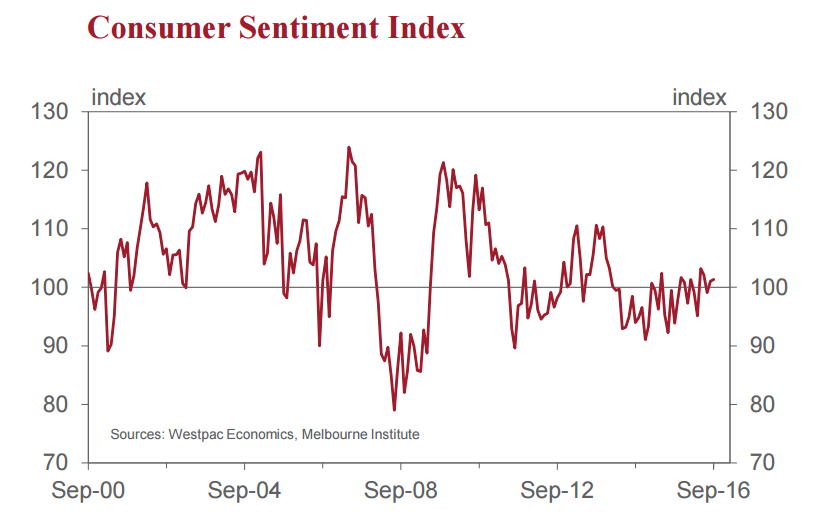

Consumer Sentiment has been remarkably stable for the last six months. Over that period the Index has averaged 100.3 so today’s reading is just 1.0% above this average. Indeed the September reading is just 1.7% above the average reading over the previous six month period to March as well.

This stability over the last six months has been despite significant events that can usually be expected to impact confidence: two interest rate cuts from the Reserve Bank and associated reductions in mortgage rates; a Commonwealth Budget; a Federal election; and some major developments offshore such as the surprise UK referendum result (‘Brexit’) and the build -up leading into November’s US election.

In the September survey we have the benefit of respondents nominating those news categories that they most recalled and whether that news was favourable or unfavourable. There have been some important trends that might explain the stability of confidence at a reasonably solid level.

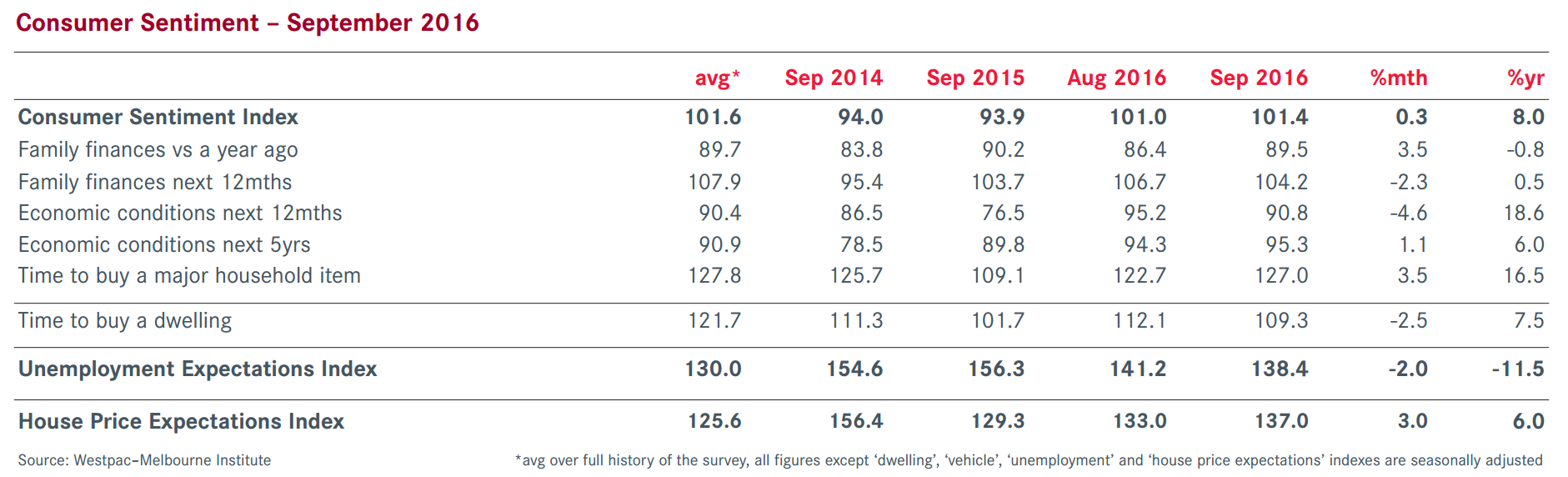

A year ago the most recalled news items were around ‘economic conditions’ (53.9% of respondents) and ‘international events’ (41.8% of respondents). Recall on these topics is now down to 21.9% and 11.4% respectively. Not surprisingly, the news is assessed to be considerably less unfavourable today than last year. Having said that there has been a marginal deterioration in the assessment of domestic economic conditions since June. That move has been more than matched by a significant improvement in the assessment of news on international conditions over the last three months.

