Australia’s government bond rating affirmed at Aaa with a stable outlook On 17 August 2016, we affirmed Australia’s Aaa government bond ratings. The factors supporting the rating affirmation are: (1) our expectation that Australia’s demonstrated economic resilience will endure in an uncertain global environment, (2) a very strong institutional framework, and (3) stronger fiscal metrics when compared with some similarly rated peers—despite the increase in government debt levels from previously low levels—and which we expect will remain consistent with a Aaa rating over the medium term.

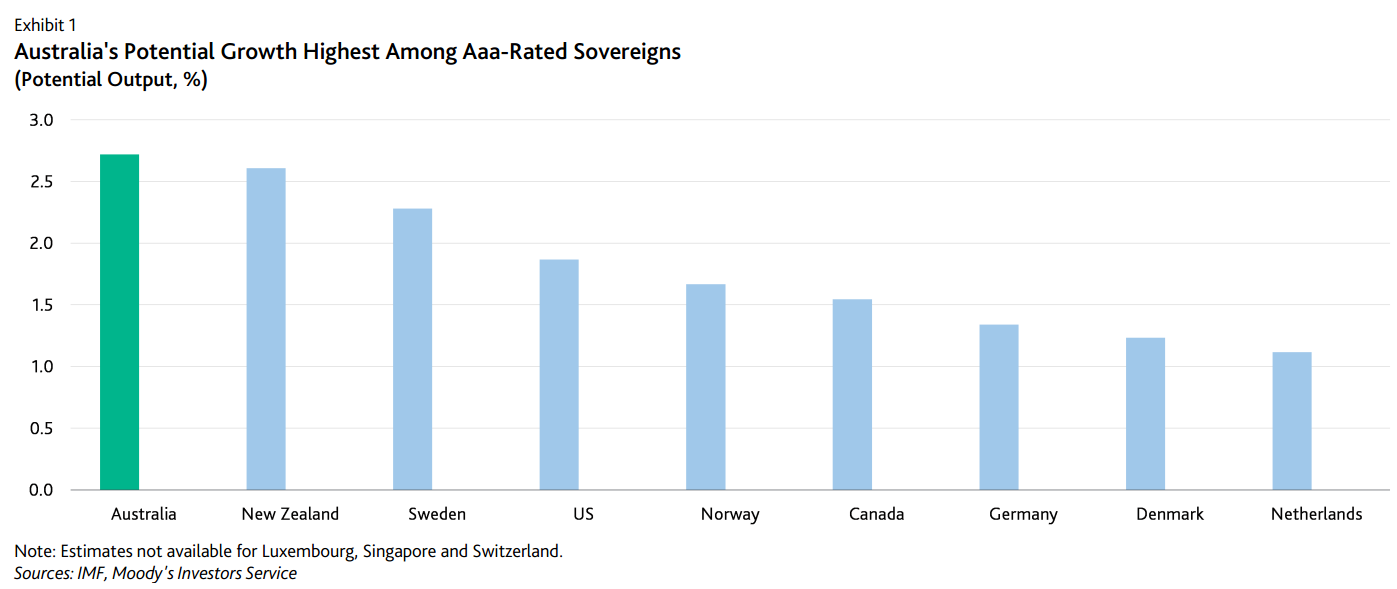

Australia’s large size, high income levels, competitiveness, flexibility and growth record combine to offer exceptional economic strength, which supports in turn its Aaa rating. The economy is quickly and effectively adjusting to lower commodity prices that have dampened a significant source of revenues and incentives to invest in the country. As a result of the deterioration in terms of trade, nominal GDP growth has slowed, and we expect it to remain moderate over the next few years. However, with a flexible labour market, a rapidly adjusting exchange rate and low interest rates, some services sectors—in particular tourism, education and housing construction—have grown rapidly, creating jobs and supporting incomes in the economy. As the shift in economic activity continues, we expect real GDP growth to remain robust, at around 2.5% from 2017 onwards, after registering 2.8% in 2016. Growth in services will continue to support employment and household incomes and consumption. We note that few high-income economies are growing at similar rates. Over the longer term, Australia’s potential growth is higher than that for most Aaa-rated sovereigns (Exhibit 1). In particular, the country’s population growth is stronger, aging is slower, and financial provisions for an aging population are more advanced than in many advanced economies.

