Commonwealth Bank of Australia and other lenders are toughening conditions on popular investment property loans in response to regulatory pressure to clamp down on interest-only products.

Lenders are also repricing many of their other products by offering selective discounts and targeting the most attractive sectors, rather than racing for volume with across-the-board cuts.

CBA, which flagged tougher lending conditions for interest-only borrowers back in July, is offering 10-year interest-only terms for borrowers that live in the dwelling. Those with an investment loan have up to 15 year’s interest only and principal and interest for the remainder of the term.

It’s good timing even if manifestly not enough from APRA. CBA and WBC have been leading a small revival in investors loans:

ANZ

CBA

MQG

NAB

WBC

BOQ

BEN

SUN

Aug-16

80605

133134

9051

98221

138350

11645

11024

11839

Jul-16

80859

132274

9137

97829

137514

11773

10915

11878

Jun-16

81305

131298

9191

97544

136918

11901

10865

11886

May-16

81713

129801

9197

97450

136070

11978

11546

11685

Apr-16

82073

128671

9215

97045

135754

12029

11478

11445

Mar-16

82270

128065

9220

96825

135712

11981

11370

11322

Feb-16

82469

127835

9221

96531

135351

11919

11243

11332

Jan-16

82656

127872

9257

96114

135471

11680

11229

11414

Dec-15

82766

128018

9269

95749

135279

11470

11258

11475

Nov-15

82722

127957

9311

95278

135372

11295

11280

11595

Oct-15

82718

128396

9253

94384

134938

11166

11292

11701

Sep-15

82911

129616

9264

94019

149687

11062

11266

11800

Advertisement

But as UBS pointed out earlier this week, it’s all far too late:

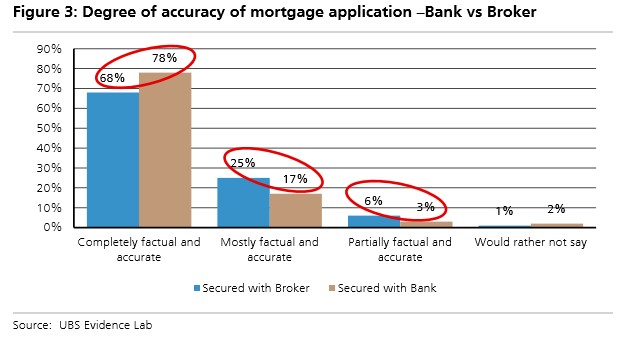

The most significant findings of the survey were (1) Only 72% of respondents stated their application was “completely factual and accurate”. 21% stated they were “mostly factual and accurate”, 5% stated they were “partially factual and accurate” while 2% “would rather not say”; (2) 32% of respondents who secured a mortgage via a broker stated they misrepresented some element of their application, compared to 22% who secured a mortgage via bank distribution; (3) More concerning, 41% of respondents who used a broker in 2016 and misrepresented elements of their application stated they did so based on their broker’s suggestion (vs 13% for bank channel equivalent)…

Of the 344 respondents who stated they misrepresented parts of their application: 14% over-represented household income (18% of those who used brokers and 5% who used bank networks); 13% overstated other assets; 17% under-represented other financial liabilities; 26% under-represented living costs; 11% “other”; 31% “would rather not say”. 12% stated they misrepresented multiple factors.

Unfortunately survey results suggest misrepresentation is systemic with findings similar across the 2015 and 2016 Vintages, price to income levels, LVR, owner occupiers and investors. However, there was a correlation between borrowers who misrepresented their application and: those whose expenditure was broadly equal to their income; stated they are under financial stress; or have missed a debt payment…

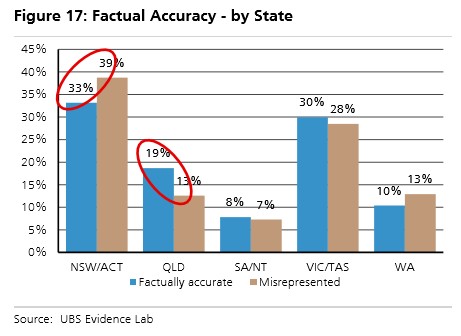

Interestingly customers who come from NSW were more likely to misrepresent their mortgage applications. Notably this continues to be the most buoyant housing market in Australia. Customers from Queensland are more likely to be factually accurate.

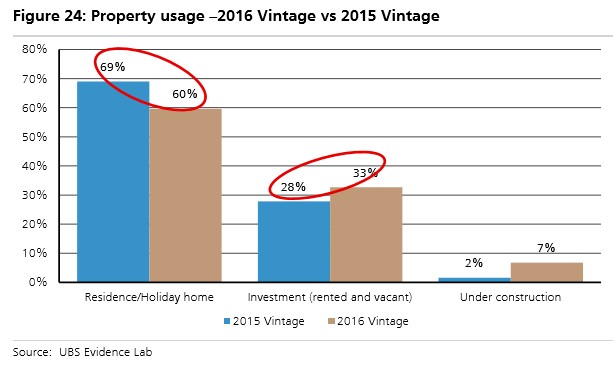

Finally, the use of mortgages for investment purposes accelerated in 2016 contrary to the banks’, RBA and APRA’s data…

We believe this ties in with the ‘areas of less factual accuracy’ section above. This may suggest some customers were not factually accurate when stating the purpose of the loan, especially given the higher interest rate which has now been introduced on Investment Property compared to Owner Occupied mortgages.

What does this mean?

We believe these results are disturbing given: the recent housing market reacceleration; elevated household leverage (186% debt to income); and mortgages accounting for 62% of bank loans.

While banks have tightened underwriting following APRA’s ‘sound lending’ guidance, it does not appear to have prevented applicants ‘stretching the truth’. While low unemployment and rising house prices may help prevent losses near term, more rigorous auditing of applications appears essential, especially via brokers…

We believe it is more important than ever that the banks tighten their mortgage underwriting standards and ensure applications are factually accurate. We continue to see the mortgage broker network as a potential area of weakness in this process.

After what they did to the US housing market, these loans should simply have been banned.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.