Another upgrade to our housing forecasts; & update to our (2018) supply peak

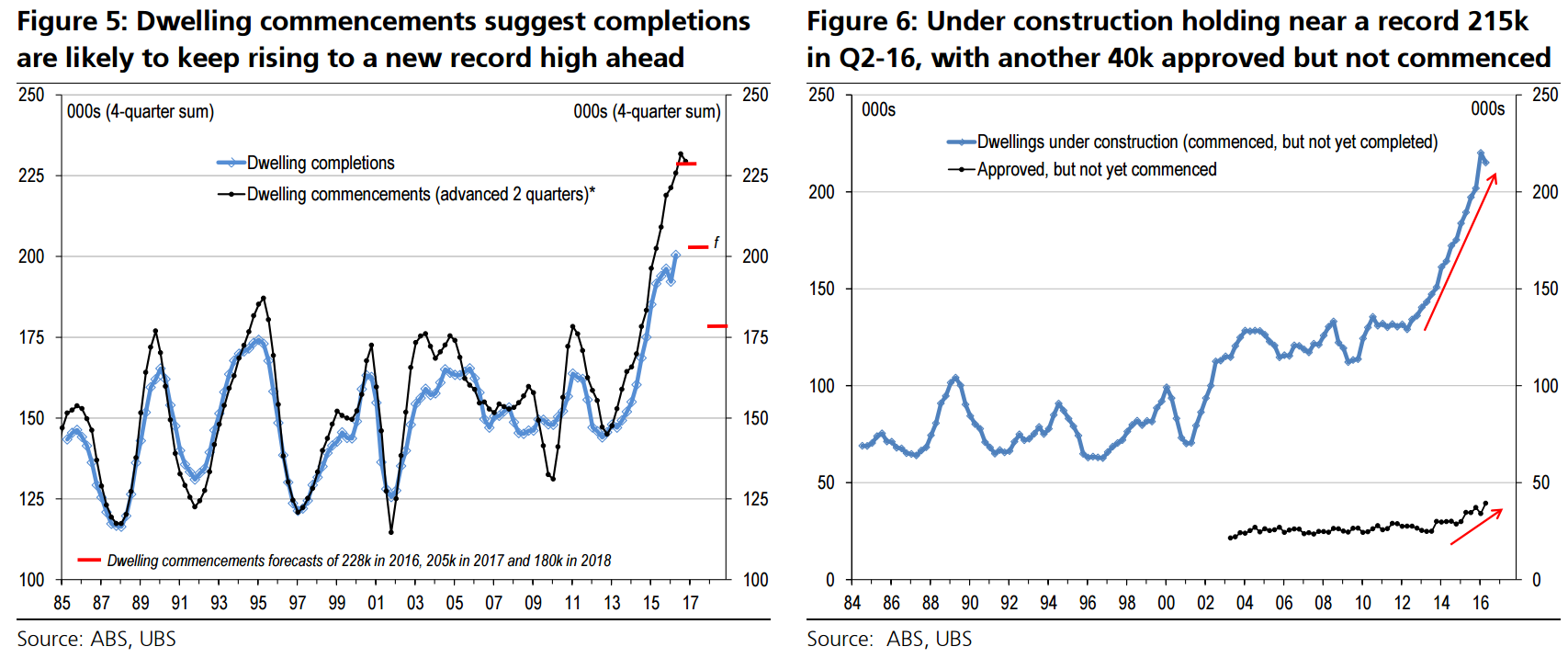

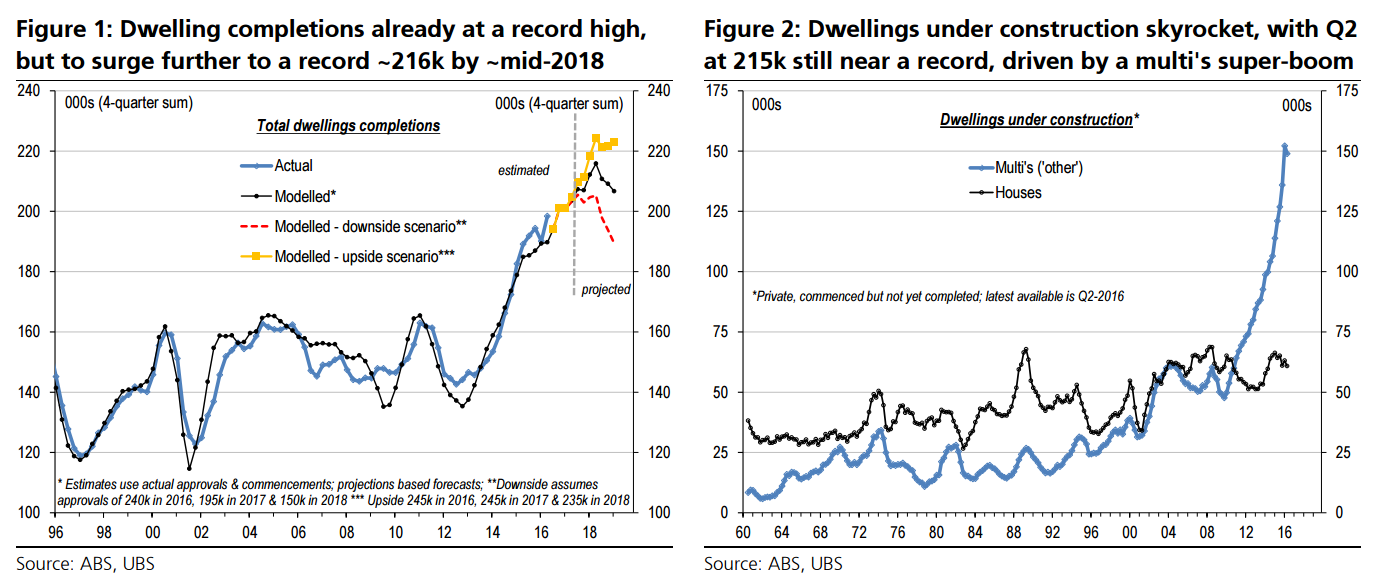

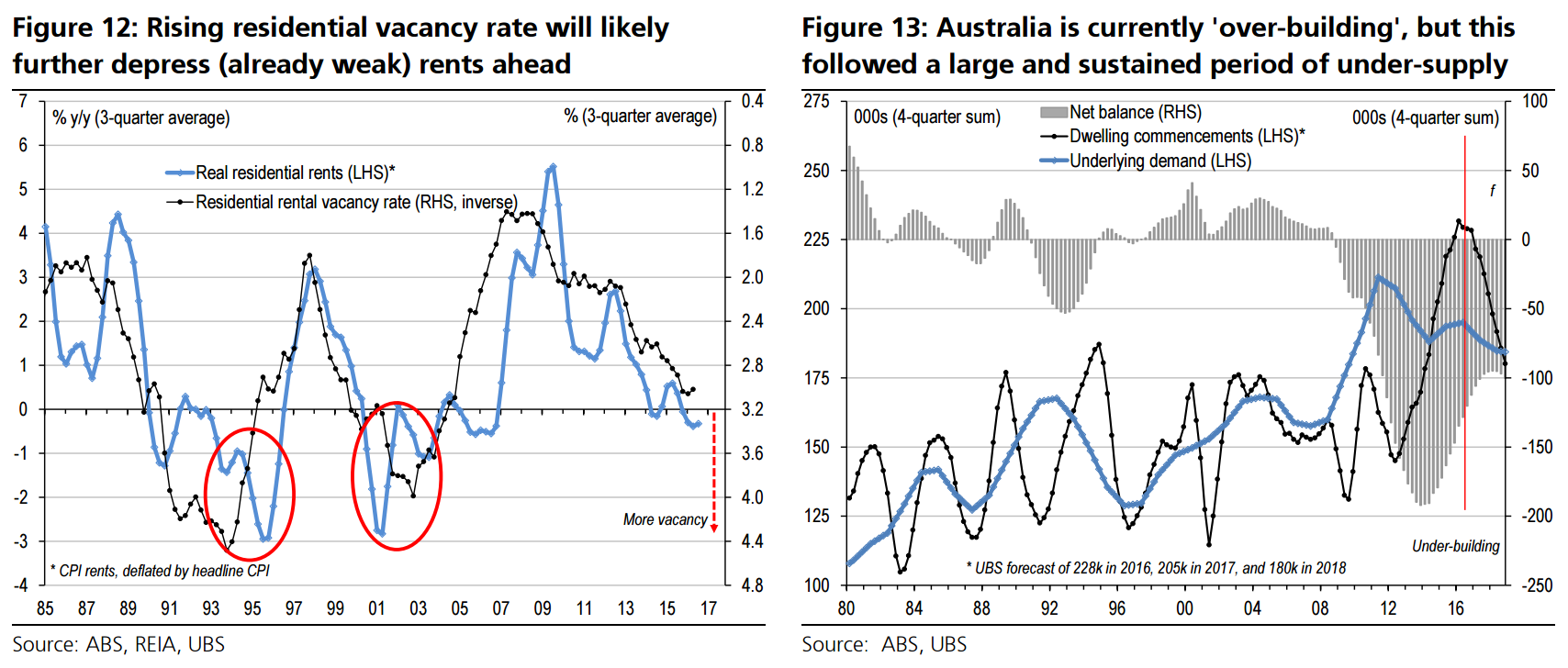

While Q2 dwelling commencements retraced 9% q/q, they’re still booming at 220k a.r., & followed an upwardly revised record 243k a.r.. Indeed, more recent approvals rebounded in July/August to a record 252k. Hence, we upgrade our commencements forecasts again. 2016 is raised to a record 228k (was 217k), but we also lift 2017 to a still strong 205k (was 190k), before a sharper moderation to a still solid 180k in 2018.

