By Chris Becker

So the US CPI comes in on target, but because internals were off by 0.1%, everyone thinks the Fed will be a bit slower with their rate rise agenda, so stocks and risk were bid across the board. That’s markets for you – although better earnings in the US were also part of the narrative, particularly bank stocks while in Europe markets lifted in anticipation of another accomodative central bank meeting tomorrow night – this time the ECB. Oil lifted on speculation of production cuts and innuendo surrounding increased gasoline inventories in the US – both unconfirmed, but that’s oil for you! USD has retreated due to all of the above, as many scramble to cover short positions in the majors.

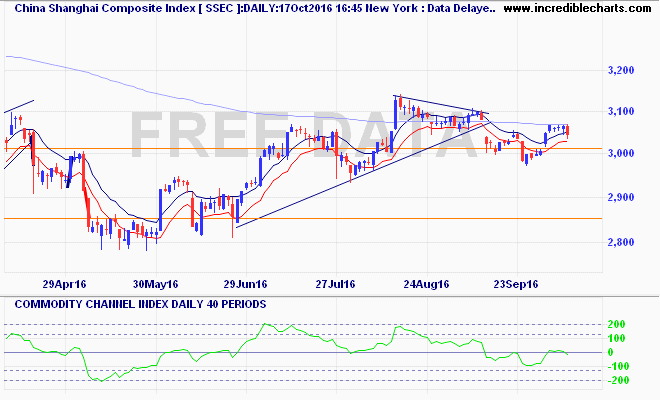

Looking at Asian stocks first yesterday, where the Shanghai Composite shot out of the gate lifting 1.4% to 3083 points almost above the closely watched 200 day moving average. Today’s slew of releases including GDP is likely to determine where we go from here with my target the former high at 3140: