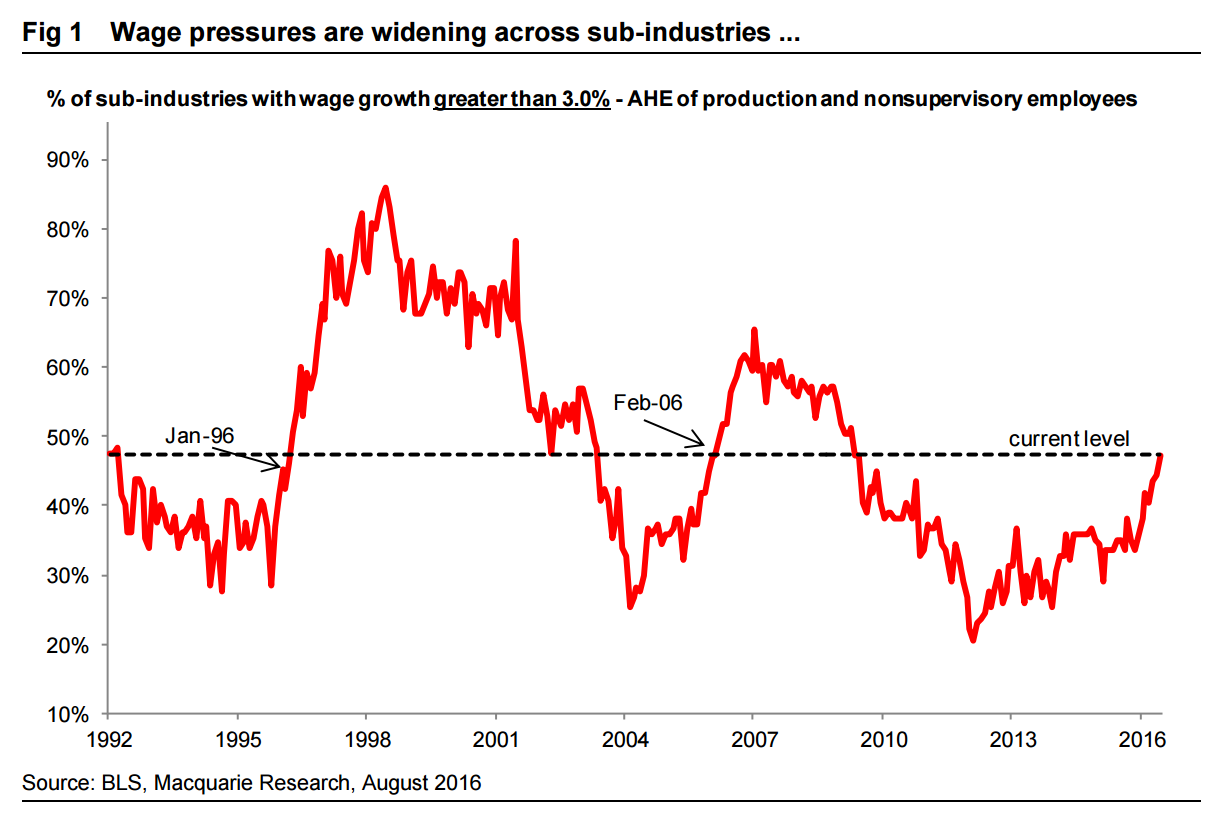

Evidence continues to mount in our proprietary analysis of 131 sub-industries that headline wage growth (average hourly earnings) is on the cusp of further acceleration and new jobs are of high quality. Our work shows wage growth has broadened significantly across sub-industries in recent months. In the past two cycles, this foreshadowed accelerating headline wage growth. As of June, nearly 50% of sub-industries had YoY wage growth greater than 3.0%, showing a dramatic broadening in 2016 (Fig 1). Similarly, our median sub-industry measure reached a cycle high of 2.9% (Fig 2).

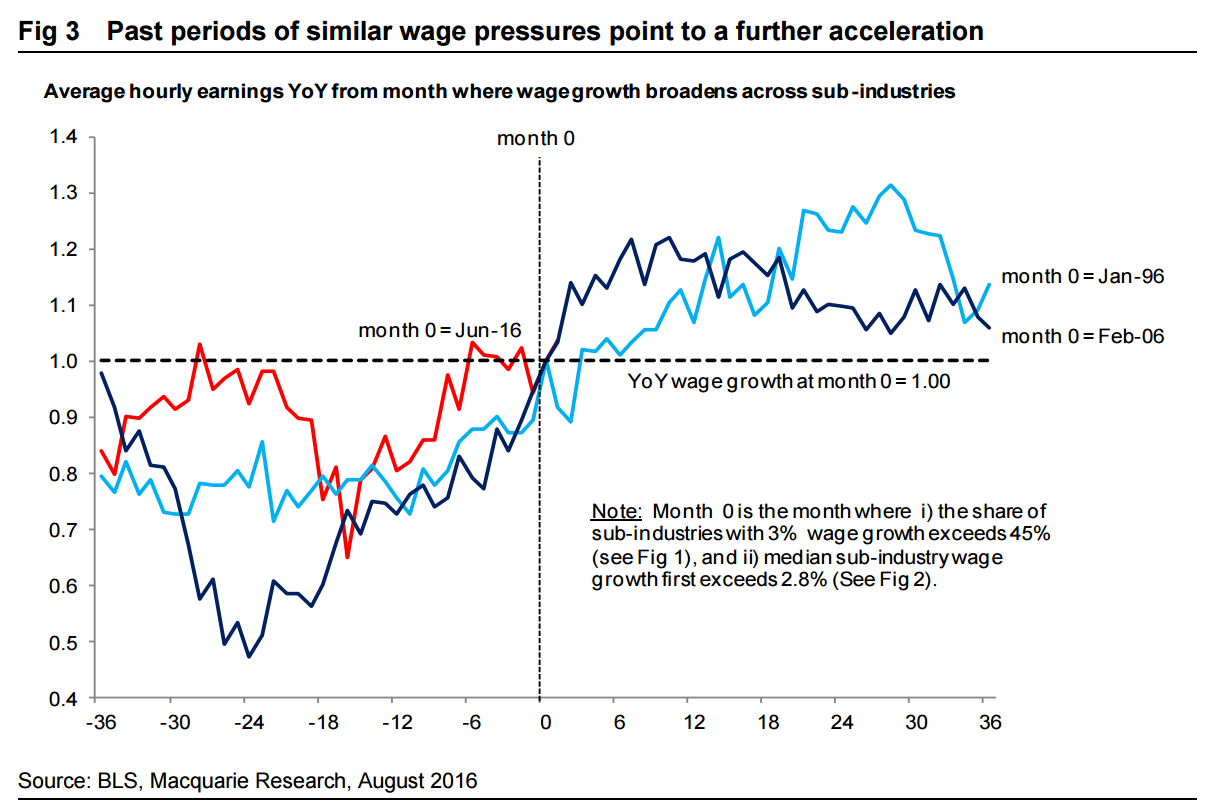

In the last two expansions wage growth similarly broadened in Jan-96 and Feb-06. In both instances, the YoY measure moved 20% higher over the next 12-18 months (Fig 3). This suggests headline wage growth should rise above 3% before end-17. What’s more, our preferred measure (the Atlanta Fed Wage growth tracker) is suggesting this acceleration is already occurring “on the ground”. Proprietary analysis indicates wage growth has turned

