Leith has covered this but I’ll give a word to UBS who have been ahead of curve:

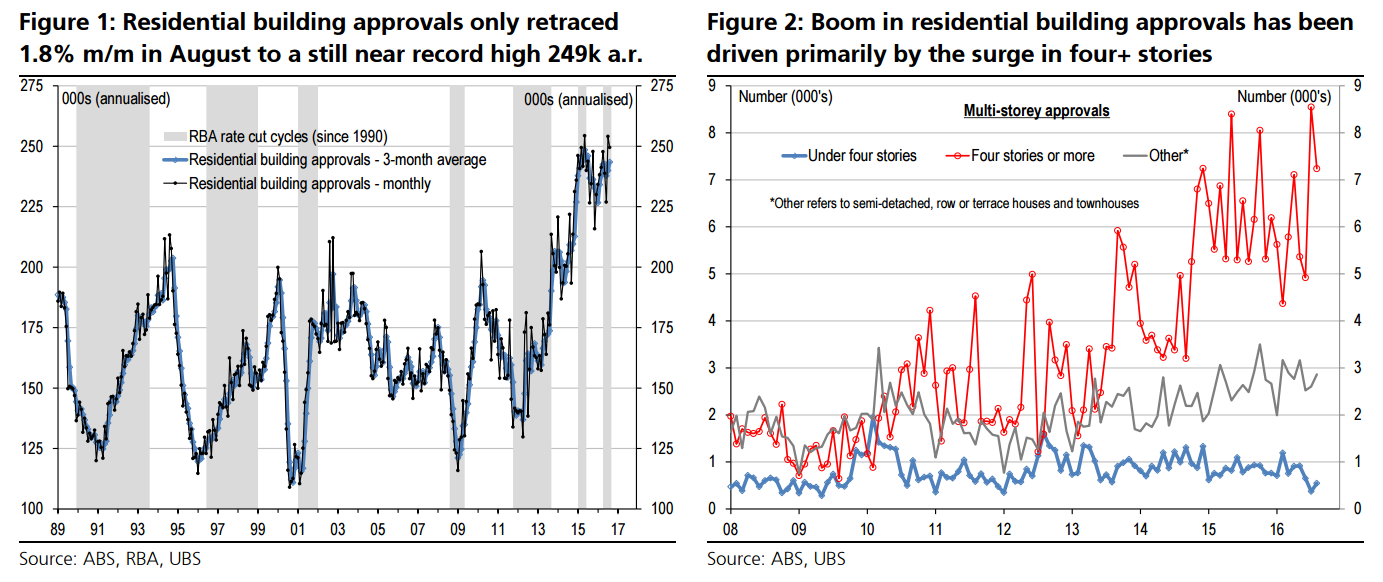

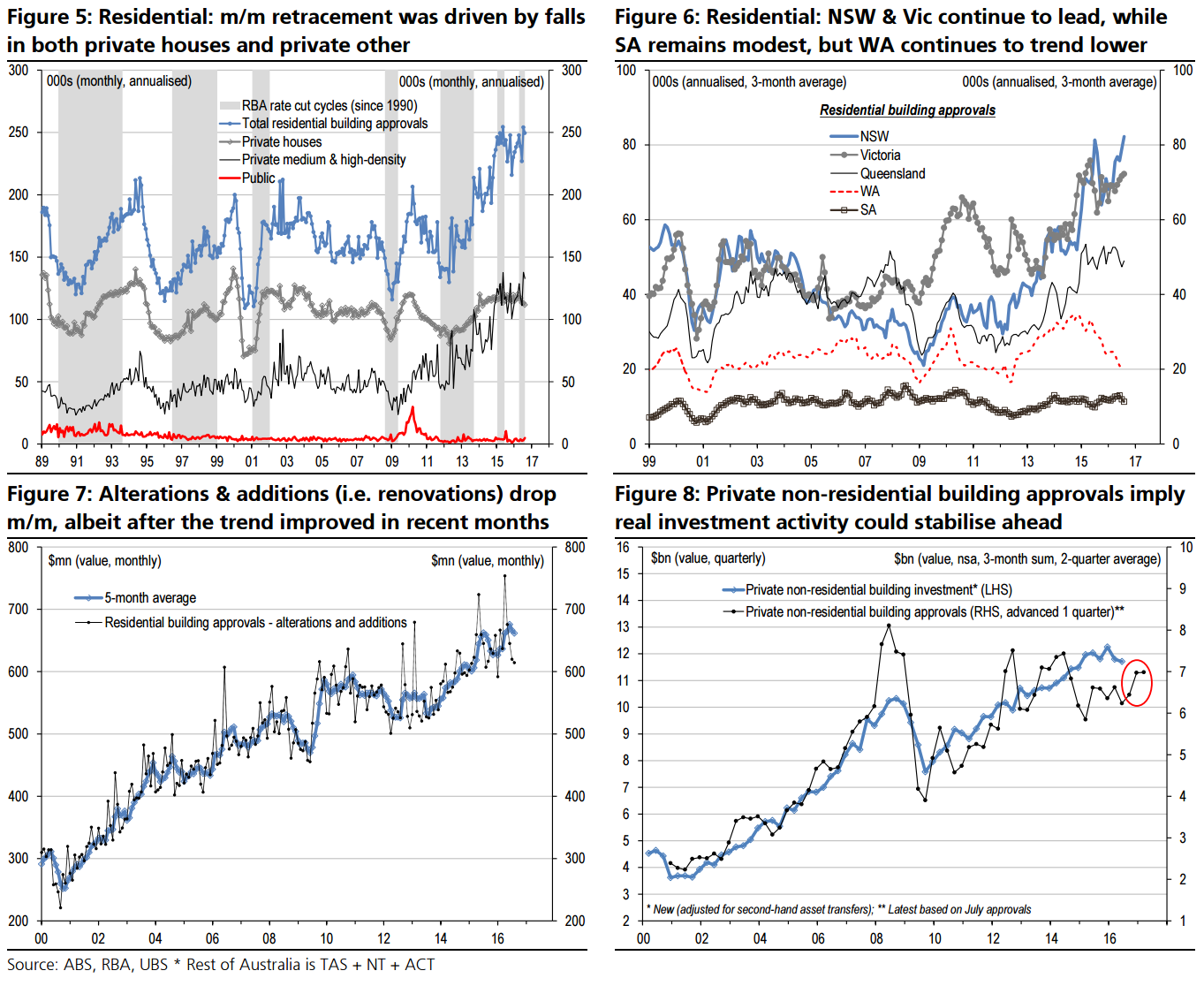

August residential approvals again surprise higher at near-record 249k a.r. Residential building approvals were again stronger than expected in August, falling back by only 1.8% m/m (UBS & mkt: -6.0%, +10.1% y/y), to a 249k a.r.; and followed an upwardly revised 12.0% spike in July to an equal record 254k a.r. (was 252k) – seeing the last 2 months average the highest on record. In August, the m/m fall was led by private multi’s (-4% m/m, but +26% y/y), which was driven by high-rises of 4+ storeys (see Figure 2). Private houses eased again (-1.3%, -6.5% y/y). The tiny public sector spiked again (+61%, +148% y/y). For total approvals by State, NSW & Victoria continue to lead, QLD is broadly sideways, while WA continues to trend lower. Meanwhile, the value of alterations & additions (i.e. renovations) retraced further (-1% m/m, +1% y/y), after previously showing some renewed momentum. Elsewhere, the value of non-residential building approvals slumped back again (-24% m/m, after -6%, -13% y/y) – albeit dragged by volatile public (-57% m/m) – with the trend of private approvals still implying a steadier trend for private non-residential investment ahead.

Overall, housing once again continues to defy even our relatively positive view, pointing to upside risks to our forecasts for prices and commencements, and shows that housing is stronger than the RBA thinks. As detailed by a suite of models in our deep-dive – the UBS ‘housing supply tracker’ – the backlog of approvals/commencements implies dwelling completions (i.e. housing supply) will not actually peak until ~2018. Today’s data reinforces that strong conclusion. Hence, dwelling investment seems likely to continue to rise in 2017, and provides a key support to our recently upgraded GDP forecast for above consensus growth of 3% y/y in 2017, as well as supporting our view that the RBA is set to hold the cash rate unchanged ahead.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.