A key purpose behind the ECB’s alternative easing programs has been to materially improve credit provision and conditions in the Euro Area economy. Exhibiting a lagged relationship with the business cycle and further hampered by the health of European banks, success on this front has been slow and limited.

As referenced in their most recent policy statement, “loan dynamics followed the path of gradual recovery observed since the beginning of 2014”. However, that has only left annual growth in loans to non-financial corporates and households at 1.9%yr and 1.8%yr respectively at September 2016.

These are hardly strong outcomes and, of late, there has been a clear lack of momentum, meaning further material gains are unlikely for the forseeable future. Indeed, from the detail of the ECB’s own bank lending survey, there is evidence to suggest credit growth is set to slow.

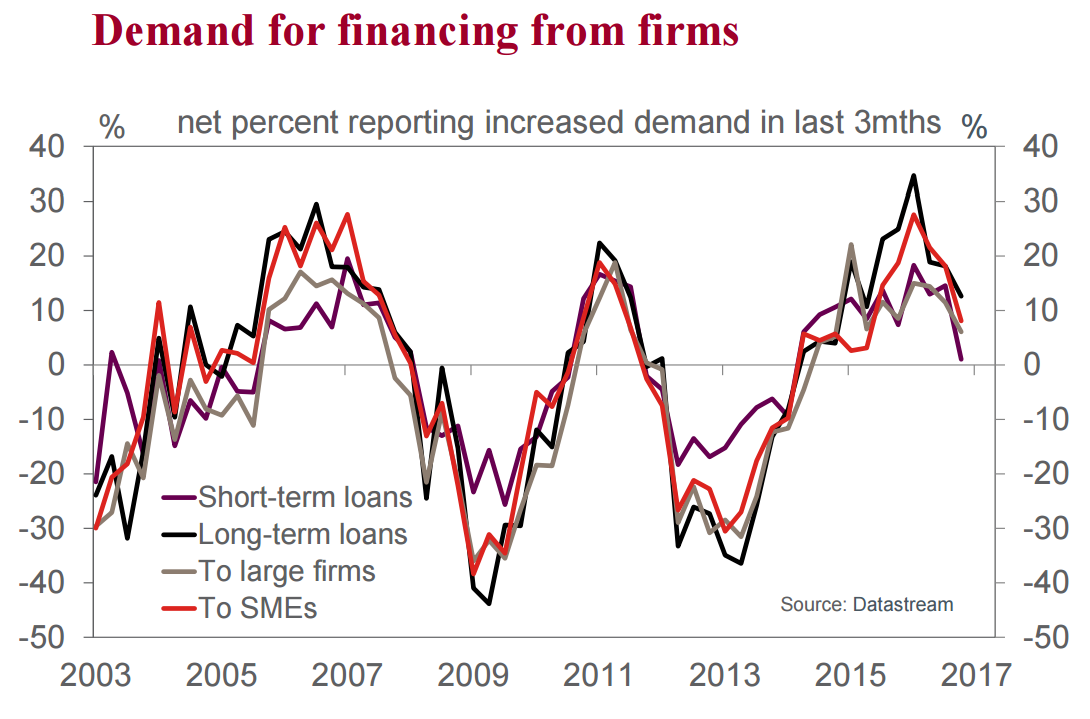

Starting with non-financial corporates, the ECB survey reports that there is a clear downtrend in current credit demand, with the net per cent of respondents reporting increased demand for credit from firms having peaked in the first quarter of 2016 and consistently declined ever since.

Expectations of future growth in non-financial corporate loan demand is also in a clear downtrend. Importantly, the peak in the expected series came in mid-2015 (six months ahead of the actual series’ peak) and has endured. It should be noted though that the expected series peaked at a high level and is still consistent with positive credit growth – so we are not anticipating an outright contraction in new lending.