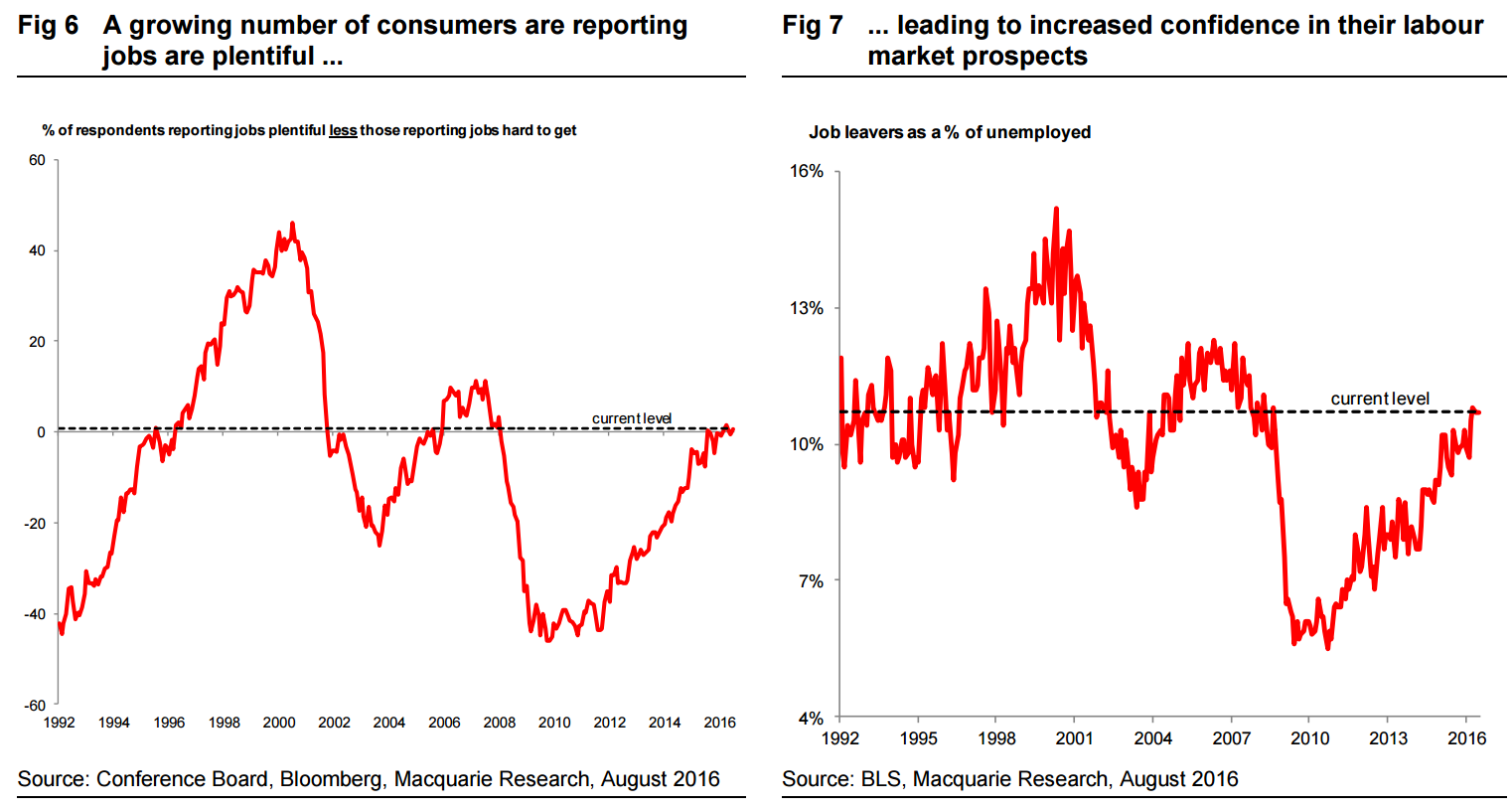

Several indicators suggest the pace of gains will further accelerate. i) The ratio of job openings to the unemployed is above the 2002-07 expansion peak (Fig 4). ii) Small business owners are continuing to report a high level of job openings they cannot fill (Fig 5). iii) An increased share of respondents view jobs plentiful rather than hard to get (Fig 6). iv) A growing percentage of the unemployed are workers that have willingly left their jobs (Fig 7). v) The Beveridge curve has shifted outward indicating employers are struggling to find qualified workers (Fig 8).

