by Chris Becker

Its not looking like a fun week, with Asian stocks following the US lead overnight with falls across the board. The volatility went the other way in currency markets as both Aussie and more so Pound Sterling bounced back, the latter uncharacteristically in the Asian session leading into the London open as commodities were relatively unchanged. Tonight’s Fed Minutes will be the focus as currency traders continue to hedge – now almost 70% in favour of an interest rate rise in December.

The Shanghai Composite has fallen slightly, down 0.3% at 3055 but still above terminal support at the 3000 level as the Yuan fix heads even lower. The Hang Seng is off more, down a little over 1% and teetering on its own support level at the 23000 point level.

In Japan, the moves were similar, with the Nikkei falling almost 1% as expected, now below 17,000 points, swapping the previous session gains as Yen strengthens slightly.

For the ASX200, the local market gapped down more than 1% in line with futures, but rallied throughout most of the session to only close down 0.1% yet still below 5500 points. This is a market still beholden to outside factors, so watch out!

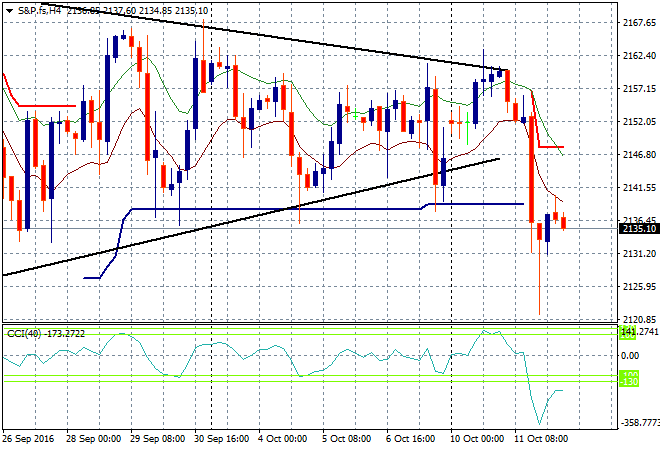

Tonight, the S&P500 bears watching with futures indicating more falls at the open as the market remains below last week’s long held support at 2130 points:

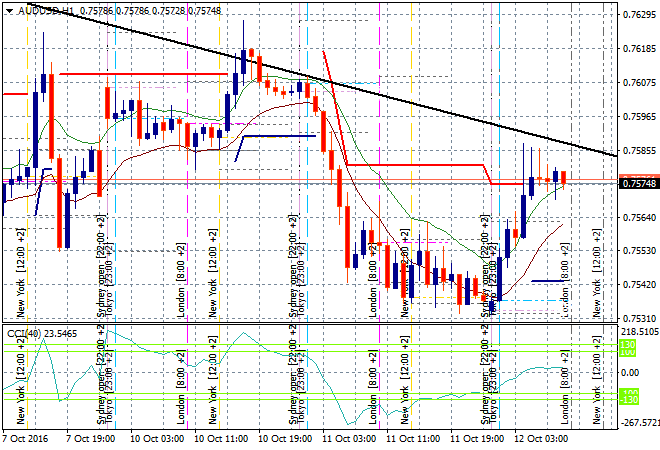

The Aussie dollar with congestion on the hourly chart and oversold momentum pointing to an upswing from the 75.30 to the 75.70 level today. This has run out of puff going into the London session as the daily downtrend line becomes resistance overhead. Only a poor reading of the Fed minutes is likely to see this bound over that line:

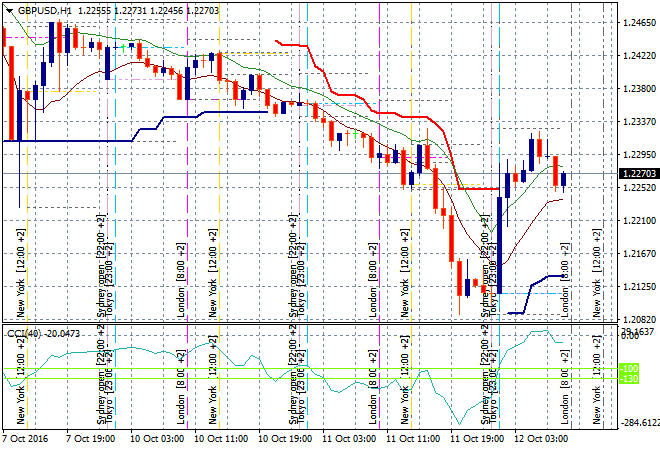

Similarly, the extremely oversold Pound had a fightback today, up over 150 pips and settling at 1.2270 where it could fly higher again tonight as The City takes stock:

The data calendar tonight includes a few speeches from BOE and Federal Reserve deputy governors, while industrial production numbers for Europe and the Fed minutes from last month’s meeting will be watched closely.