Very strong institutional and policy framework

Australia’s monetary policy and banking regulation and supervision are vigilant and responsive to economic and financial conditions. The Reserve Bank of Australia (RBA) has a very long track record of delivering stable inflation at moderate levels. Compared with many other central banks in advanced economies, the RBA has retained more space for conventional monetary policy, the effectiveness of which is better established than that of unconventional measures. On banking regulation and supervision, the Australian Prudential Regulation Authority (APRA) has implemented measures that should diminish the probability and reduce the negative consequences of a potential downturn in housing. These measures include: limiting investor lending growth to 10% annually; imposing a minimum serviceability buffer of 2 percentage points above the standard variable interest rate on new loans or a floor of 7% (whichever is higher); and ceasing high-risk lending practices, such as writing excessive numbers of interest only loans, loans over very long terms (greater than 30 years) as well as writing too many loans at high loan-to income and loan-to-value ratios.

Fiscal metrics remain stronger than many Aaa-rated sovereigns

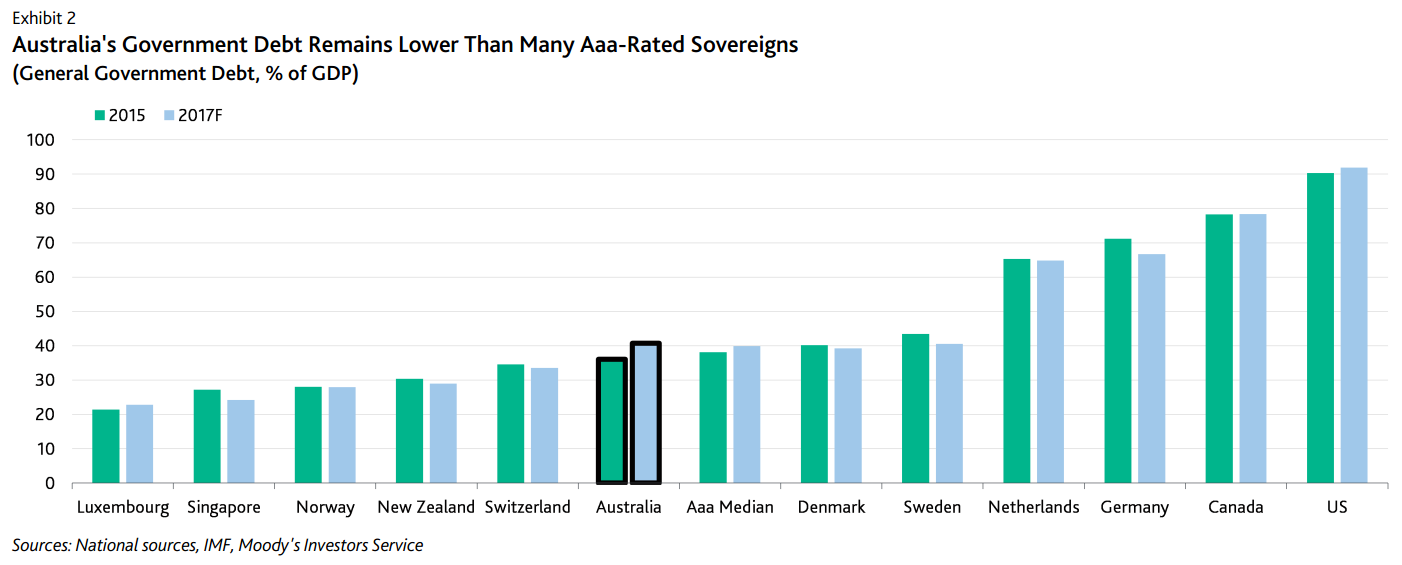

At 36.1% of GDP in fiscal 2015, Australia’s general government debt was somewhat lower than the 38.1% median for Aaa-rated sovereigns. However, government debt has increased markedly from the 19% of GDP in fiscal 2010. We expect it to rise further over the next few years, because fiscal consolidation has proved challenging. Moderate nominal GDP growth will continue to dampen government revenues, while the government faces political hurdles in implementing fiscal tightening measures, given that it rules with a very thin majority in the House of Representatives and a splintered Senate. The effectiveness of fiscal policy could therefore be undermined. Against this backdrop, we forecast that government debt will rise to close to 41% of GDP by fiscal 2017 and to just under 45% by the end of the decade. Nevertheless, Australia’s debt burden—while rising and no longer at low levels—will remain consistent with a Aaa rating, and will be lower than some other Aaa-rated sovereigns such as Canada or the Netherlands, and not significantly higher than Sweden’s or Denmark’s (Exhibit 2).

We expect the strength of Australia’s institutions and its moderate debt burden to continue to shore up domestic and international investors’ confidence in the creditworthiness of Australian assets, thereby maintaining the cost of debt at low levels.

Rationale for stable outlook

