Market (hub)-based gas prices have been dominant in North America for the past quarter century. The UK has had a similar mechanism for nearly 20 years and, since 2008, major continental European gas markets have made a transition away from oil-linked to market prices. But in all of the major gas markets of these regions, prices were related to (domestic or imported) pipeline gas, with LNG as a marginal source of supply. The exception is Spain where – due to the infl uence of LNG and lack of pipeline links to the rest of Europe – oil-related gas prices remain dominant, largely due to Asian LNG prices remaining tied to the traditional JCC crude oil-related formula. Because two-thirds to threequarters of global LNG cargos are delivered to Asian markets, in particular Japan, Korea, and Taiwan, changes in pricing in those markets will be crucial to the overall future pricing of LNG. Long-term Asian LNG contracts have traditionally been based on JCC (colloquially known as the Japan Crude Cocktail) pricing, according to which the LNG price is based on, and indexed to, an average of the prices of crude oils imported into Japan.

The 2010–16 period: peak followed by collapse

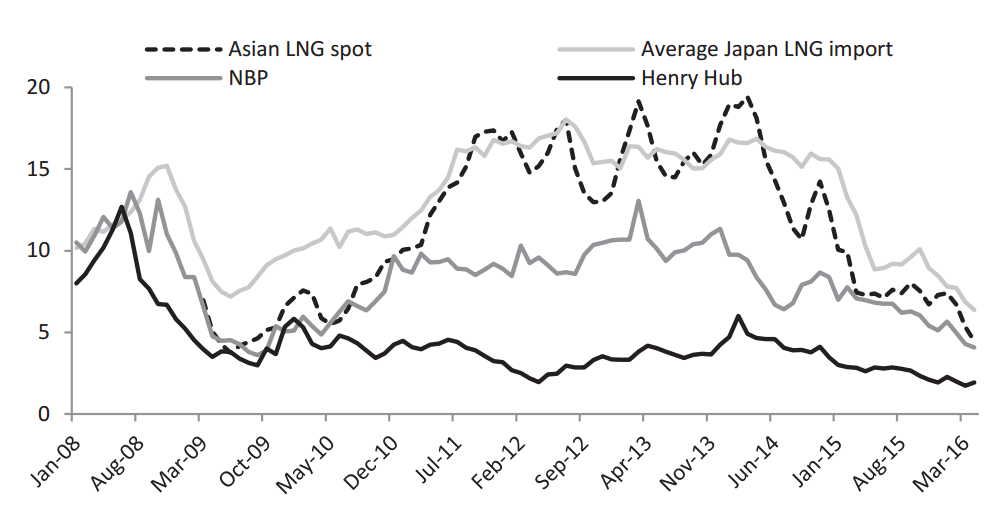

By 2010 it had become clear that although market fundamentals differed between the Asian LNG importing countries, even in countries such as South Korea, India, and China where oil products remained important competitors to gas, 100 per cent linkage to crude oil (let alone to Japanese crude oil imports) had ceased to be a logical way to price LNG. In 2011, two major events occurred in Asian LNG markets: oil prices rose and remained above $100/bbl, and the Fukushima nuclear accident (and subsequent closure of all Japanese nuclear power stations) created signifi cant additional demand for LNG which had not been foreseen. The result was that LNG imports rose substantially – mainly in Japan, but also in China where gas demand was increasing in double digits annually. These sudden, and unforeseen, additional requirements led to companies having to rely on spot and short-term cargos – bid away from Atlantic Basin (principally European) markets often at even higher prices than JCC at $100/bbl equivalent – to meet their demand. The result was huge differences in regional gas prices with Asian (and particularly spot) LNG substantially above European and North American prices (shown in the fi gure ‘Asian LNG prices compared with NBP and HH’).

Since 2014, oil prices have fallen from more than $100/bbl to around $45–50/ bbl by May 2016. Asian LNG prices fell from highs of $15–18/MMBtu (and higher for spot prices) to less than $5/MMBtu in the second quarter of 2016. Over this period, regional gas price differentials have narrowed substantially, with the spread between US gas prices and those of Europe and Asia narrowing from $6 and $11/MMBtu respectively in early 2014, to $2 and $5/MMBtu respectively by early 2016. Within a very short time the famous ‘Asian premium’ in relation to LNG import prices had disappeared. (It is a little diffi cult to fi nd a precise defi nition of the ‘Asian premium’ but it generally refers to excess prices paid by Asia– Pacifi c countries for oil and gas relative to those paid in other regions for the identical products.)

Henry Hub-based pricing

The 2010–14 period had forced Asian buyers to consider a number of different options, including spot indexation and pricing at different hubs. During that period, a number of tolling (and modifi ed tolling) contracts were signed for imports of US LNG which would result in Asian buyers signing 20 year contracts containing a formula of: 1.15 times the Henry Hub price, plus a fee for liquefaction (in the range of $3–3.5/MMBtu) plus transportation. While this formula looked very attractive in comparison with JCC when Henry Hub prices were at $2–3/MMBtu and oil prices were at $100/bbl, the benefi t very much reduced, and then reversed, at oil prices below $50/bbl, especially if Henry Hub prices increase. This highlighted the importance for Asian LNG buyers of focusing on price formation as opposed to price level, and on supply/demand fundamentals in their national markets as opposed to the fundamentals in US (Henry Hub) and European (NBP/TTF) markets.

The emergence of Asian gas and LNG hubs

The logical endpoint of this process will be the development of Asian gas and LNG hubs – along the lines of those operating in North America and Europe. There are a number of different requirements for hub development, starting with third-party access to facilities and moving on to price discovery, OTC and futures trading. Eventually one or more hubs will develop with a forward curve of prices several years ahead, which is suffi ciently liquid to be accepted as a price reference for long-term contracts. In North America and Europe this process required a minimum of fi ve – and mostly closer to 10 – years (and in many European countries has yet to be completed). The only existing Asian gas hub is in Singapore, which has a liberalized gas market and where trading teams from many major companies have based their operations. Singapore has fi rstmover advantage but the disadvantage of being a physically small market with limited growth potential. Nevertheless, the Singapore hub could evolve from its current small physical status to a virtual hub encompassing the whole of south-east Asia – given the potential noted above for LNG demand growth in that region.

In Shanghai, there is a benchmark price at the city gate where gas is priced against fuel oil and LPG, but it is intended that this evolves to encompass prices of gas from a range of sources – domestic and international, pipeline and LNG. The Shanghai Petroleum Exchange is trading small quantities of LNG, but volumes are currently too small and erratic to constitute a signifi cant traded market. Thus despite the use of the term, a ‘Shanghai hub’ does not yet exist in terms of a deep liquid traded market, but there is great potential for a signifi cant gas hub to develop in that location. The likely growth in Chinese gas demand (albeit more slow than was experienced and expected a few years ago), and the diversity of sources of gas supply – domestically produced and imported, pipeline gas and LNG – are ideal conditions for the establishment of a physical gas hub. A key development will be third-party access rights to pipelines and LNG terminals which currently exist but at the discretion of the owners of those facilities.

In Japan, there has been discussion of an LNG hub for several years. The passage of liberalization legislation to open up the LNG terminals to thirdparty access in 2017 (with separation of supply and transportation functions of the main gas companies by 2022) 0 5 10 15 20 Asian LNG spot Average Japan LNG import NBP Henry Hub Asian LNG prices compared with NBP and HH ($/MMBtu) has been an important step. But this needs to be accompanied by a commitment of all parties to spot and short-term trading, and the establishment of common trading rules and regulations. The publication of the Japanese government’s LNG strategy in May 2016 demonstrated a level of seriousness which had not previously been evident. However, that strategy confi rms the likelihood that a hub will emerge in the early 2020s. Because of the lack of pipeline connections between the different regions in Japan, the initial establishment will probably need to be a physical LNG hub which in time (with greater regional pipeline connectivity) could evolve into a virtual hub for the whole of the country.

Asian LNG pricing: evolution or revolution?

The surplus of global LNG supply over demand which began in 2014, and is accelerating as new supplies come on line, will create a much larger and more liquid short-term traded market. This will be a catalyst for a more radical change in long-term contract LNG prices, leading to the use of spot indices in long-term contracts, and eventually to hub creation. This interim fi ve to 10 year period will see the evolution of hybrid pricing with short – and perhaps also longer – term contracts based on a mixture of hub (Henry Hub, NBP/TTF), spot (JKM, Argus, RIM, ICIS), and traditional JCC prices. A potential alternative is a price based on an average of all LNG (under long-term and spot contracts) imported into a specifi c market such as JLC for Japan and KLC for Korea. However, all of these can be regarded as transitional measures from which a price mechanism will eventually evolve which will refl ect supply/demand conditions on a fl exible basis, and will be accepted by the majority of Asian LNG players.

This in turn raises the question of whether such a transition can be achieved without the contractual discontinuities and litigation which have been experienced in Europe and North America. Liberalization of access to LNG terminals and pipelines could allow new players to import cargoes at prices which would signifi cantly undercut those of established utilities under long-term JCC-linked contracts. With demand not increasing as fast as expected, and perhaps falling in Japan and Korea, the established utilities could fi nd themselves losing market share to new entrants and struggling to meet their take-or-pay commitments.

At that point, established utilities would be forced to offer lower prices to prevent their customers switching to new entrants, while being contractually required to continue to take-or-pay for minimum volumes at JCC-linked prices. A consequence of such developments could be severe fi nancial hardship, and possibly litigation launched by buyers. This would be revolutionary in a region with no culture or tradition of long-term gas contract litigation, but in North American and European markets it has been a catalyst for (painful) change. Buyers must hope that by the time they face exposure to such risks, suffi cient long-term contracts will have expired for them to be able to renegotiate the volume and price terms of their contracts (or terminate them), in order to ensure a ‘smooth transition’ to a new contractual status quo. The alternative could be a ‘contractual train wreck’ of litigation with uncertain outcomes.

Hope you got through that without falling asleep. Oxford is thorough but horribly plodding and, like most academically based analysis, couldn’t make a market call to save its life.

The apposite analogy for the evolution of the Asia LNG pricing market is not what happened in Europe or the US decades ago, it is what happened to the iron ore market post-GFC when a severe market imbalance drove precipitous change to contract markets owing to the enormous arbitrages that were stake.

Advertisement

On that occasion the changes were driven by suppliers but, if anything, the glut in LNG is a more extreme imbalance today than was the shortage of iron ore then with as much as 25% of global supply capacity in danger of being idle by 2020:

So, this time change will be driven by customers and suppliers will delay and delay then break in a rush.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.