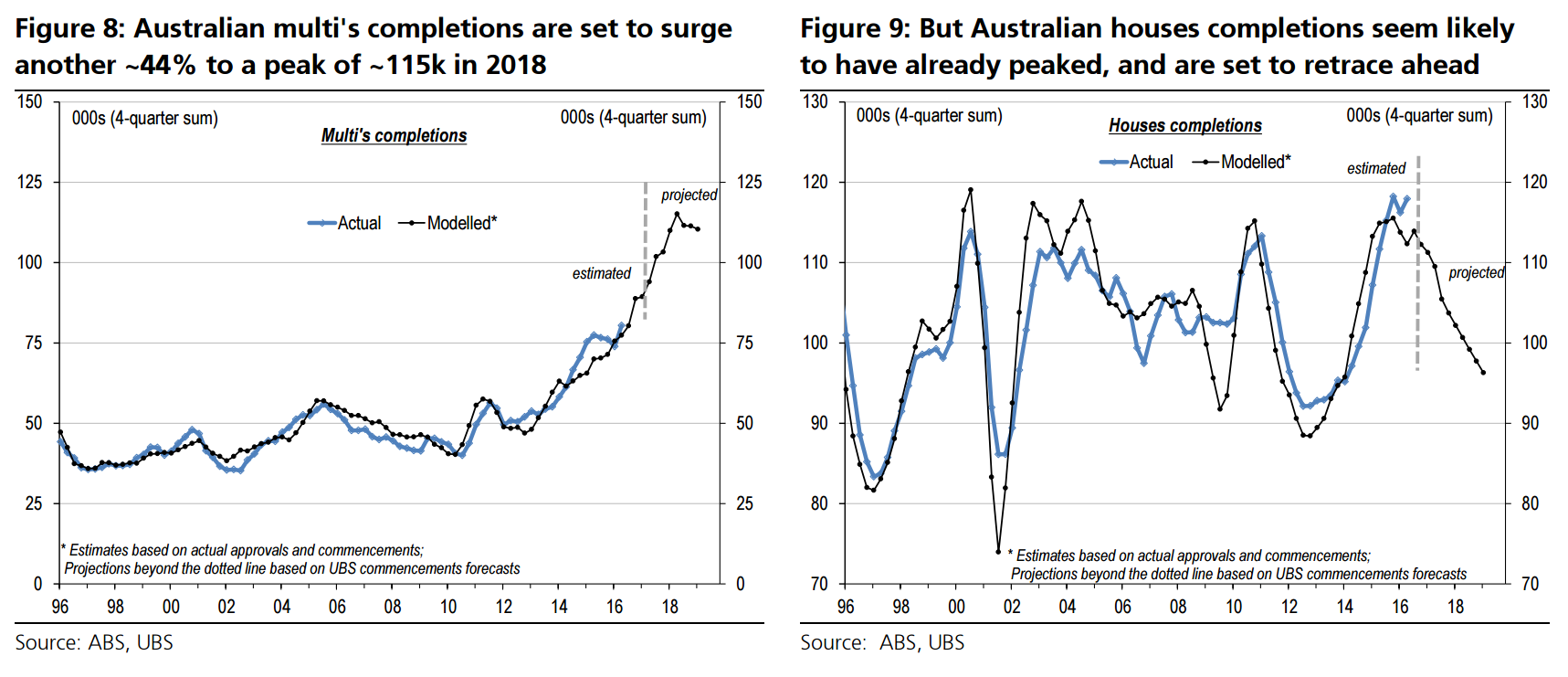

We also update our ‘UBS supply tracker’ models. With completions lifting to a record in Q2-16, we estimate the ‘completions cycle’ is now ~79% done (was 68% as at Q1 in our initiation). Since the trough of annual completions at 144k back in Q3-12, we look for a cumulative 50% lift to a peak of ~216k by Q2-18 (a similar level and timing as our initiation). However, within this, completions of houses already peaked last year. In contrast, the multi’s (i.e. ‘other’, mainly 4+ storeys) super-cycle is still only ~half done, with the level of completions likely to end up well over double the pre-boom trend.

We also provide upside/downside scenarios. Even if approvals collapse from now, given ~record dwellings under construction, completions will stay elevated out to 2018. By State, the largest rise in supply is in NSW, albeit Victoria had arguably been booming since the GFC (driven by multi’s, while houses are peaking). Notably, WA & SA likely peaked already, but QLD is set for another lift over coming years, after flattening out.

