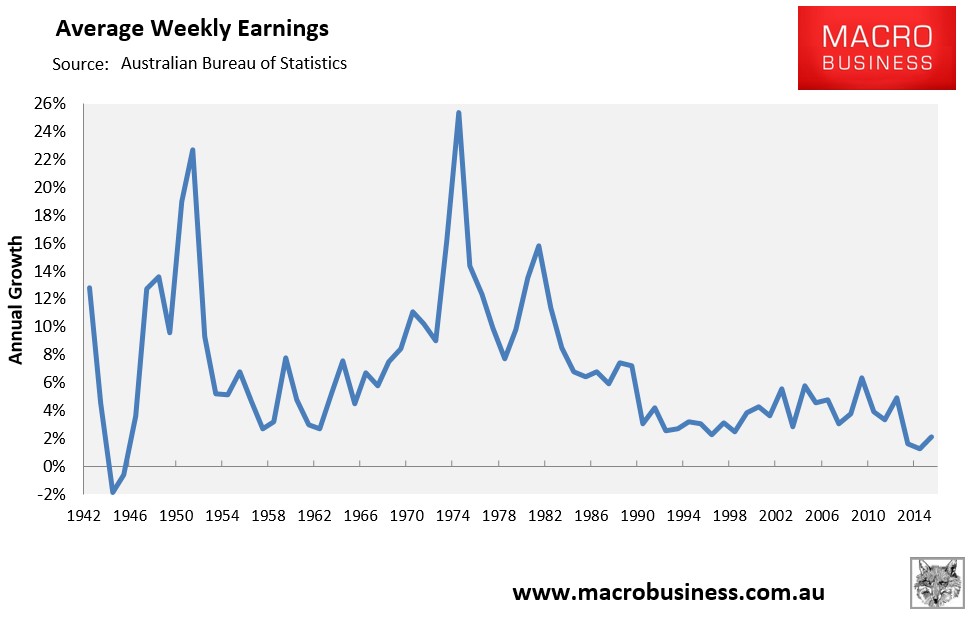

One only has to look at the below chart showing that average earnings growth is hovering near its lowest level in recorded history:

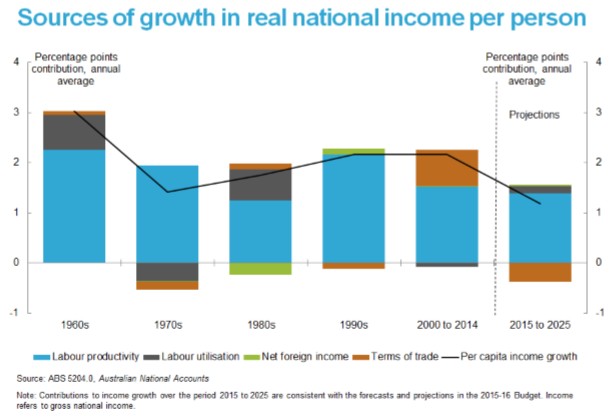

And the next chart from the Australian Treasury showing that real average income growth is expected to be the weakest in at least 60 years over the coming decade (see next chart).

Again, today’s first time buyers will be paying-off their mega mortgage debts for decades, thanks to anaemic inflation and wages growth that will not erode their debts, as it did for many of the baby boomer generation. Thus, their pain will be both deep and prolonged.

Rather than being a ‘benefit’ to today’s home buyers, the low inflation/interest rate environment that exists today is a curse that will act as a millstone around their mortgaged necks for decades to come.

unconventionaleconomist@hotmail.com