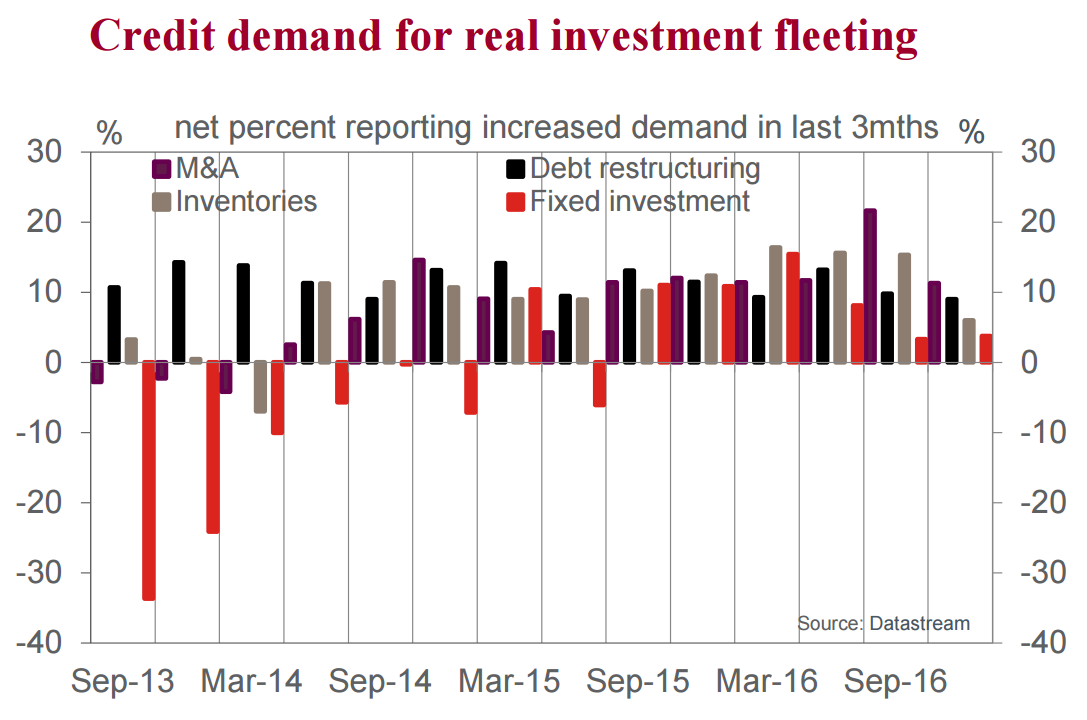

The purpose for new loans for corporates also remains unhelpful to the growth outlook for the real economy. Having improved from mid-2015 to early 2016, the six months to October saw demand for credit to fund fixed asset investment abate.

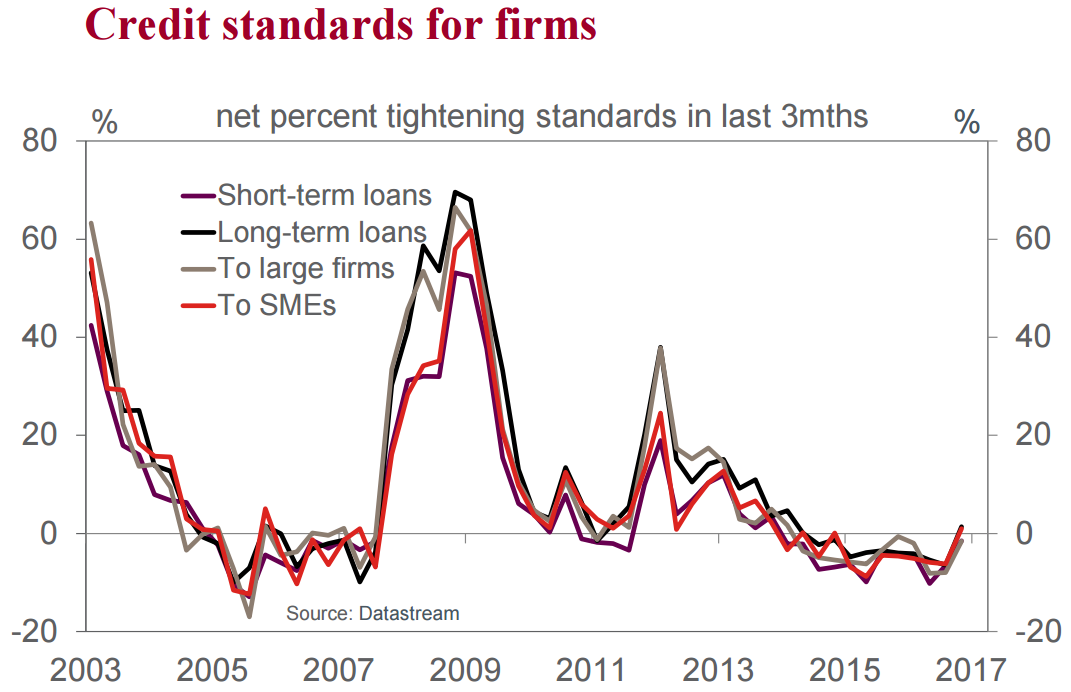

Ergo, after a prolonged contraction to mid-2015, it seems a recovery in real investment has failed to launch. This is partly attributable to a lack of confidence in the outlook. But it has also come as a result of loan conditions for firms remaining tight. The ECB’s survey suggests conditions have only improved incrementally since mid-2014.