If we were to use this analysis as a guide to the durability of the US (and global) business cycle, recognising that in the normal run of events it is Fed tightening that ends it, we would conclude that the cycle has another 2-3 years to run and that the Fed might be able to get away another two or three hikes before it all comes tumbling down. Remembering that the Fed will be in no hurry to cut short labour income gains in this cycle owing to the need to deleverage and reboot middle class income.

I would describe that as the global best case, possible so long as European exit politics doesn’t get moving and China doesn’t crash through its glide slope. Macquarie describes it as the “long, grinding cycle”:

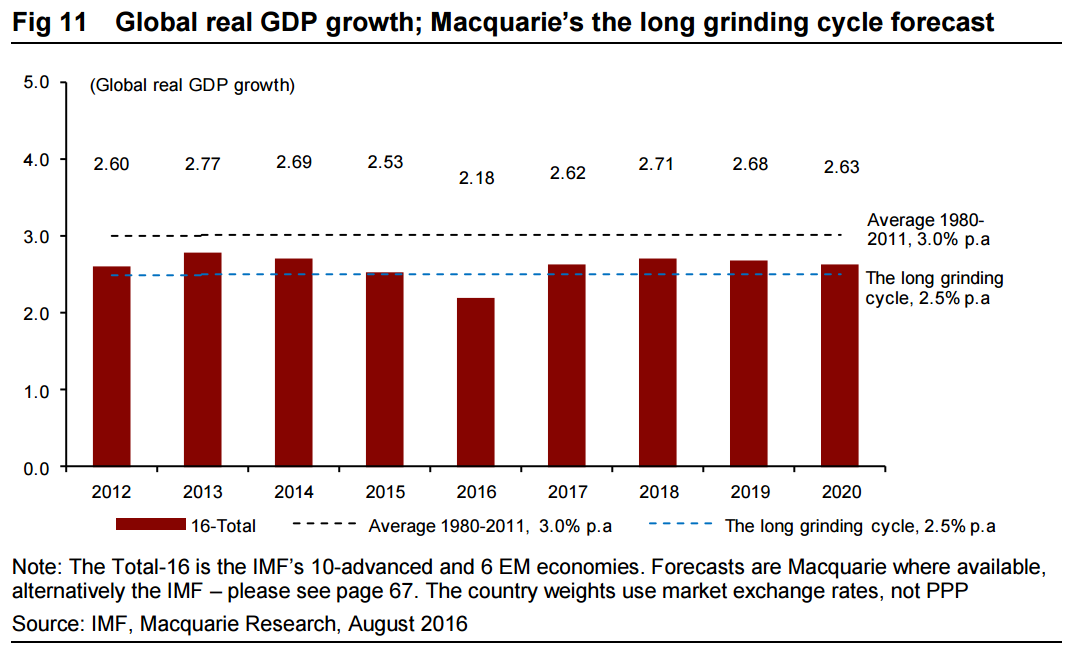

When looking to the financial markets for guidance, some see a record-high on the S&P 500; some see record-low bond yields. Those focussing on the record-low bond yields see a signal of an impending global slump, and regard global equities as highly vulnerable – the half-empty view. Those focussing on the record-high in the S&P 500 foresee an earnings reacceleration, global growth lift-off, and believe that low bond yields cannot persist – the half-full view. We see both. A record-high on the S&P 500 and record-low bond yields is a combination consistent with moderate global growth. It is not a combination consistent either with a global slump or with global lift-off. As Fig 11 shows, global growth has been remarkably stable since 2012. This is long enough to believe that financial markets have come to reflect this as “the new normal”. As Fig 11 also shows, our forecasts out to 2020 are for a continuation of moderate global growth, for the long, grinding cycle and associated low bond yields to continue (more below).

Advertisement

If it were to transpire then the current MB allocation matrix would look reasonable as:

equities slowly grind higher but so do bonds, especially Aussie as interests rates keep falling;

the US dollar remains bid but only slowly so gold remains firm as the bond curve remains flat;

the Aussie dollar would steadily fall with commodity prices and a closing yield gap,

and local house prices might hold up for a while longer before tanking into the next bust as monetary and fiscal policy is exhausted.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.