From Bill Evans at Westpac:

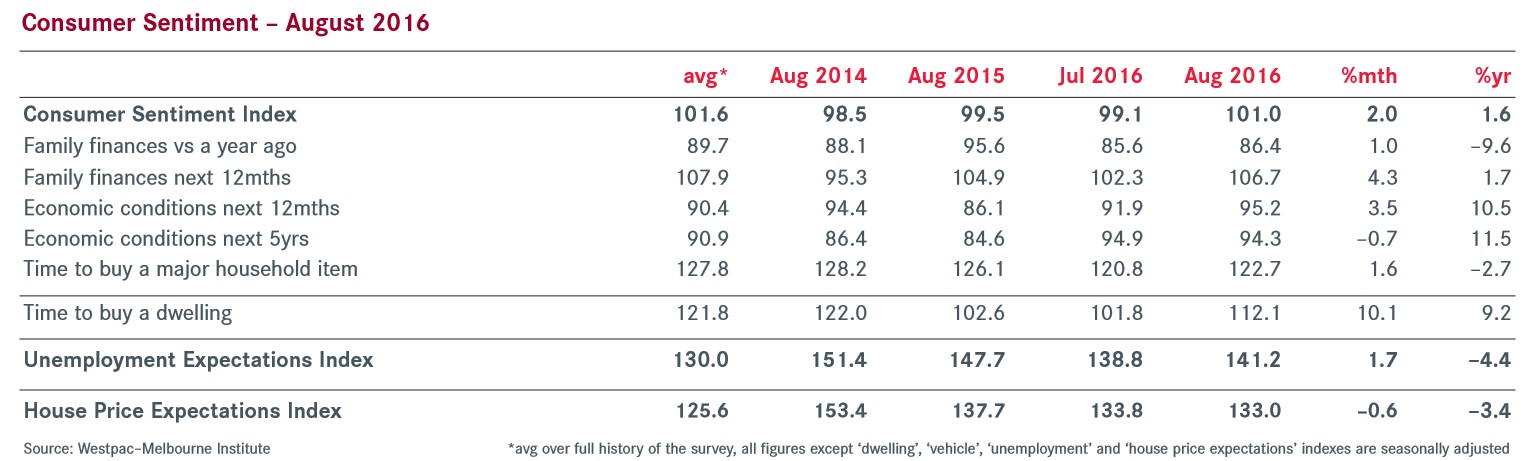

The Westpac Melbourne Institute Index of Consumer Sentiment increased by 2.0% in August from 99.1 in July to 101.0 in August.

The survey was conducted over the first four days of August, covering the Reserve Bank’s August 2 announcement of a 0.25% cut in the overnight cash rate from 1.75% to 1.5%. The response to this development has been much more muted than we saw in May when the Bank last cut the rate, from 2.0% to 1.75%.

On that earlier occasion the Index lifted by an impressive 8.5% from 95.1 to 103.2. That was an exceptionally large positive response and much stronger than the average rise following rate cuts historically. That can be explained by a number of factors. Firstly, there was a larger surprise element to the May decision with, arguably, significantly less intense media speculation than we saw in August. Secondly the standard variable mortgage rate offered by most banks was reduced by the full 0.25%, whereas in August the four major banks only reduced variable rates by 0.100.14%. Finally, the Index was coming from a significantly lower starting point in May (95.1) than in August (99.1).

Another development that may have unnerved respondents in August has been political unease. With the government having been returned with a wafer thin one seat majority in the House of Representatives and considerable change in the Senate, respondents might also be somewhat uncertain about future prospects around potential political stability.

Finally we have to accept that as interest rates go progressively lower some respondents, particularly those who may not have a mortgage, may become more unnerved about the signal that record low rates is sending about the economy. For example, in today’s result, while respondents with a mortgage responded strongly, there was a 1.3% fall in the confidence of those respondents who wholly own their properties.

That negative might have been expected to be even bigger for respondents that have low debt and rely on interest income. However, the decision by banks to raise some term deposit rates following the RBA rate cut has instead given a notable boost – sentiment amongst retirees in particular posted a strong 7% rise.

Notably, consumers do not expect to see more interest rate relief. In our special question around the outlook for mortgage rates, 37% of respondents expect mortgage rates to rise over the next 12 months; 36% expect rates to be steady; and just 27% expect further rate cuts.

Overall the lift in the Index is still consistent with an improved outlook for the Australian economy. We are now back in the range where optimists outnumber pessimists. Over the last thirty months there have only been eight when optimists have been in the ascendency with three of those months figuring in the last four.

In particular, prospects for the housing market appear to have been boosted by the rate cut. The confidence of those respondents who hold a mortgage lifted by 7%.

Westpac’s Index of ‘time to buy a dwelling’ rose by 10.1% to be up by 9.2% over the last year. In particular, the key states of NSW and Victoria showed strong improvements. The Index lifted by 19% in NSW and by 12.8% in Victoria. This is particularly significant for the key Sydney market where the Index is now 61% above the average of the second half of 2015 when confidence collapsed in the Sydney housing market.

The Westpac Melbourne Institute House Price Expectations Index was basically flat for the month but, consistent with the ‘time to buy’ index is signalling considerably more confidence than we saw at the start of the year. This Index has increased by 28% since the end of 2015.

Despite the lift in overall confidence prospects in the labour market deteriorated somewhat. The Westpac Melbourne Institute Unemployment Expectations Index increased by 1.7% from 138.8 to 141.2 (recall that higher reads indicate higher expectations for unemployment and a worsening outlook for labour market conditions). The Index is still 4.4% below its level from a year ago. However the promising improvement we saw in the Index near the end of last appears to have stalled over the course of this year.

Both of the components of the Index that assess family finances increased in the month. The ‘family finances vs a year ago’ subindex lifted by 1.0% and the ‘family finances over the next 12 months’ sub-index was up by 4.3%. This is the second highest read on the outlook for finances since October 2013 although there has been no comparable outperformance for the backwardlooking component, which is 9.6% below its level from a year ago. Note that in its Statement on Monetary Policy the Reserve Bank gives most attention to this component of the Index.

Short term confidence in the economy improved. The ‘economic conditions over the next 12 months’ sub-index lifted by 3.5% to be up by 10.5% over the year. While there was little movement in the ‘economic conditions over the next 5 years’ sub-index (down 0.7%) that Index is also up by an encouraging 11.5% over the year.

Retail prospects improved marginally with the ‘time to buy a major item’ sub-index up 1.6% (although still down 2.7% on a year ago).

The Reserve Bank Board next meets on September 6. Having cut rates at its last meeting the Board is almost certain to keep rates on hold in September. However it is clear from the Bank’s recent Statement on Monetary Policy that it holds an easing bias. That sentiment has encouraged markets to expect a further cut in November following the release of the next inflation report. The case for a cut is based on Australia’s ongoing low inflation environment.

However, by November, consistent with some of the messages in this survey we expect that economic conditions will have firmed sufficiently for the Bank to be more patient with its inflation objective. It may recognise that rigid adherence to the current inflation target of 2–3% might not be the best way to run policy in this current low inflation world.

Accordingly we expect that the Bank will decide to hold rates steady in November”