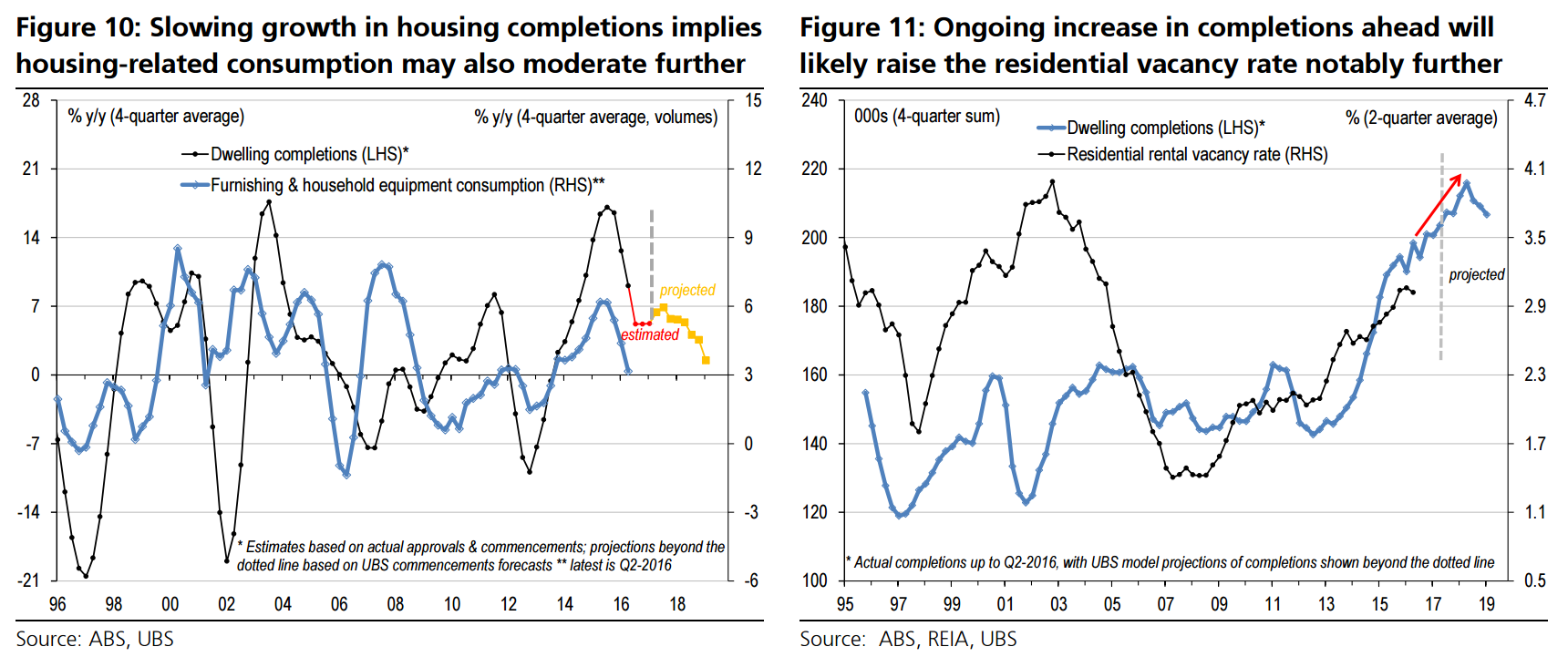

Since our last ‘crane-count’ update, housing has been stronger than (we &) the RBA expected. Indeed, we upgrade prices for end-16 to 7% (was 5%), but stick to ~flat in 2017, given more supply. Nonetheless, the ‘big picture’ suggests the RBA’s rate cuts delivered a greater risk of ‘better now, but worse later’ scenario for housing, given a UBS Evidence Lab survey showed material misrepresentation of mortgage applications, amid tighter lending conditions particularly to foreigners. We continue to expect the RBA to hold ahead, given new Governor Lowe’s increased focus on financial stability.

Wowsers! We still see the balance of risks titled towards the contribution to growth with an earlier peak. There is strong suggestion of a double top in approvals that hints at a peak plateau rather than sharp top.

Anyway you cut it, though, the message is clear. Straya is headed for a monumental housing glut because:

once the building stops there is nothing else to drive the economy so it is currently catering to some element of phantom demand and is by definition a massive overshoot, and

the political imperative of lower immigration is rising as a major risk indeed inevitability so the longer term prospects for back-filling the surplus are declining.

Advertisement

This is the dying Chinese economic model bought to Australia, quite literally by its banks and developers :

We’ve never seen a cycle like this before. Aussie banks woke up to it a year ago and stopped lending but they’ve been out-flanked. Australian housing is being Chinarised with massive over-building leading to immovable gluts followed by stagnant and falling prices.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.