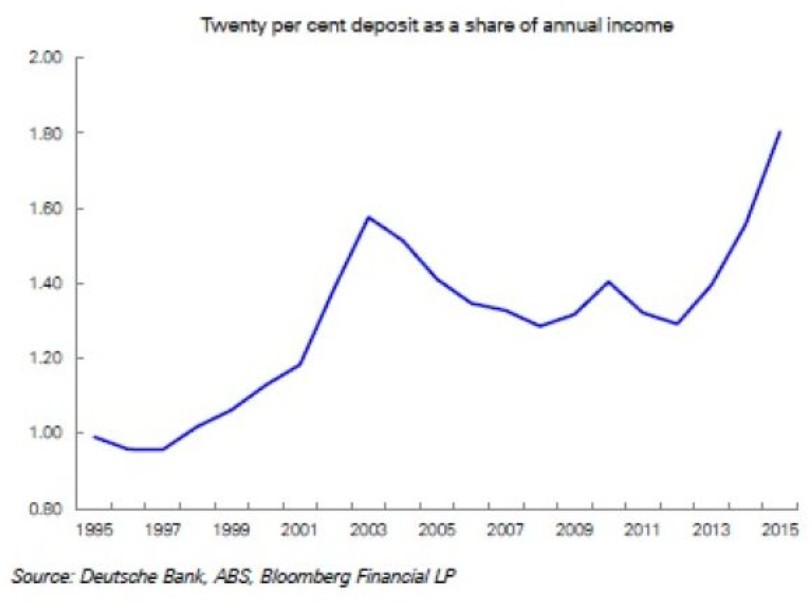

Escalating home prices against sluggish wages growth has driven the deposit gap facing Sydney first home buyers (FHBs) to record highs, according to new research from Deutsche Bank. From ABC News:

Research by Deutsche Bank’s chief Australian economist Adam Boyton shows it would take a 25 per cent drop in Sydney home prices to bring the size of deposit required back to average levels over the past 20 years…

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.