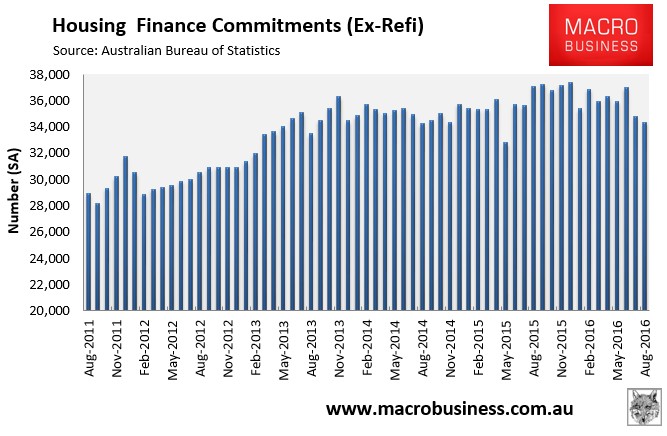

Today’s housing finance data for August, released by the Australian Bureau of Statistics (ABS), posted another seasonally adjusted fall in overall housing finance commitments, with the trend in mortgage growth also continuing to weaken.

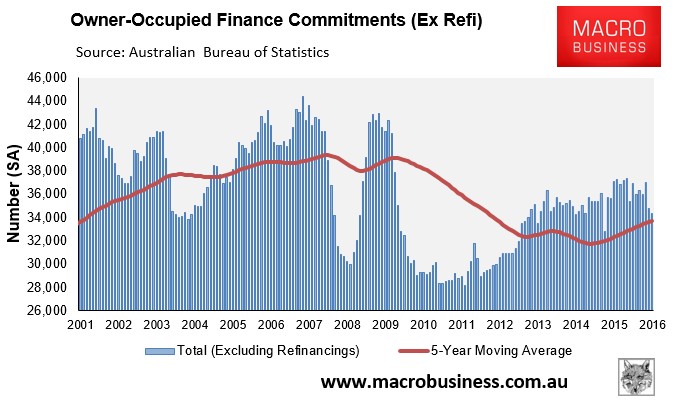

According to the ABS, the total number of owner-occupier finance commitments (excluding refinancings) fell by a seasonally adjusted 1.3% over the month and was 7.4% lower over the year:

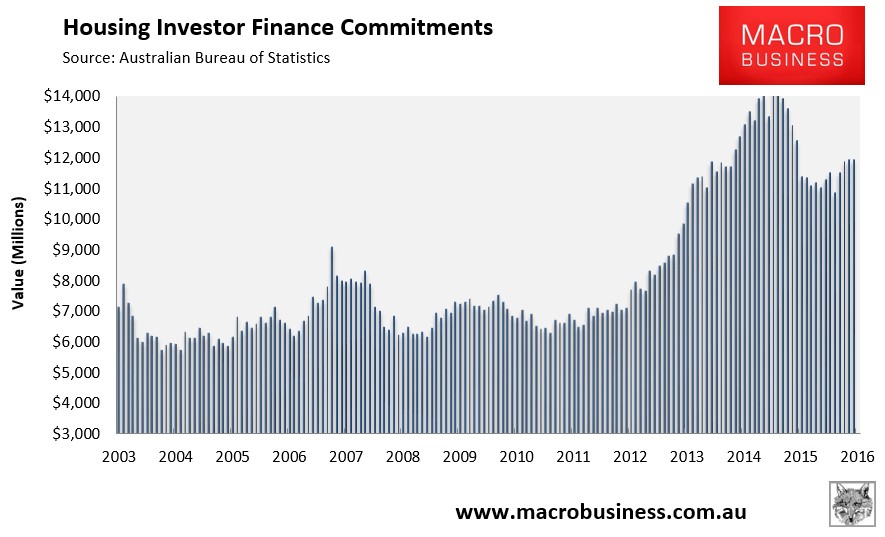

In comparison, the value of investor finance commitments was basically flat (+0.1%) in August but was down by 5.0% over the year (see next chart).

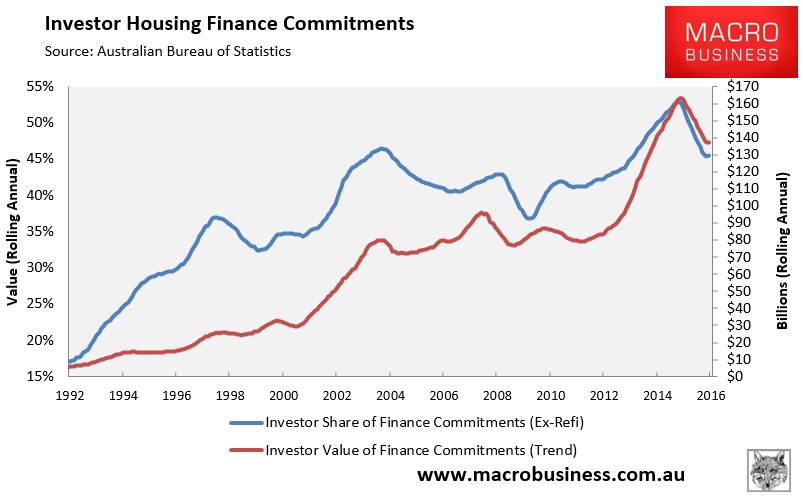

The annual share of total loans going to investors (excluding refinancings) rose marginally (+0.1%) to 45.5% in August, but was still down significantly from the peak of 52.9% recorded in July 2015:

