The CBA’s Gareth Aird has written another ripper report examining the casualisation of the Australian workforce and its implications.

Below are the key extracts.

Key Points:

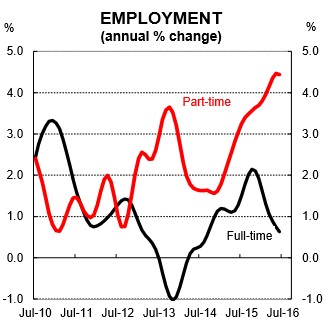

The ABS report that 87% of the lift in jobs over the past year has come via an increase in part-time employment.

The rise in the number of part-time employees as a share of Australia’s workforce is not new, but the pace of change has quickened.

The recent acceleration in part-time rather than full-time employment is concerning because it has been accompanied by a historically high underemployment rate.

Record low wages growth, below target inflation and pressure for more monetary policy easing are the consequence.

Overview:

The ability of the Australian economy to generate headline jobs growth while going through a massive downturn in mining investment (and associated job losses) has been impressive. Rate cuts, a lower Aussie dollar and the wealth effect have helped. Over the past two years, employment growth has outpaced growth in the population. As a result, the unemployment rate has trended down to 5¾%. These headline numbers look commendable. But they overstate the strength of the labour market.

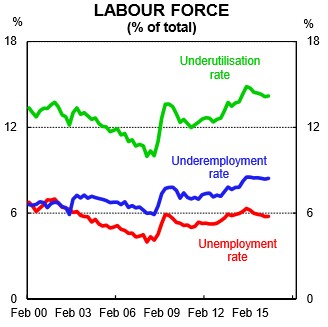

The majority of the net jobs created over the past few years have been part-time and in the more labour-intensive services sector which favours a more causal workforce. At the same time, the underemployment rate has been stuck around 8½% – its highest level on record. This means that there is a significant proportion of people who are working, but whose labour is not fully utilised. This is undesirable and means spare capacity in the labour market is a lot higher than the unemployment rate implies.

An elevated level of slack in the Australian economy (driven by labour force underutilisation), coupled with a large fall in the terms-of-trade, has led to record low wages growth and below target inflation. The RBA has responded by cutting its policy rate to a record low of 1.5%. In this note, we look at the casualisation of Australia’s workforce in the context of the shift towards part-time employment and the rise in the underemployment rate. We explore what has been happening, ask if it’s a problem and look at what it means for growth, wages and monetary policy over the period ahead.

What does the data show?

The ABS data indicates that over the year to July 2016, employment has risen by 1.9% – a lift in headcount of 220k. The split shows that 190k of those jobs were part-time and just 30k were full-time…

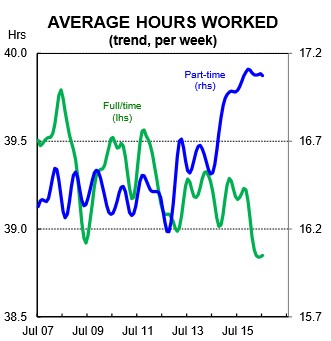

To recap, a worker is deemed to be employed full-time if they are working more than 35 hours a week. Working between 1 and 35 hours a week means a worker is considered part-time. So a part-time worker could be working a significant number of hours or hardly working at all. The latest figures show that a part-time employee works on average 17.1 hours a week. A full-time worker on average clocks up 38.9 hours…

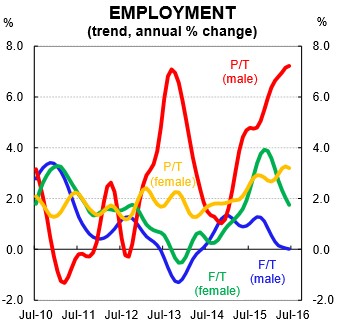

The lift in part-time jobs has been broad-based – across both genders and most age cohorts. However, the big growth in part-time employment has been for men…

Is it structural or cyclical?

