by Chris Becker

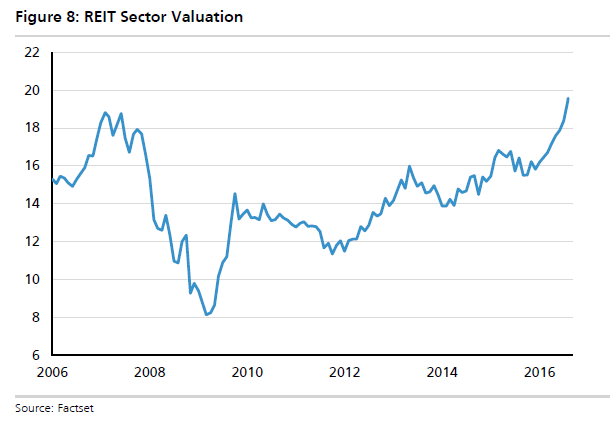

With office vacancy rates at near record levels in Brisbane and Perth, and retail sales growth flagging, it’s timely that UBS has a research note out explaining that while other risky and cyclical stocks are trading below value, the defensive income side – with REIT’s leading the way – are grossly overvalued:

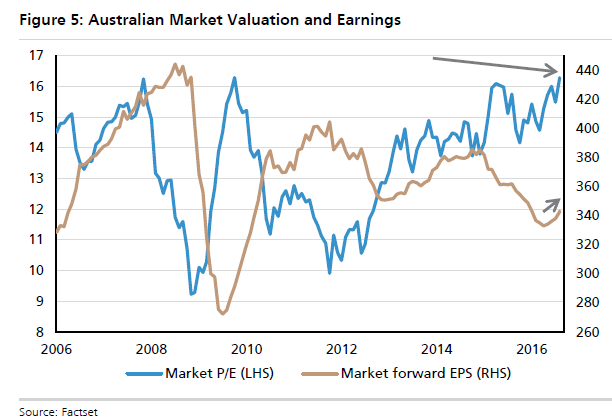

While the market’s valuation at over 16x looks stretched in an absolute sense, we think “dispersion” of valuation is still the bigger story. Defensive growth (e.g. health care) and defensive income (e.g. REITs) are trading well above historical valuation levels while cyclical/risky areas of the market are trading seemingly cheaply. This remains both a global and domestic theme.

Better growth and an upward shift in interest rates is the most obvious catalyst for a more concerted shift towards cyclicals/value but growth continues to look patchy and bond yields continue to test fresh lows. While there is no doubt that growth has downshifted structurally, bond yields are still discounting too bearish a view of growth prospects in our view.

Real rates are negative just about everywhere while nominal long term rates are negative in a number of countries. However, ongoing QE in Europe and Japan may continue to depress yields for some time. This leaves us moderately underweight popular income areas like REITs (where yields are actually below market) but cognisant that the search for yield will likely continue.

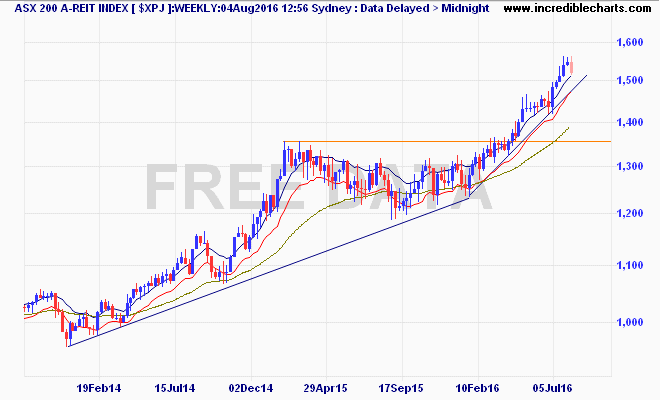

With the RBA cutting rates and Australian bond yields under pressure, the only thing left apart from diverging term deposits are those juicy REITs for yield chasers:

But at pre-GFC valuation? Nuts. The technical picture clearly shows an accelerating bubble:

Underweight? Stay away unless you are very quick at pressing that “SELL” button.