by Chris Becker

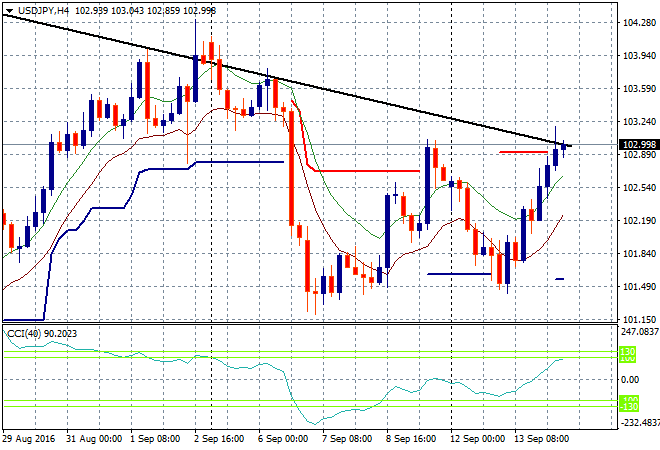

A sea of red across Asian bourses following the selloff on risk markets overnight, as bond markets extend their volatility as Australian sovereigns and long dated Japanese bonds are sold off with all the bids going to the short end of the yield curve. Japanese stocks led the charge down, possibly pushed by the poor industrial production print for August, with the Nikkei losing 0.8% even as Yen sells off, with the USDJPY almost breaching the 103 level and its long term downtrend:

The Shanghai Composite is dicing with terminal support, currently down 0.5% to just over 3000 points going into the close, while the Hang Seng is holding on to a scratch session.

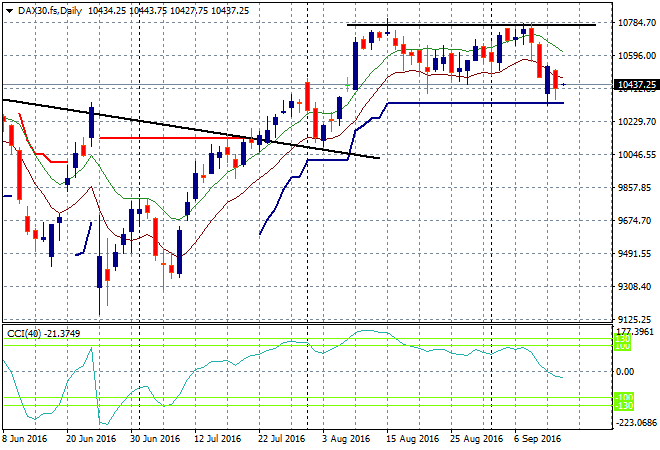

The ASX200 slumped at the open, but has recovered and closed approx. 0.4% as short covering continued across bank stocks, in anticipation of a bounce on European bourses tonight. I don’t see it – consider the German DAX daily chart below – which is tentatively poised here and ready to break down if the ECB doesn’t change its “don’t care” tune soon:

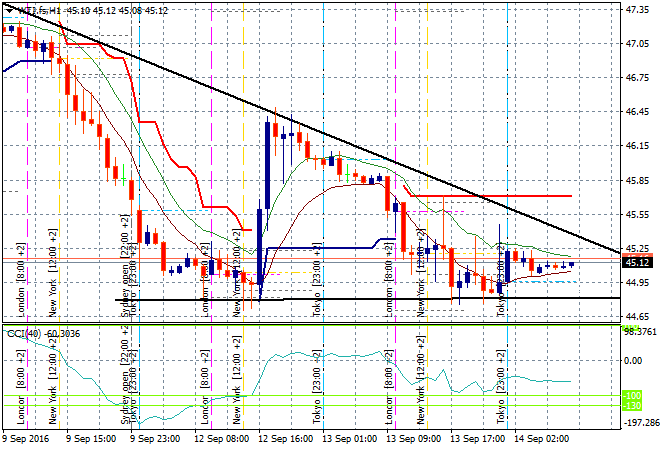

Turning to commodities I’m watching oil closely with DOE inventories reporting tonight. The hourly chart of the WTI contract is showing a nearly completely descending triangle with support to watch just below $45USD per barrel:

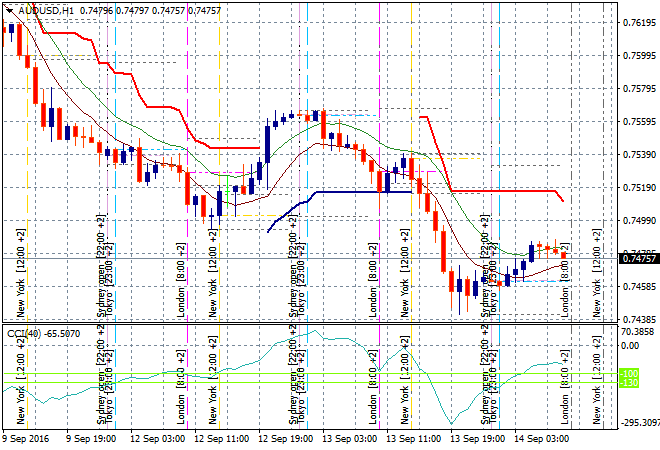

Meanwhile in currencies, the Aussie dollar is eking out a minor lift in the Asian session that is already reversing now. I would contend the 75 handle won’t hold here tonight and we’ll see a repeat of last nights action, down to 74 cents or lower:

The data calendar rolls on tonight with mid tier releases to watch out for – UK unemployment stats, EZ industrial production and DOE oil inventory reports.