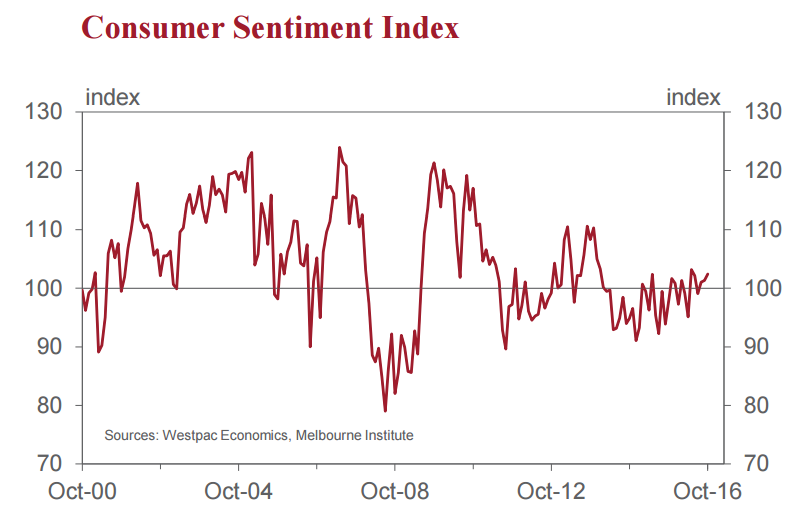

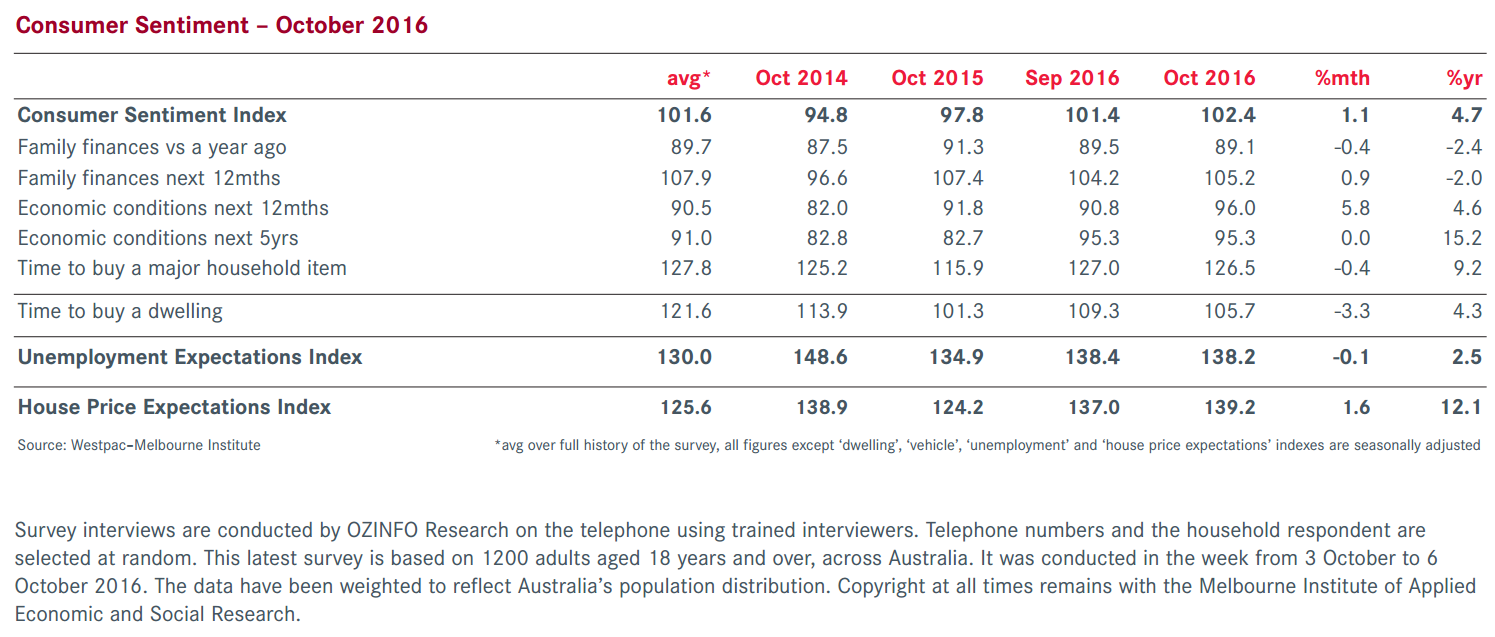

• The Westpac Melbourne Institute Index of Consumer Sentiment rose by 1.1% in October from 101.4 in September to 102.4 in October.

