We expect a 165k increase in nonfarm payroll employment in August, below consensus expectations for a 180k gain. …

The unemployment rate is likely to decline to 4.8%, while average hourly earnings were likely flat in August and up 2.3% over the past year.

…Our below-consensus forecast primarily reflects seasonal quirks specific to the August payroll period. Since 2011, August payroll growth has fallen short of Bloomberg consensus expectations by an average of 49k, only to be revised up by an average of 71k in subsequent releases. Industry-level payroll data indicate that the education sector (specifically, education services and state & local government employment, the latter largely reflecting public schools) accounts for much of the upward revision, which mostly occurs from the first to the second estimate of payroll growth. In our view, the initial August weakness and subsequent revisions reflects seasonal adjustment challenges related to shifts in the timing of school calendars. Since this pattern failed to hold last year, we are estimating a more conservative 20k impact this year.

The August employment report has come to be seen as the deciding factor in the Fed’s upcoming decision on rates. See Sam Fleming at the Financial Times here. Maybe this is the case, maybe not. I hope not. Hinging policy on the first print of nonfarm payrolls – a volatile, heavily revised number – would be pretty low quality policy making.

I keep coming back to this by Federal Reserve Chair Janet Yellen from back in December:

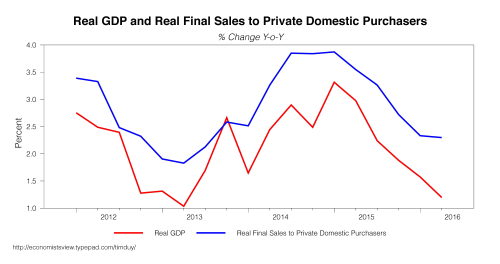

…total real private domestic final purchases (PDFP)–which includes household spending, business fixed investment, and residential investment, and currently represents about 85 percent of aggregate spending–has increased at an annual rate of 3 percent this year, significantly faster than real GDP. Household spending growth has been particularly solid in 2015, with purchases of new motor vehicles especially strong.

This was Yellen’s way of justifying a rate hike last December in spite of faltering GDP numbers. Trouble is that PDFP continued a downward slide since then:

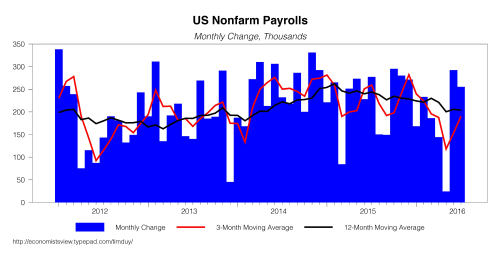

Final sales here are off roughly 1.5 percentage points from their cycle highs. That is a nontrivial swing. It is no wonder that job growth accelerated in 2013-14 and then decelerated in 2015:

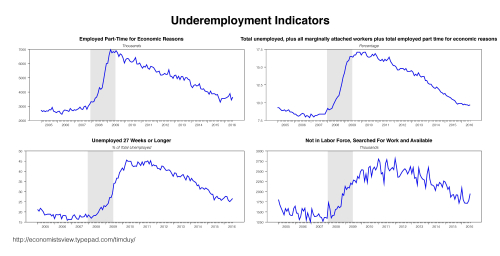

I tend to think there is room for some further deceleration. Note too that progress on reducing underemployment slowed markedly:

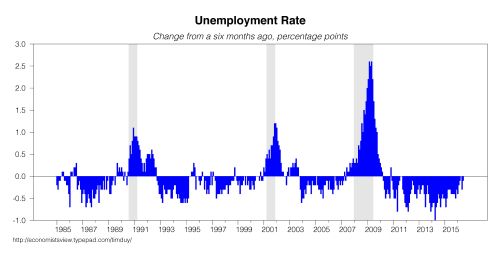

and the unemployment rate is flattening out:

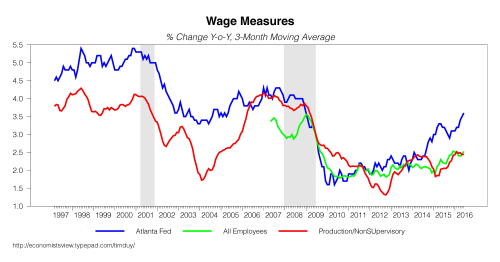

Now, you might say that the Fed needs to hike because wages are rising. But I would say that wages are a lagging indicator

and are likely to continue rising even after a recession begins. Overly shifting the policy focus to wage growth would be a red flag in my opinion. I think the Fed tends to focus too much on lagging indicators in the later stages of a business cycle while ignoring their own policy lags. The end result is overly tight policy.

So when I look at the data, I don’t see that the August employment report should be a critical factor in a rate hike decision. I think the critical factors should be the Fed’s confidence that growth is set to rebound in the second half of the year and the balance of policy risks.

On the first point, while early signals on growth are positive – see the Atlanta Fed GDPNow measure, for example – they are still just early signals. And today’s ISM release doesn’t indicate that a manufacturing rebound is right around the corner, so maybe that rebound in investment spending just might take more time as well. And auto sales look to have peaked and are flattening out, so that is not likely to be a source of growth and might be slight drag. So, overall, I don’t think we have enough data to be confident that growth will rebound just yet.

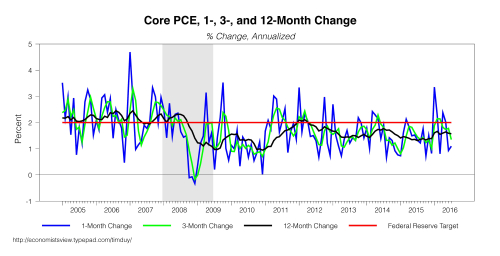

Regarding the balance of policy risks, that asymmetry has not magically gone away. The Fed has less room to ease than tighten. And inflation remains mired below

So I don’t see that that the basic calculus here has changed. If the Fed errors by being too loose now, they have plenty of wiggle room on inflation and policy to respond. If they error on by being too tight, they don’t have much policy room and they risk holding inflation below 2 percent for another decade. What’s that going to do for inflation expectations?

All that said, there appears to be a movement among FOMC members to minimize the asymmetry of the policy risks. First you have Federal Reserve Vice Chair Stanley Fischer arguing that inflation is close enough to target that it shouldn’t be a concern. Via Greg Robb at MarketWatch:

And the core measure of the personal consumption expenditure index — the Fed’s favorite measure of inflation — at 1.6% “is within hailing distance” of the central bank’s 2% target, Fischer added.

I am starting to think Fischer is still living in the 1970s. But perhaps more disconcerting is Yellen’s final line from her Jackson Hole speech:

But even if average interest rates remain lower than in the past, I believe that monetary policy will, under most conditions, be able to respond effectively.

She is playing down the asymmetric policy risk issue here. Given the experience of the past decade, she is way too complacent in my opinion. And her complacency hinges on the assumption that they now know they (nominal) natural rate of interest is 3 percent. But that has been a moving target. And I don’t think that is the signal being sent by the long end of yield curve.

Then there is the financial stability argument. All I will say on that is the Fed had better be damn certain that they are facing a real risk to the economy before they pull the trigger on that argument. And I don’t see how they can be that certain.

Bottom Line: Regardless of the outcome of the employment report, good or bad, I don’t see good case for moving next this month. Too many questions about the forecast, and they still face persistently low inflation and asymmetric policy risks. But all that said, there seems to be a large swath of voting members ready to get behind a rate hike. I think the low odds on a rate hike in September is the market’s way of telling the Fed that if they do hike, it would be a mistake.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.