The stable outlook on Australia’s rating reflects our expectation that Australia’s credit profile and related metrics will remain consistent with a Aaa rating, and resilient to potential negative shocks. Australia is exposed to two types of shocks. First, the rise in and level of Australian household debt, fuelled by rising house prices, is large by international and historical standards, and pose a potential source of vulnerability in the event of a downturn in the housing market. At the end of 2015, household debt amounted to 124.3% of GDP, a result which was at least 25 percentage points above that of any other high-income economy except for Denmark (Aaa stable, 122.5%). Australian household debt levels are also higher than in the US (Aaa stable), Ireland (A3 positive) and Spain (Baa2 stable), and equivalent to these countries’ housing peaks during 2007 of between 78.2% and 95.4% of GDP. Second, the Australian government and private sector’s dependence on external financing is a source of vulnerability because it exposes the domestic financial sector to global developments. Foreign investors can also at times shift their investments to different markets more suddenly than domestic investors would. Nonetheless, there are factors that mitigate the potential sovereign credit impact of both the above risks. Should house prices fall significantly, the strong capitalization of Australian banks—and in general their high intrinsic financial strength—significantly reduce the risks of a banking crisis and the eventual costs for the sovereign. Meanwhile, the robustness of Australia’s institutions bolsters the attractiveness of Australian assets to foreign investors and reduces the risks derived from significant dependence on external finance. Moreover, in the case of a downturn in the housing market or a tightening in external financing conditions, scope for monetary and fiscal policy stimulus would combine with the shown resilience of the economy to mitigate the negative impact on overall economic activity. The economy’s resilience creates in turn a floor to the potential weakening of fiscal metrics in such scenarios.

RATING RATIONALE

Our determination of a sovereign’s government bond rating is based on the consideration of four rating factors: Economic Strength, Institutional Strength, Fiscal Strength and Susceptibility to Event Risk. When a direct and imminent threat becomes a constraint, that can only lower the preliminary rating range. For more information please see our Sovereign Bond Rating Methodology.

A nice backwards looking rating. Just a few questions:

if the sovereign is so strong why are the banks on downgrade watch given they’re publicly guaranteed?

why does Moody’s see such strong institutional frameworks when it doesn’t believe our Budget outlook?

why does Moody’s reckon that Australian public debt will remain so low during the next shock? The last one took it from -5% to today’s 36% and that was with a mining boom.

The answers to these questions mean that the Australian sovereign will definitely blow through AAA metrics during the next shock, which means today’s result is not discounting future risk, the role of a credit rating.

Over the S&P next to see what the grown-ups think.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.