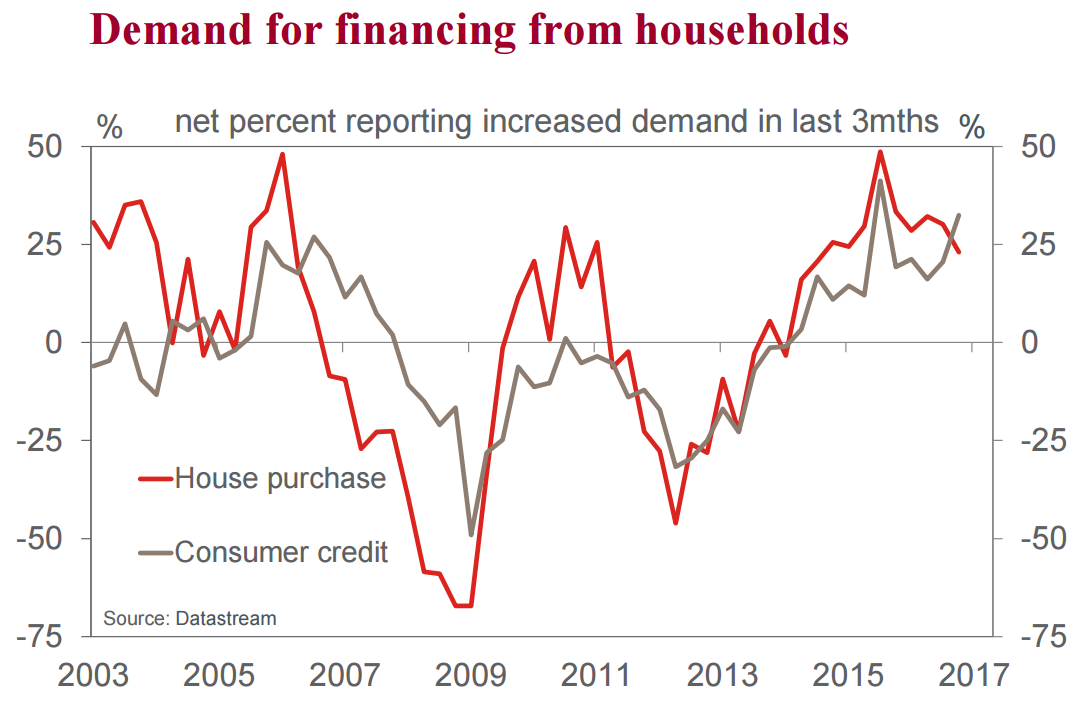

The above results imply only limited support to job creation and therefore to household incomes. It is unsurprising then that growth in credit to households also looks to be peaking at a fairly modest pace relative to history.

As for non-financial corporates, households in the Euro Area are clearly benefitting from lower interest rates. Yet the overall credit conditions they are currently experiencing are little changed from a year ago, or indeed late-2013. Note that since end-2013, the average percentage of banks reporting an easing in standards for mortgages and consumer credit has been 2% and 3% respectively. In the three years prior, an average of 14% and 6% of respondents reported tighter conditions each quarter.

The above analysis does not, of itself, justify the ECB continuing its asset purchases well beyond March 2017 – there are many market and political points that also need to be considered. But it does suggest that credit provision in the Euro Area is not yet self sustaining. Without the ECB’s support, the Euro Area’s economy; banks; and financial markets will be left in a fragile state, susceptible to any and all economic or financial shocks.

Add the political strife building across the Continent that is threatening further eurozone fracturing with the Italian referendum in December, Netherlands election in March, French election April-May, German election in September then Italy six months later and there is no way that the ECB can allow economic weakness and/or peripheral funding stress to creep back in.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.