No surprise at all, really. S&P sees a slight fall:

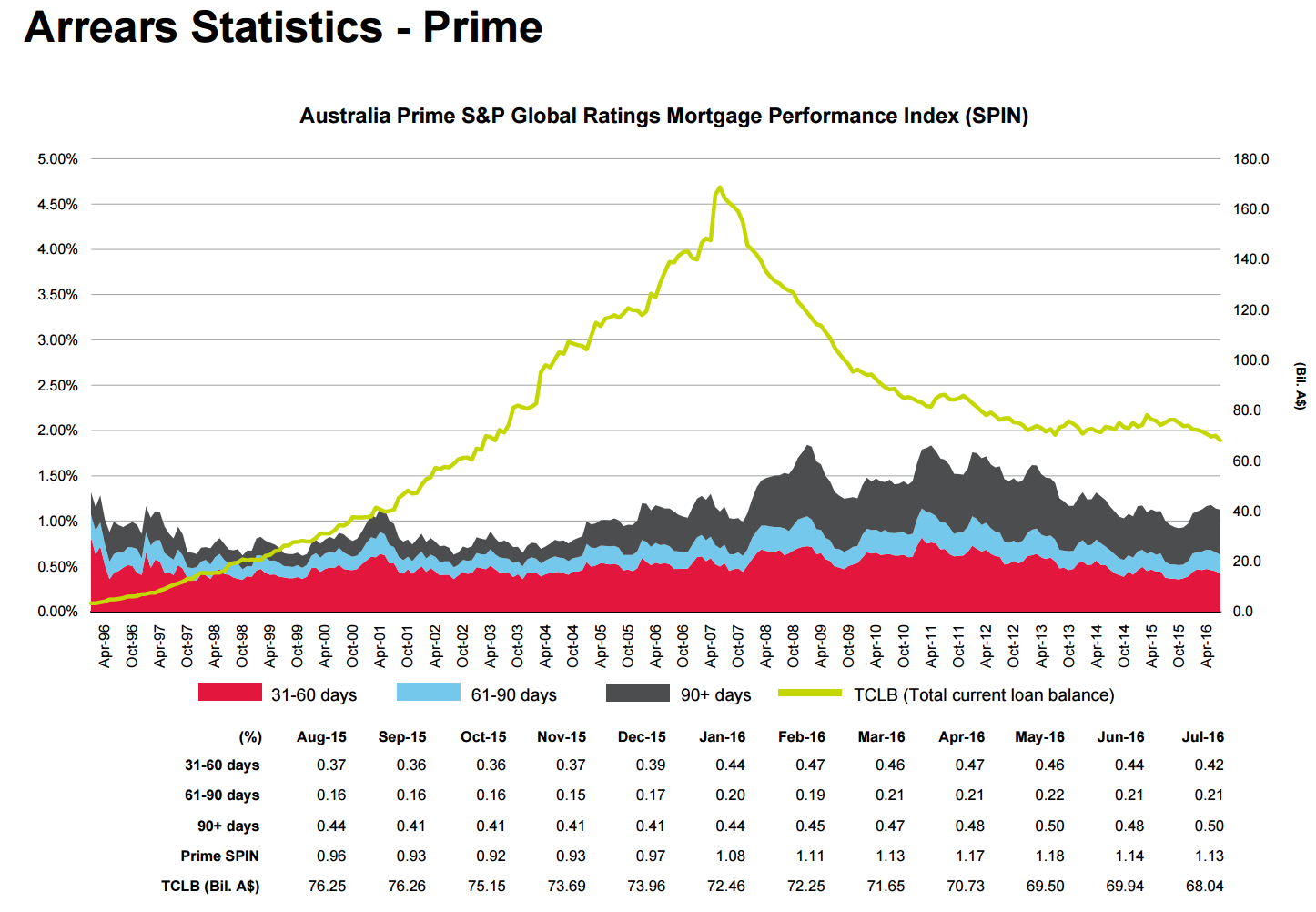

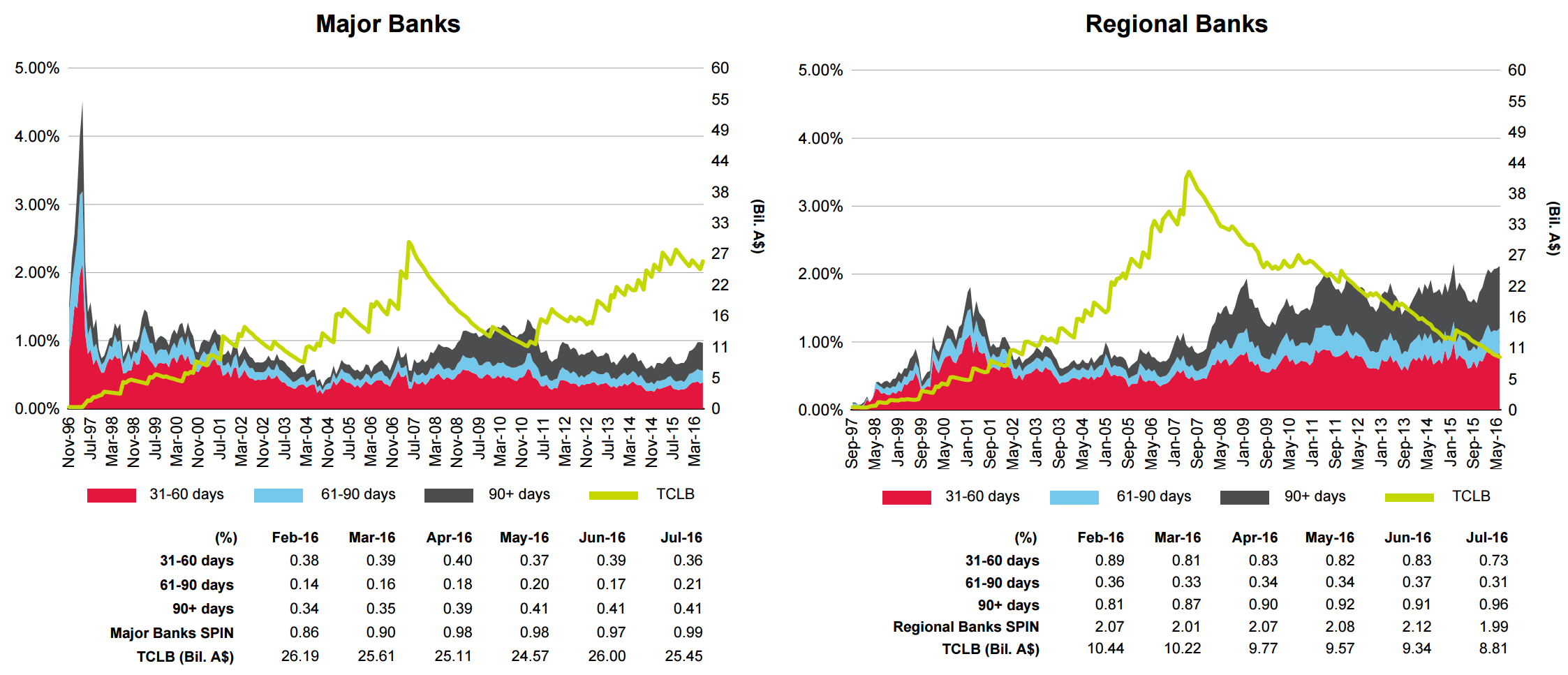

The number of Australian housing loans in arrears declined in July for the second consecutive month for prime residential mortgage-backed securities (RMBS), as measured by Standard & Poor’s Performance Index (SPIN). The prime RMBS SPIN was 1.16% in July, down from 1.19% a month earlier. We expect arrears to trend downward during the third quarter and most of the fourth, before climbing again in December as the effects of pre-Christmas spending start to kick in. Arrears in July were up 21% year on year, but remained below their peak and decade-long average. Low-documentation loans in arrears increased to 4.34% in July from 4.23% in June. Arrears on full-documentation loans meanwhile fell to 1.12% in July from 1.15% the previous month. Full-documentation loans account for more than 98% of loans underlying prime RMBS transactions and their performance largely dictates movements in the SPIN. Nonbank financial institutions continued to have the lowest arrears across originator types, at 0.71%, followed by other banks and nonbank originators, each at 1.07%. Arrears at the major banks were at 1.08% in July. Arrears fell month on month across all originator types except for other banks, which recorded an increase to 1.07% from 1.05% in June. A significant increase in the major banks’ outstanding loan balances, which have more than doubled since late 2012, has assisted with their lower arrears profile, with arrears generally trending below 1% during the past 14 years. Nonbank originators, despite experiencing a decline in outstanding loan balances of more than 65% since 2007, meanwhile have recorded a general improvement in arrears, particularly during the past 4.5 years, with arrears declining to 1.07% in July from 2.57% in January 2012.

I expect the “surprises” to continue as the entire county ex-Sydney and Melbourne stalls and sinks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.