by Chris Becker

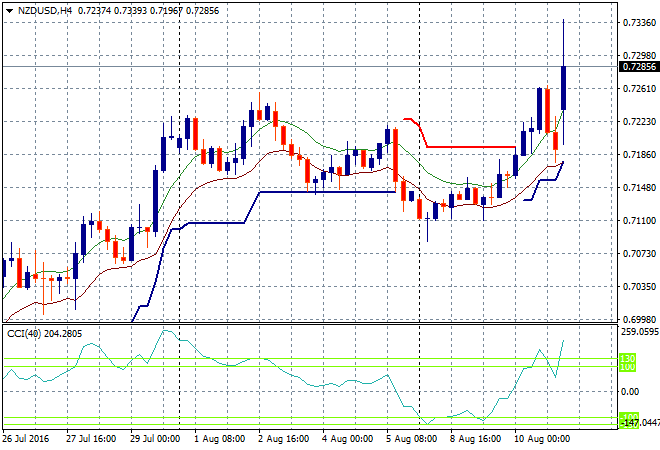

As I mentioned yesterday, New Zealand remains the only major Western economy with interest rates above that of Australia, but has just cut them to the “bone” to 2% even. The Kiwi raced ahead to over 73 cents against the USD, almost making a new high for the year:

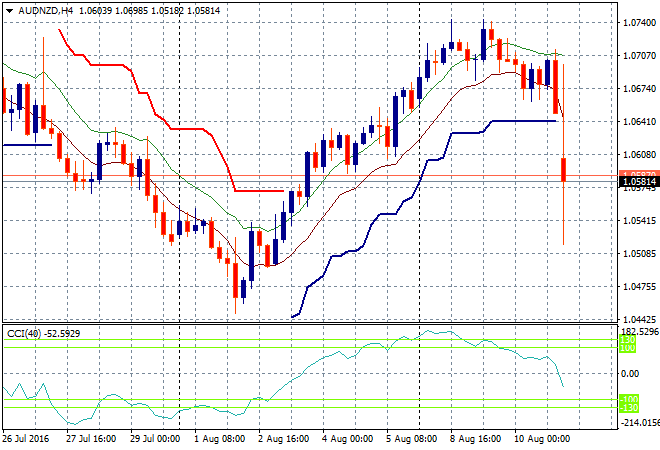

Meanwhile the Aussie/Kiwi slumped as interest rates start to converge:

The gist from Bernard Hickey at interest.co.nz:

Wheeler said weak global conditions and low interest rates relative to New Zealand were placing upward pressure on the New Zealand dollar.

“The trade-weighted exchange rate is significantly higher than assumed in the June Statement. The high exchange rate is adding further pressure to the export and import-competing sectors and, together with low global inflation, is causing negative inflation in the tradables sector,” Wheeler said.

“This makes it difficult for the Bank to meet its inflation objective. A decline in the exchange rate is needed,” he said.

“Domestic growth is expected to remain supported by strong inward migration, construction activity, tourism, and accommodative monetary policy. However, low dairy prices are depressing incomes in the dairy sector and reducing farm spending and investment,” he said.

“High net immigration is supporting strong growth in labour supply and limiting wage pressure.”

Wheeler said that house price inflation remained excessive and had become more broad-based across the regions, “adding to concerns about financial stability,” and he noted that the bank was consulting on stronger macro-prudential measures to help risks to the financial system from the rapid escalation in house prices.

“Headline inflation is being held below the target band by continuing negative tradables inflation. Annual CPI inflation is expected to weaken in the September quarter, reflecting lower fuel prices and cuts in ACC levies. Annual inflation is expected to rise from the December quarter, reflecting the policy stimulus to date, the strength of the domestic economy, reduced drag from tradables inflation, and rising non-tradables inflation,” Wheeler said.

“Although long-term inflation expectations are well-anchored at 2 percent, the sustained weakness in headline inflation risks further declines in inflation expectations,” he said.

“Monetary policy will continue to be accommodative. Our current projections and assumptions indicate that further policy easing will be required to ensure that future inflation settles near the middle of the target range. We will continue to watch closely the emerging economic data.”

The Reserve Bank’s central forecast for the 90 day bill rate included the potential for one more 25 basis point cut to 1.75% some time over the next six months.

Only one more cut is what has “disappointed” markets as the RBNZ like the RBA is caught between a rock and a hard place with housing bubbles and the international interest rate war overriding effective monetary policy.