The most recalled news category in September was ‘Budget and taxation’ (26%). News on this category has been assessed as more unfavourable than in June but still less unfavourable than a year ago.

Recall levels for news items on ‘interest rates’ (15.2%); ‘employment’ (11.9%); and ‘inflation’ (6.4%) have been fairly steady over the last year. However for all of these categories, we have seen significant improvements in how news has been viewed.

That theme of improving assessment of the jobs market is supported by the Westpac Melbourne Institute Unemployment Expectations Index. This fell from 141.2 in August to 138.4 in September (down 2%, recalling that a lower print means fewer respondents expect the unemployment rate to rise in the year ahead). The Index is now down 11.5% over the last year and 10.5% since September 2014. The Index was stubbornly high through 2012- 2015 so it is very encouraging that confidence seems to be gradually returning to the jobs market. 14 September 2016 • The Westpac Melbourne Institute Index of Consumer Sentiment increased by 0.3% in September from 101.0 in August to 101.4 in September.

Confidence in the housing market is improving. The ‘time to buy a dwelling’ index fell 2.5% in September from 112.1 in August to 109.3 in September. The Index is still 7.5% above its level from a year ago and 4.3% above its average for the last six months. Confidence in both the major markets improved over the month. Sydney lifted by 4.0% and Melbourne rose by 5.1%.

Confirmation of a continuation of improvements in the housing market was apparent in the Westpac Melbourne Institute Consumer House Price Expectations Index which increased by 3.0% for the month to be up by 6.0% for the year. Increases were recorded in NSW, Victoria and Queensland.

There were mixed messages around the components of the Index. Of most significance was a 3.5% jump in the sub-index tracking assessments of ‘family finances vs a year ago’. Readers will recall that the Reserve Bank usually highlights this component when discussing its assessment of the consumer in its quarterly Statement on Monetary Policy. Less encouraging was a 2.3% fall in the subindex tracking views on ‘family finances over the next 12 months’. While the overall Index is up 8% over the last year both ‘family finances’ components are around the same levels.

Confidence around the economic outlook deteriorated somewhat. The sub-index tracking views on ‘economic conditions over the next 12 months’ fell by 4.6% while the ‘economic conditions over the next 5 years’ sub index increased by 1.1%.

The sub-index tracking assessments of ‘time to buy major household Item’ increased by 3.5% to now be 16.5% up on a year ago.

In this survey, we also receive information on respondents’ saving preferences .These responses are particularly important for assessing whether there has been a change in risk aversion. Consistent with ‘stability’ in the overall survey we saw little change in saving preferences. Most respondents still see bank deposits as the wisest form of saving (29.9% up marginally from 29.5% in June). That proportion compares to the 40yr peak of 39% in 2012 when risk aversion was much higher.

A second measure of risk aversion is the component ‘pay down debt’. That proportion increased from 20.0% to 21.0% and compares with record high of 27% in 2010. However the ‘pay down debt’ component has steadily lifted over the last three years.

The proportions favouring ‘real estate’ (15.4%) and ‘shares’ (8.6%) remained steady in September.

The Reserve Bank Board next meets on October 4. This will be the first meeting under the new Governor Lowe. It is extremely unlikely that there will be any change to rates at that meeting.

Since the cash rate returned to its historical low of 3% in 2013 all six subsequent cuts have occurred on the meetings in February/ May/August and November when the Bank has a ‘fresh’ print on inflation and is able to communicate any forecast changes in its quarterly Statement on Monetary Policy. That really suggests that the next ‘live’ meeting will be November 1.

We expect rates will be held steady in November as well. Signs of stability in the real economy, as signalled in this report, point to steady rates being the most appropriate policy. Of course there is always the possibility of a shock from the inflation report on October 26 but both our inflation forecasts and our assessment of current high RBA inertia to moving again this year point to stability in November.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.