This result extends a remarkable run of stability in the Index. Over the last six months the Index has held within a relatively tight 4% range with five of the six readings hovering just above 100 indicating that optimists have remained slightly in the ascendancy. This has been despite some significant local events including two rate cuts from the Reserve Bank; a very close election result and the aftermath of the May Budget.

International events have hardly been without highlights including the vote by the British people to leave the European Union (‘Brexit’) and a particularly volatile US presidential election. On the other hand anxieties around China have definitely settled down and the prices of Australia’s major commodity exports have been particularly buoyant.

This stability is signalling a sustained lift in Consumer Sentiment over the last year. The average level of the Index over this last stable six months is now 4.9% higher than the average of the same six months a year ago. However that boost is all in expectations. The “Current Conditions components of the Index have been steady while the Expectations components of the Index are up 8.1% on the previous year. This boost to expectations has been sustained. Certainly there was a 4.4% lift following the change of Prime Minister a year ago but the Expectations Index has lifted a further 5.2% since last October.

The only disappointing aspect of this story is that the component of the Index which measures how respondents feel about their own finances relative to a year ago has fallen by 2.9% (on a six month average basis) whereas the component that tracks their outlook for finances over the next 12 months has lifted by 2.2%.

The largest average boost of the components has been the outlook for the economy over the next 12 months which has lifted by 13.1% on a year ago (on a six month average basis).

Ongoing stability in the labour market has been one likely explanation for the overall boost to confidence. The Westpac Melbourne Institute Index of Unemployment Expectations dipped from 138.4 to 138.2. The average print for the Index over the last six months is 138.2 – emphasising the stability of the current assessment of the labour market. This average read is 8.0% below the average of the same six months a year ago indicating a definite improvement in respondents’ assessments of the conditions in the labour market.

There were generally minimal movements in the components of the Index over the month. The ‘family finances compared to a year ago’ sub-index fell by 0.4% while the ‘family finances over the next 12 months’ sub-index lifted by 0.9%.

The ‘economic conditions over the next 12 months’ sub-index lifted by 5.8% while the ‘five year’ outlook was unchanged. The ‘time to buy a major household item’ sub-index fell by 0.4% but is still up by 9.2% over the year. The average reading for this component over the last six months is up 3.3% on the average six months reading a year ago.

Confidence in housing faded in October. The ‘time to buy a dwelling’ Index fell by 3.3% in October from 105.7 to 109.3. There was a particularly sharp fall in the NSW Index – down by 10.5% with the Sydney Index down from 101 to 82.2 (–18.6%). However if we consider the average of the ‘time to buy’ index over the last six months relative to the same period a year ago the Index is around 2% higher. In the case of the volatile Index in NSW we can see a 14.7% improvement while the Sydney index has improved over that period by 34%.

Confidence in house prices continued to improve. The Westpac Melbourne Institute Index of House Price Expectations increased by 1.6% in October to be 12.1% above its level in October last year. House price expectations in NSW lifted by 2.6% in the month to be 20% above the level a year ago. There have been solid improvements in expectations across the major states over the year with Victoria up by 6%; Queensland by 9% and Western Australia by 15%. With vacancy rates rising and prices falling in Perth we had been surprised by the resilience in respondents’ expectations for prices in WA although this month we have seen a disturbing 16% fall in expectations in one month.

The Reserve Bank Board next meets on November 1. A significant number of commentators have been predicting a rate cut in November and a few weeks ago markets had been giving around a 50% probability to a move. We were never convinced that the inflation report which is due to be released on October 26 would provide the case for a cut. In fact, with a 0.3% reading for the underlying inflation dropping out, it seems likely that the September quarter report will actually show that annual underlying inflation has lifted.

It has also become clear that the new Governor will give considerable weighting to ‘financial stability’ in his policy deliberations. With Sydney house prices having been reported to have lifted by 3.5% and Melbourne by 5% in the last three months the risks of further boosting housing with another rate cut will be a significant consideration for the Board. While the results of today’s report point to some short term deterioration in housing sentiment the longer term picture is clearly still positive.

Indeed while we give little probability to a further rate cut at the next meeting our assessment of the growth outlook, including the shape of the construction cycle, points to rates remaining on hold for the foreseeable future.

Way to over-egg it, Bill. If we cyclically adjust the index – that is look at where it is relative to where it would normally be at this point in a maturing business cycle – the current levels remains somewhere between luke warm and room temperature, notwithstanding the recent improvement from simply awful.

Still, I agree that the RBA is on the sidelines for a goodly period. Ceterus paribus H2 2017 looks like the next pit stop for cuts as the current purple patch passes into renewed income shock, dwelling downturn, car industry closure and mining capex cliff.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.