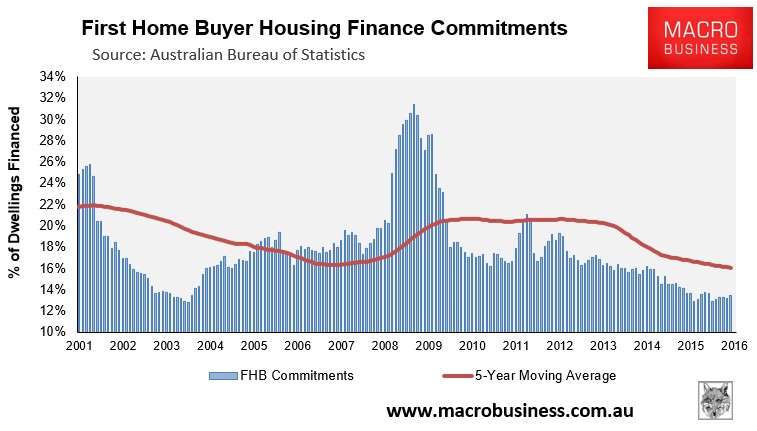

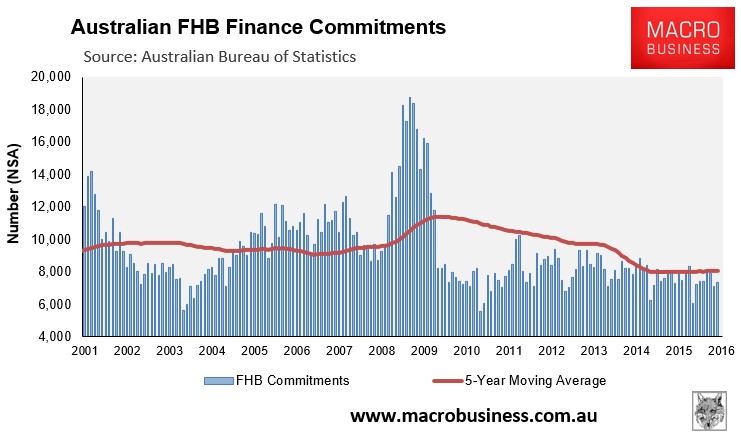

First home buyer (FHB) owner-occupied demand rebounded in August. It rose by 3.5% over the month to be up by 1.2% year-on-year, but represented an appallingly low 13.4% share of total owner-occupied finance commitments, which are stuck in a protracted funk (see below charts).

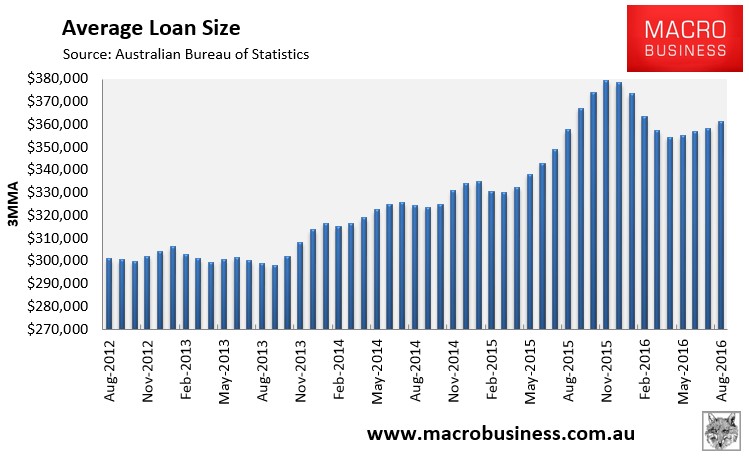

Meanwhile, the average loan size rose marginally in August, up 0.7% over the month, but was still down by 1.0% over the year. The trend is also soft given the sharp falls at the start of the year:

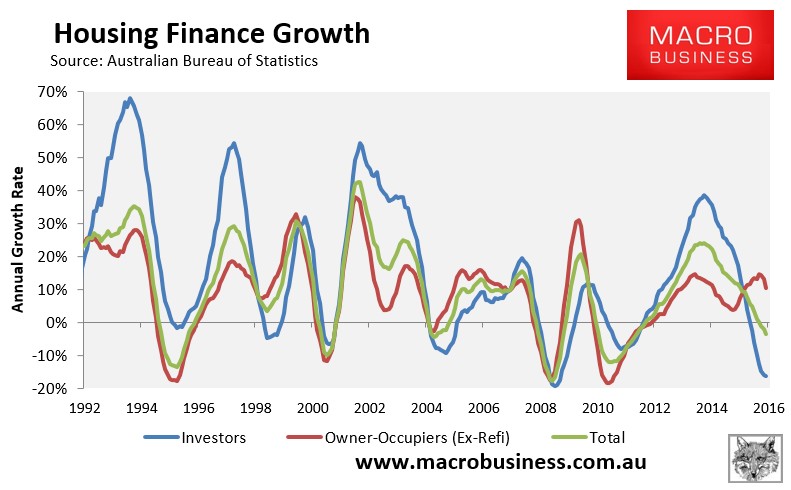

Finally, the below chart shows that growth in both owner-occupied housing demand and investor demand are now falling, thus dragging the overall growth of housing finance (excluding refinancings) sharply into negative territory:

Normally, when trend housing finance growth has fallen to this extent, it has been associated with a significant weakening of house price growth nationally. The fact that it is reportedly not happening this time around, at least according to the CoreLogic index, is very odd and most likely explained by a corresponding collapse in volumes; huge sums of foreign money; or numberwang in the CoreLogic index.