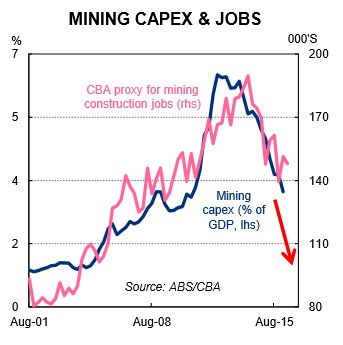

The shift towards part-time employment is not new… The pace of change, however, has accelerated over the past year, primarily because of the downturn in mining and related construction activity and associated reduction in headcount…

As has been highlighted on many occasions, the third and final phase of the mining boom – production – is not labour intensive like construction. As such, output in the resources sector has lifted significantly while headcount has fallen. There have also been full-time job losses in the manufacturing, utilities and wholesale sectors…

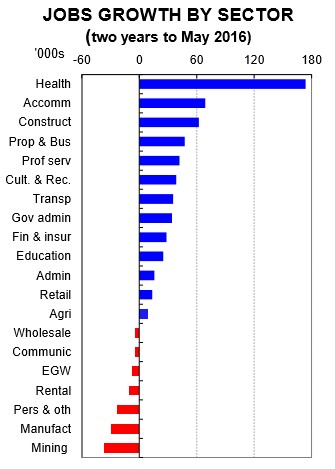

The shift towards part-time employment is structural, but a cyclical downturn in mining employment has exacerbated the trend. Recent job creation has largely been in the services sector where a greater proportion of the workforce is employed on a part-time basis. The health sector (especially aged care) and tourism industry in particular have seen headcount lift significantly. These sectors have a high proportion of their workforce employed on a part-time basis.

Is it a problem?

As a general rule, economists and policymakers should welcome part-time employment growth when it reflects the desires of employees… As a society, a shift towards part-time employment is a positive development if that reflects the desires of the population… The well-being of society should come above the pursuit of economic growth – if a shift to part-time employment is part of raising welfare then it should be embraced.

However, growth in part-time employment, rather than full-time work, becomes a problem (and indeed undesirable) when there is growth in the number of workers who are not working as much as they would like. This is captured in the underemployment rate. Unfortunately, the underemployment rate has been rising in Australia and it remains near its highest level on record. This indicates that a growing proportion of people are employed, but they are not working as much as they would like.

The sum of the unemployment rate and the underemployment rate produces the underutilisation rate which is the broadest measure of spare capacity in the labour market – it is high and presently sits above the level hit during the Global Financial Crisis. This means that the economy is operating below its capacity and there is an output gap. This has had implications for wages and inflation…

In our view, a material lift in investment (business or public) is likely to be the precursor to an increase in full-time jobs growth. Generally, a lift in investment is a sign of a genuine lift in current and expected demand. We would expect to see labour demand grow in such circumstances.

In the short term, a lift in private investment looks unlikely…

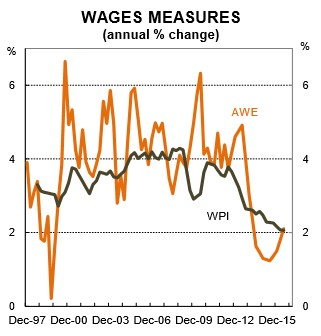

Whichever wage you slice it, wage growth is weak. The pulse of wage inflation is soft and the compositional changes in the labour market are negatively impacting the mining states (i.e. WA and QLD) in particular…

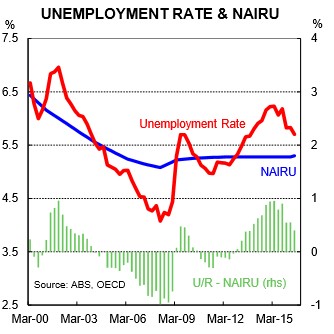

In our view, wages growth is unlikely to lift until the unemployment rate gets closer to the non-accelerating inflation rate of unemployment (NAIRU which is around 5¼%) and the underemployment rate starts moving south. Or to put it more generally, spare capacity in the labour market needs to be gobbled up for wages growth to increase. We are some way off that…

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.