A couple of sell side wraps for EVN (which I quite like the look of). From Morgan Stanley:

EVN is acquiring an interest in the Ernest Henry copper-gold mine, taking the gold production and a share of copper, funding the deal via an entitlements issue and additional debt, though our preliminary view is EVN will once again rapidly delever via strong group cash flows. Buying Ernest Henry’s gold stream (and 30% of copper) – a novel transaction to buygold: EVN has agreed to buy 100% of future gold and 30% of future copper and silver production from the Glencore operated Ernest Henry mine for A$880mn (ex trans costs). The mine has been in operation since 1997, originally an open pit, moving to a sub-level cave U/G operation following a ~A$600mn capital investment. This gives EVN access to ~1Moz of gold and ~184kt of net copper reserves. The mine has an 11yr life under the current plan,equating to ~73kozpa over the life of mine, though we expect higher production in the next 5 years. AISC in FY16 (pro-forma based on EVN’s ownership structure) would have been -A$59/oz,given the considerable copper credits, though guidance for FY17 implies AISC of A$10/oz.

Funding via entitlement offerand debt: EVN is undertaking an underwritten 2- for-15 pro-rata accelerated renounceable entitlement offer to raise A$401mn and will also obtain a new A$500mn term loan. The entitlement offer price is A$2.05/sh, reflecting a 13% discount to TERP of A$2.37/sh. EVN expects gearing to peak at ~22%, similar to peak levels seen post Cowal. Total debt would be ~A$800mn,adding pro-forma FY16 Ernest Henry FCF(EVN’s pro-forma share) to our base-case FCF expectations over the medium-term would see EVN able to pay down this debt in <2yrs. This is just a preliminary calculation, but highlights the potential to rapidly delever (again).

Transaction metrics look fair to full value, as was the case for Cowal and Mungari…: EVN states FCFin FY16 would have been A$141mn at spot prices, which equates to a 6.2x multiple. This is around a 30% discount to EVN’s current EV/FCF multiple on our base-case model at spot prices. On a reserve and resource multiple, the deal equates at A$530/oz Au equivalent,above Cowal (A$445/oz) and in line with Mungari (A$530/oz).

…but the value-add opportunity could be more challenging as a minority holder: At the time, we thought both the Mungari and Cowal acquisition prices appeared rich, but were pleasantly surprised by the value-add created by EVN after the assets were brought in to the fold. With EVN having a minority interest in this case,upside could be more challenging to find, though we acknowledge the JV terms appear to cover EVN’s position in the event of major changes to the Evolution Mining ( EVN.AX, EVN AU ) current mine-plan. We need to do more work in valuing the new asset, but we note EVN management stated it sees ~1.5x base case upside if current spot AUD gold prices, consensus copper and 5yr mine-life additions are factored in.

And Citi:

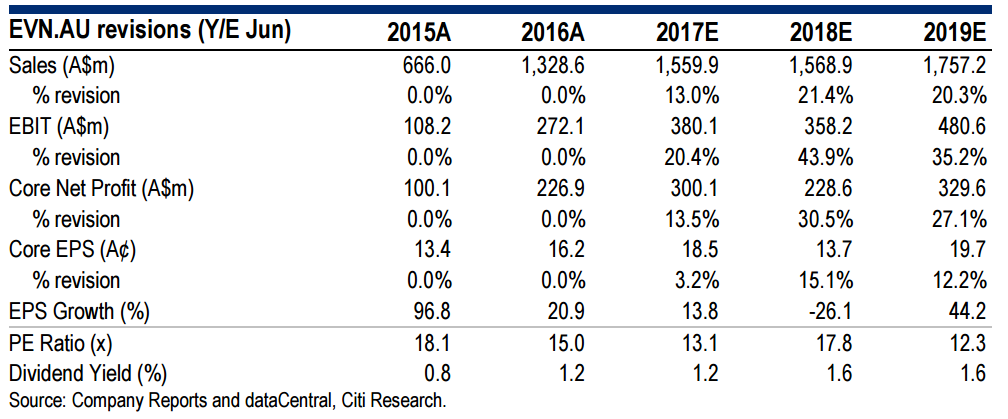

Upgrade to Neutral — EVN has continued its strong track-record of M&A, and cemented its place as Australia’s second-largest gold producer, after a deal with Glencore over the Ernest Henry copper-gold mine in QLD. EVN has lifted FY17 guidance to 830kozpa @ AISC A$930/oz (+57kozpa, -$70/oz) and added long-life, low-cost production to its portfolio. We see the deal as a value-add for NPV and earnings, and upgrade to Neutral with a target price of A$2.55/sh (+25cps).

Ernest adds low-cost gold — In what amounts to a metal streaming deal, EVN will pay Glencore (GLEN.L) A$880m (~US$670m) for a share of production from the GLEN-managed Ernest Henry, getting 100% of gold plus 30% of copper and silver over an agreed life (11 years) and block model; it will pay 30% of production costs. If the mine extends, EVN receives 49% of metal and pays 49%. The deal, settling Nov 1st, is funded by a $500m term facility and $401m rights issue at $2.05/sh – a 13.4% discount to the ex-rights close and 11% discount to our previous valuation.

Key assumptions and valuation — We estimate that NPV of the deal is A$1070m, a value-add of $170m including $21m fees. The mine is an underground sub-level cave with reserve 57.9Mt. We model 6.4Mtpa at reserve grades (0.54g/t Au, 1.06% Cu) over 11 years, to produce 89kozpa Au (100% EVN) and 64kt Cu (30% EVN, i.e. ~19kt). Recoveries: 80% Au and 94% Cu; EVN indicates payabilities of 96-98%. Opex is A$24/t mined, $12/t processed, $6/t G&A; while capex is sustaining at $40m/yr over the next 3-4yrs; overall, AISC could be negA$6/oz Au for FY17.

Upside — The LoM could extend beyond 2027 – EVN says it sees another 5yrs at least (the resource is 96.1Mt), which could add 20cps to our valuation. Throughput could be lifted to 7Mtpa. The Cloncurry area is prospective for IOCG deposits; GLEN has agreed that EVN will drive exploration, which could lead to a JV. Changes to estimates — The new low-cost production lifts post-issue EPS 3% in FY17E and 15% in FY18E; this increases our target price by 25cps.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.